Inside China's Machine: Humanoid Industry Landscape

140 companies. Over 10,000 robots. One question nobody is asking.

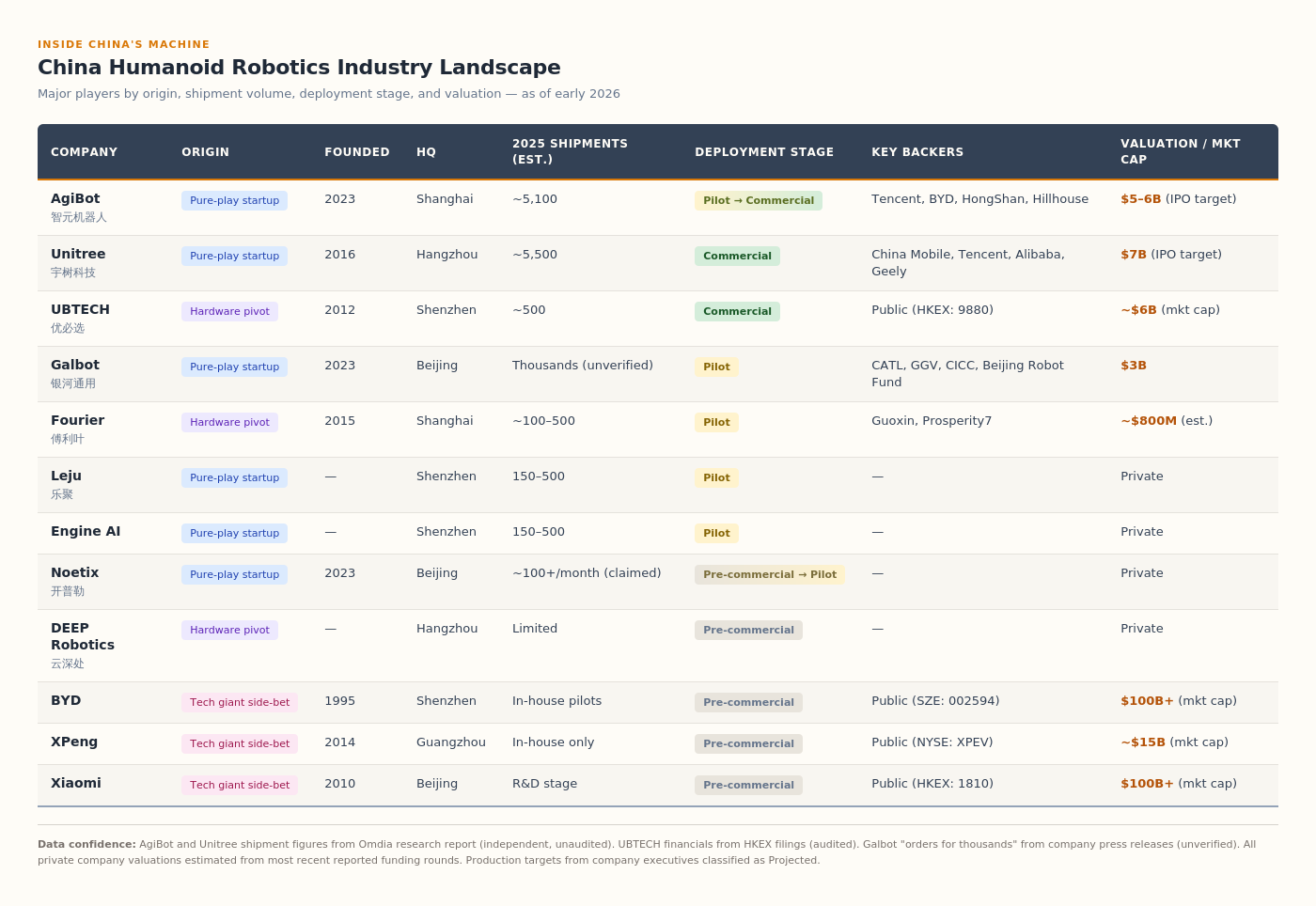

In January 2026, research firm Omdia released its first global ranking of humanoid robot shipments. The top three names were all Chinese. AgiBot led with an estimated 5,168 units. Unitree followed with roughly 5,500, though the two firms dispute who is actually number one depending on counting methodology. UBTECH came third. Together with Leju Robotics, Engine AI, and Fourier, Chinese companies accounted for approximately 87 to 90 percent of the roughly 13,000 humanoid robots shipped worldwide in 2025.

Those numbers have appeared in nearly every media article about China’s robotics sector since. They sound impressive. They should.

But they conceal more than they reveal.

The industry’s entire 2025 global output, 13,000 humanoid robots, would fill one floor of one warehouse. China’s Ministry of Industry and Information Technology (工信部) counts over 140 domestic manufacturers and more than 330 models. That means the average company shipped fewer than 100 units. Most shipped none.

Then, of the robots that did ship, how many are doing productive work? Not sitting in a university lab, not performing on a conference stage, not collecting data in a training facility. Actually working. That is the question almost nobody is asking, and it is the question that separates the companies that matter from the ones that merely exist.

This article is a map of who is actually building China’s humanoid robot industry, what their machines are doing in the real world, and which of the 140 companies might still exist in five years. The framework: a deployment reality matrix that sorts every major player by where they came from and how far they have gotten from the demo stage to productive work.

The Framework: Origins and Deployment Reality

China’s humanoid robotics landscape looks chaotic from the outside. Over a hundred companies, dozens of form factors, a blizzard of funding announcements. But a pattern emerges when you sort the field along two axes.

Axis one: origin story. Where did this company come from? Three distinct paths lead into Chinese humanoid robotics. First, the pure-play robotics startups: companies founded specifically to build humanoid or embodied intelligence platforms. AgiBot, Unitree, Galbot, Noetix. Second, the hardware pivots: companies that built expertise in adjacent robotics and redirected it toward humanoids. UBTECH pivoted from educational and entertainment robots. Fourier pivoted from rehabilitation exoskeletons. DEEP Robotics pivoted from quadrupeds. Third, the tech giant side-bets: established corporations, usually automakers or consumer electronics firms, that launched humanoid programs as extensions of existing AI and manufacturing capabilities. BYD, Xiaomi, XPeng, Huawei.

Axis two: deployment stage. Not what the company claims, but what the available evidence supports. Three tiers. Pre-commercial: the company has demonstrated prototypes, attracted funding, and perhaps shipped units to research labs, but has no documented productive deployment. Pilot deployment: the company has robots operating in real commercial or industrial environments, but in small numbers, typically fewer than a hundred units at a handful of sites, and usually with significant human oversight. Commercial production: the company is manufacturing at scale, fulfilling paid orders, and can point to repeat customers or multi-site deployments.

The combination produces a landscape that is far less crowded than 140 companies suggests. Most of the 140 sit in the pre-commercial corner. The interesting story is in the handful that have moved beyond it.

The Landscape

Notes on data confidence: AgiBot and Unitree shipment figures come from an Omdia research report, an independent but unaudited source. UBTECH’s financials are from its Hong Kong Stock Exchange filings, the only audited figures on this list. Galbot’s “orders for thousands” claim comes from company press releases and has not been independently verified. All valuations for private companies are Estimated from the most recent reported funding rounds.

Company-by-Company Analysis

AgiBot (智元机器人): The Speed Record

AgiBot’s story is a case study in Chinese startup velocity. Founded in February 2023 by Peng Zhihui, a former Huawei engineer who became famous on Bilibili for his DIY robotics projects, the company shipped its first prototype within six months. By January 2025, it had manufactured roughly a thousand units. By year’s end, Omdia estimated it had shipped over 5,100.

That pace is startling by any standard. For context, Boston Dynamics spent decades moving from research to commercial products. AgiBot went from founding to global shipment leader in under three years.

The product line spans three form factors. The A2, a full-size humanoid standing 169 centimeters, is the flagship service robot. It holds certifications for China, the United States, and European markets. The Yuanzheng series targets industrial applications, and in August 2025 AgiBot announced a deal worth tens of millions of yuan with automotive parts manufacturer Fulin Precision Engineering (富临精工) to deploy nearly 100 Yuanzheng robots at factory locations. That deal represents one of the largest documented commercial humanoid deployments in Chinese manufacturing.

The company has also built what it calls the largest embodied data collection facility: a 4,000-square-meter site in Shanghai’s Lingang district where roughly 100 robots continuously learn to perform domestic and industrial tasks across more than 3,000 real objects. This data factory feeds the company’s proprietary vision-language-action model, Genie Operator 1.

The capital trajectory matches the speed. AgiBot completed at least eight funding rounds in two years, attracting Tencent, BYD, HongShan (formerly Sequoia China), Hillhouse, and Warburg Pincus. A Hong Kong IPO is expected by mid-2026, with a target valuation between HK$40 billion and HK$50 billion (roughly $5.1 to $6.4 billion). CICC, CITIC Securities, and Morgan Stanley are named as sponsors.

Deployment reality: The Fulin deal and the data collection facility suggest genuine commercial traction, but the overwhelming majority of AgiBot’s 5,100 shipped units are research platforms and data collection robots, not autonomous factory workers. AgiBot’s own disclosures indicate that of its early production run, around 200 units were for internal use. The company has not released a breakdown of how many of the remaining units are performing productive work versus serving as research or demonstration platforms. At the current stage, AgiBot is shipping at scale but deploying productively at pilot scale.

Unitree (宇树科技): The Price Destroyer

If AgiBot’s story is about speed, Unitree’s is about price. Founded in 2016 by Wang Xingxing in Hangzhou, Unitree built its reputation in quadruped robots, capturing nearly 70 percent of the global market by 2023. The pivot to humanoids came with the H1, a full-size humanoid priced at $90,000, followed by the G1, launched in mid-2024 at 99,000 yuan (roughly $13,600), a price point that made competitors blink.

Then it went lower. The H2, a full-size humanoid at 182 centimeters, launched in October 2025 for $29,900. And in 2025, Unitree released the R1 at $5,900: a 127-centimeter humanoid that is, by a significant margin, the cheapest on the global market. For the price of a used car, a university lab can now buy a walking, talking robot with 26 degrees of freedom and a multimodal language model.

The pricing strategy is deliberate. Morgan Stanley’s research noted that the G1 is likely the most widely deployed humanoid robot in the world. At $16,000, it reaches universities, research labs, and state-owned enterprises that would never pay $90,000 for an H1 or $250,000 for a Western alternative. Unitree’s bet: cheap hardware creates a data flywheel. Every G1 sold is a node generating training data that improves the next generation of models.

The financial profile is unusual for the sector. Unitree has been profitable since 2020, a claim supported by its IPO filings, with annual revenue exceeding 1 billion yuan ($140 million). The company completed its pre-IPO tutoring with CITIC Securities in just four months, signaling regulatory support, and is expected to list on Shanghai’s Science and Technology Innovation Board (科创板) by mid-2026 at a target valuation of up to 50 billion yuan ($7 billion). Wang Xingxing was also named deputy chair of the new national standardization committee for humanoid robots, a position that signals both political access and industry influence.

The buyer profile tells a structural story. State-owned China Mobile awarded Unitree and AgiBot a joint procurement contract worth 124 million yuan ($17 million) in July 2025: the largest single public order in the domestic humanoid robot sector to date. Unitree’s share was 46 million yuan. China Mobile is both a venture capital investor in Unitree and a buyer of its robots.

Deployment reality: Unitree is the volume leader. It ships more legged robots than any other company on earth. But the G1’s primary market is research and education, not industrial production. The company plans to ship 20,000 humanoids in 2026, up from over 5,500 in 2025. Whether that volume translates into productive deployment or simply more units sitting in university labs is the question investors should be asking. Unitree’s strength is hardware and price. In AI capability and manipulation dexterity, the company trails the ambition of its own pricing strategy.

UBTECH (优必选): The Only Audited Numbers

UBTECH holds a distinction no other Chinese humanoid company can claim: public financial statements. Listed on the Hong Kong Stock Exchange since late 2023, UBTECH is the only major player whose numbers are audited and independently verifiable.

Those numbers tell two stories. The good story: revenue in the first half of 2025 reached 621 million yuan ($87 million), up 27.5 percent year over year. Orders for the Walker S2, UBTECH’s full-size industrial humanoid, exceeded 800 million yuan ($112 million) by November 2025. Major contracts include a 250-million-yuan deal with an unnamed Chinese enterprise, a 159-million-yuan data center deployment in Zigong, and a 126-million-yuan project in Guangxi. The company targets annual production capacity of 5,000 units by 2026 and 10,000 by 2027. Partners include BYD, Geely, FAW-Volkswagen, Audi FAW, BAIC New Energy, Foxconn, and SF Express.

The harder story: UBTECH is still losing money. In the first half of 2025, it reported a net loss of 440 million yuan, narrower than the prior year but substantial. Operating cash flow improved to negative 370 million yuan from negative 427 million yuan. Humanoid robots represent roughly 30 percent of UBTECH’s total sales, up from 10 percent the year before, but the company’s revenue base still includes educational robots, commercial service robots, and logistics systems.

The Walker S2 itself represents a genuine engineering achievement. Standing 176 centimeters with 52 degrees of freedom, it features something no other humanoid offers: autonomous battery swapping. The robot can walk to a charging station, remove its own depleted battery, and install a fresh one without human assistance. This solves the runtime problem that limits every other humanoid to two-to-four-hour operating windows. UBTECH began mass production and delivery in mid-November 2025, shipping several hundred units to partners including BYD and Foxconn factories. Founder James Zhou described it as the world’s first mass delivery of full-size humanoid robots to industrial environments.

In August 2025, UBTECH secured a $1 billion strategic financing credit line from Infini Capital, to be deployed through placements, convertible bonds, and cash withdrawal rights. The company’s share price surged more than 150 percent in 2025, closing at HK$133 in November, with Citi and JPMorgan maintaining buy ratings with price targets above HK$170.

Deployment reality: UBTECH is the closest thing to a verified commercial deployment story in Chinese humanoid robotics. The Walker S2 is on automotive production lines performing real tasks: material handling, palletizing, quality inspection. Internal reports claim a 93 percent success rate on handling tasks and 40 to 50 percent efficiency improvements per cycle. But the absolute numbers remain small. Hundreds of units, not thousands. And the financial losses suggest the unit economics of industrial humanoid deployment have not yet closed.

Galbot (银河通用机器人): The Wheeled Bet

Galbot takes a different approach to the humanoid question. Its flagship robot, the G1, has a human-like torso with two arms mounted on a wheeled chassis with folding legs. The design choice is a statement: legs are expensive to build, hard to control, and unnecessary in most commercial environments. Smooth floors in warehouses, pharmacies, and retail stores do not require bipedal locomotion. Save the R&D budget for the hands and the brain.

Founded in May 2023 by He Wang, a Peking University professor, Galbot has raised $800 million in total funding, including a record-breaking $300 million round in December 2025. Its valuation reached $3 billion, and a Hong Kong IPO is reportedly under consideration. Investors include CATL (the world’s largest battery manufacturer), Beijing Robotics Industry Fund, GGV Capital, CICC Capital, and sovereign-adjacent funds from Singapore and the Middle East. A subsequent 2.5-billion-yuan round in March 2026, led by a national AI fund, was the largest single embodied AI investment announced so far this year.

The deployment model is distinctive. Galbot has launched “Galbot Store,” a fully autonomous retail concept where G1 robots handle entire store operations without human staff. The company claims these stores operate in over 30 cities across China. In healthcare, G1 robots assist at Xuanwu Hospital in Beijing with pharmacy, patient room, and guidance tasks. In industrial manufacturing, Galbot robots operate at CATL battery factories, with the company claiming fully autonomous operation in complex production environments.

Galbot’s technical narrative centers on synthetic data. Founder He Wang has publicly emphasized a strategy of generating high-fidelity simulation data at scale, then transferring learned behaviors to physical robots through sim-to-real techniques. The company claims full-stack in-house development across datasets, embodied foundation models, and hardware.

Deployment reality: Galbot’s claims are ambitious, and independently verifiable evidence is thinner than for the top three. “Orders for thousands of units” comes from press releases, not audited filings or independent research. The CATL deployment and Galbot Store operations provide some evidence of real-world traction, but the scale and autonomy level of these deployments remain unclear from publicly available sources. Galbot is a company to watch, but at a $3 billion valuation on $800 million in funding, the gap between promises and proof is one the IPO prospectus will need to close.

Fourier (傅利叶): The Rehabilitation Bridge

Fourier’s path to humanoids runs through hospitals. Founded in 2015 in Shanghai’s Zhangjiang Hi-Tech Park, the company spent its first eight years building rehabilitation robots and exoskeletons, deploying them in over 2,000 institutions across more than 40 countries. By 2023, overseas revenue from its rehabilitation division had grown more than 50 percent, accounting for about 10 percent of total revenue. This is not a startup chasing a trend. This is a company with an existing commercial robotics business pivoting toward a larger opportunity.

The pivot produced the GR-1 in 2023, which Fourier calls China’s first mass-produced humanoid robot. Over 100 units were delivered to companies across sectors. The GR-2 followed in late 2024, standing 175 centimeters with 53 degrees of freedom, 12-degree-of-freedom dexterous hands, and a battery life doubled from its predecessor. In early 2025, Fourier launched the N1, China’s first verified open-source humanoid. And in 2025 it unveiled the GR-3, a care-focused humanoid with emotional AI capabilities, priced above 200,000 yuan ($27,500) and targeting B2B healthcare clients.

Fourier closed a Series E round of nearly 800 million yuan ($110 million) in January 2025, backed by Guoxin Investment, Pudong Venture Capital, and Saudi Aramco’s Prosperity7 fund. President Xi Jinping personally visited Fourier’s facilities in December 2023, a signal of political importance that few companies in any sector receive.

Deployment reality: Fourier’s rehabilitation heritage gives it a genuine deployment advantage in healthcare. It has real customers, real revenue, and real operational data from years of exoskeleton deployment. But its humanoid production remains small-scale. CEO Alex Gu has been candid about this, stating in interviews that large-scale humanoid production could still be years away. Fourier’s GR-2 is a capable research platform, but the company’s commercial humanoid revenue is negligible compared to its rehabilitation business. The question for Fourier is whether its rehabilitation expertise translates into a humanoid business, or whether the pivot ends up as a distraction from a profitable core.

The Second Tier: Leju, Engine AI, Noetix, and the Rising Wave

Below the top five, a cluster of companies shipped between 100 and 500 humanoid units in 2025. These are not trivial numbers for an industry this young, but the companies remain financially opaque.

Leju Robotics (乐聚机器人), based in Shenzhen, has developed a multi-robot collaboration system powered by Huawei’s HarmonyOS and attracted attention for its Kuavo humanoid platform. Engine AI, also Shenzhen-based, has been aggressive in pricing and production scaling. Noetix (开普勒), a Beijing startup founded in 2023, reported shipping 105 units of its N2 humanoid in a single month (July 2025) and claims to be scaling toward 10,000 units annually. Its robots performed at the 2026 Spring Festival Gala. MagicLab (Wuxi-based) and LimX Dynamics (Shenzhen-based, founded by a former Ohio State professor) round out the rapidly growing cohort.

Each of these companies has raised significant capital and demonstrated functional hardware. What none of them has disclosed is audited financial data, verified commercial deployments, or unit economics. Their existence confirms the depth of China’s humanoid ecosystem. Their opacity confirms how early the industry remains.

The Tech Giant Side-Bets: BYD, Xiaomi, XPeng, Huawei

At least 15 Chinese automakers entered humanoid robotics in 2025, according to the People’s Daily. The logic is simple. Electric vehicle companies already operate the supply chains that humanoid robots need: motors, batteries, sensors, control systems, precision manufacturing. The talent overlap is substantial. And if humanoid robots eventually work in factories, automakers would rather build them than buy them.

BYD has established a dedicated embodied intelligence team and targets deploying 1,500 humanoid robots in 2025, scaling to 20,000 by 2026, according to IDTechEx. BYD already uses Unitree robots in its own production facilities and is simultaneously an investor in AgiBot. Xiaomi unveiled CyberOne in 2022, a 177-centimeter humanoid that recognizes 85 sounds and 45 emotions, but has not disclosed production plans or deployment timelines. XPeng showcased the PX5 at its 2025 AI Day: 178 centimeters, 70 kilograms, over 60 joints. It is already working on XPeng’s own P7+ assembly line. Huawei provides the HarmonyOS platform used by several humanoid manufacturers, including Leju, and multiple automakers are validating Huawei-powered humanoids in their factories.

Deployment reality for all: Pre-commercial. These companies have enormous advantages in supply chain, capital, manufacturing scale, and AI talent. But none has shipped humanoid robots as an independent product line. Their humanoid programs function as strategic R&D investments, hedges against a future where the most valuable product rolling off their assembly lines walks on two legs instead of four wheels. The EV industry parallel is instructive: BYD took decades to go from battery manufacturer to the world’s largest automaker. Humanoid timelines will compress, but the tech giants’ entry into this market is a multi-year bet, not a 2026 story.

What the Map Reveals

Six patterns emerge when the landscape is viewed as a whole.

Pattern 1: Shipment volume and deployment reality are almost entirely disconnected.

The headline number, 13,000 units shipped globally, obscures a critical distinction. The vast majority of units shipped by the two volume leaders, AgiBot and Unitree, are research platforms and data collection tools, not autonomous workers performing productive tasks. The company with the most verified factory deployments, UBTECH, shipped far fewer units. The industry measures success by units shipped because that is the number available. But the number that will matter is units doing paid work autonomously. By that metric, the industry is in the low hundreds worldwide, not the thousands.

Pattern 2: The EV supply chain is the hidden infrastructure advantage.

China’s humanoid robotics boom is not primarily a story about AI. It is a story about hardware supply chains. The same factories that produce motors for BYD’s electric cars produce actuators for Unitree’s humanoids. The same sensor manufacturers, battery suppliers, and precision component makers that built the world’s largest EV industry now service an adjacent sector. This is why Chinese humanoid robots cost a fraction of Western equivalents: not because of lower labor costs, which matter less in precision robotics, but because the supply chain already exists. A Western competitor building the same robot must either source from China or build a parallel supply chain from scratch. Neither option is fast.

Pattern 3: State capital and private capital are deeply intertwined.

Every major Chinese humanoid company has both private venture capital and state-linked investment. Unitree’s investors include Tencent and Alibaba (private) alongside China Mobile and the Beijing Robotics Industry Fund (state-adjacent). AgiBot’s backers include HongShan and Hillhouse (private) alongside BYD (which itself has deep state relationships) and LG Electronics (foreign). The China Mobile procurement contract, which gave orders to both Unitree and AgiBot, came from a state-owned enterprise that is also a venture investor in Unitree. It is the Chinese innovation model: the state creates demand, invests in supply, and extracts strategic value from the resulting ecosystem. Understanding this model is necessary for understanding who wins, because the companies that best serve state priorities will receive the largest procurement contracts, the fastest regulatory approvals, and the most favorable IPO treatment.

Pattern 4: The IPO wave will force transparency.

Three of the top five companies are preparing public listings: Unitree on Shanghai’s Science and Technology Innovation Board, AgiBot in Hong Kong, and Galbot reportedly evaluating Hong Kong as well. UBTECH is already public. These listings will produce the first audited, independently verified financial disclosures for the sector. The prospectuses will reveal actual revenue, unit economics, customer concentration, and cash burn in a way that press releases and industry media estimates cannot. For analysts and investors, the period between now and mid-2026 is the last window of low-information decision-making. After the prospectuses land, the industry’s real economics will be visible.

Pattern 5: The form factor question remains open.

Galbot’s wheeled design, Unitree’s sub-$6,000 compact humanoid, UBTECH’s full-size industrial worker, Fourier’s care-focused companion: these represent fundamentally different answers to the same question. What shape should a general-purpose robot take? The Chinese market is running parallel experiments at a scale no other country matches. Within three years, the data will reveal which form factors generate sustainable commercial demand and which are engineering exercises. That answer will reshape the global industry.

Pattern 6: China is not a monolith. Three competing business models are hiding behind the same label.

Most Western coverage treats Chinese humanoid companies as interchangeable entries in a national race. They are not. Unitree is running a volume-and-price play: flood the market with cheap hardware, treat every unit as a data node, win on ecosystem scale. UBTECH and AgiBot’s industrial line are running a deployment play: prove ROI on factory floors, grow through repeat customers and multi-site expansion. Galbot and AgiBot’s data factory are running an AI-first platform play: the hardware is a vessel for the foundation model, and the brain is the moat, not the body. These three strategies lead to different winners, different losers, and different timelines. Confusing them is the fastest way to misread the market.

What This Means

The map of China’s humanoid robotics industry reveals an ecosystem that is simultaneously more impressive and more fragile than the headlines suggest.

More impressive because the volume is real. China’s companies shipped more humanoid robots in 2025 than the rest of the world combined, and they did it at price points that make deployment economics plausible for the first time. The supply chain depth is genuine. The capital commitment, both private and state-directed, is immense. The speed of iteration, from founding to global shipment leader in under three years, has no precedent in robotics history.

More fragile because the deployment gap between “shipped” and “productively working” remains enormous. Because the unit economics are unproven for every company except UBTECH, and UBTECH is still losing money. Because the forthcoming IPO prospectuses may reveal customer concentration risks, cash burn rates, and revenue quality issues that current press coverage cannot surface. Because “over 140 manufacturers” is a sign of a capital bubble, not a healthy market, and the consolidation has not yet begun.

For the engineer: the technical approaches are worth studying on their own terms. AgiBot’s vision-language-action models, Unitree’s sim-to-real transfer at scale, UBTECH’s autonomous battery swapping, Galbot’s synthetic data strategy. Different constraints and different institutional incentives produce engineering choices that reward close attention, regardless of where you build.

For the founder: pick your model and own it. The landscape rewards clarity. Unitree did not try to build the best humanoid. It built the cheapest one and let volume do the work. UBTECH did not chase volume. It chased factory contracts with auditable ROI. The companies in trouble are the ones trying to be everything at once: a research platform, an industrial deployer, and a consumer brand, all before the first product has proven unit economics. In a market with 140 competitors and a consolidation wave coming, the survivors will be the ones who knew what they were building and for whom.

For the investor: watch the prospectuses, not the press releases. The gap between estimated and confirmed data in this sector is wider than in any other technology industry today. The IPO filings will close that gap. Until they do, every valuation in the space is a bet on narrative, not numbers.

For the curious generalist: the Spring Festival Gala robots doing martial arts flips make for great television. But the real story is in a Zigong data center, a BYD factory floor, and a Shanghai training facility where a hundred robots are learning to fold laundry. The spectacle is not the product. The product is just getting started.

Over ten thousand robots shipped from China alone. The question nobody is asking: how many are working? The honest answer, based on everything the available data can support, is a few hundred. The rest of this decade will determine whether that number stays in the hundreds or reaches the millions. This landscape is where that story begins.

Inside China's Machine. China's AI and robotics ecosystem, from the inside.

Sources

Shipment estimates (AgiBot, Unitree, global totals): Omdia “General-purpose Embodied Intelligent Robots” report, January 2026. Independent, unaudited.

UBTECH financials (revenue, losses, orders, stock): Hong Kong Stock Exchange filings (HKEX: 9880). The only audited data in this article.

AgiBot funding and IPO plans: Bloomberg, Reuters. Unitree financials and IPO plans: CNBC, Reuters, company pre-IPO disclosures. Galbot funding rounds: Caproasia, 36Kr (36氪), company press releases. Fourier product timeline and funding: TechCrunch, Xinhua, company announcements.

Market-level context (140+ manufacturers, government policy, supply chain): South China Morning Post, Rest of World, ChinaPower Project at CSIS, People’s Daily.

All private company valuations are Estimated from most recent funding rounds. Production targets from executives are Projected. Where sources conflict, the article notes the discrepancy.

Where this table with 140 companies? I have my own catalog 800 robo companies worldwide Roboatlas.org