Inside China’s Machine: Cambricon

Once a Huawei Supplier. Nearly Dead in 2019. China’s Most Valuable Stock in 2025. The Chip That Isn’t the Best, But Is the One You Can Buy.

In August 2025, a nine-year-old chip company that had never turned an annual profit briefly became the most valuable stock in China.

Cambricon Technologies, an AI accelerator designer spun out of the Chinese Academy of Sciences, surged past Kweichow Moutai, the state-backed liquor maker that had held the “king of stocks” crown for over a decade, to become the highest-priced share on the A-share market. The stock had doubled that month, climbing from around 700 yuan to nearly 1,500. For a moment, a company that had lost money every year since its 2020 IPO was worth more, per share, than the most profitable consumer brand in the country.

The Chinese internet found the right joke for it. “Baijiu is the past. Chips are the future.” One widely shared pun rewrote Cambricon’s Chinese name, 寒武纪, into 涨武纪, roughly “rise without restraint,” borrowing from a Jin Yong martial-arts hero whose devoted followers believed he could defy any limit.

The market was not pricing Cambricon’s chips. In the first half of 2025 the company booked 2.88 billion yuan in revenue, a staggering number against the 65 million yuan of a year earlier, but still a rounding error next to Moutai’s 62 billion yuan in annual profit. Cambricon’s entire annual revenue would not cover a rounding line in Moutai’s income statement. Yet for a few days in late August, and again in September, the chipmaker’s shares changed hands at a higher price than the liquor giant’s. The market was not valuing the two companies on the same axis. Moutai is priced on earnings that arrive with the reliability of a utility. Cambricon was priced on something harder to put on a balance sheet: its value as a proxy.

It is the only pure-play AI chip company on China’s public markets. Huawei, the strongest domestic AI chip effort, is unlisted. The GPU startups, Biren and Moore Threads and MetaX, were still pre-profit or only beginning to list. That left Cambricon as the single cleanest instrument through which a public-market investor could express a view on one national wager: that China can build its own AI compute and stop depending on Nvidia. When you cannot buy the thing itself, you buy the proxy for the thing, and Cambricon was the proxy. The stock was not a bet on a chip. It was a bet on a policy.

This is the story of why that bet found Cambricon specifically, what the company actually makes, and what its position reveals about the real shape of China’s AI chip ecosystem. The short version: Cambricon does not make the best AI chip in China. Huawei does. Cambricon makes something that in a sanctioned economy matters more, a chip that is good enough and that you can actually buy.

The Chen Brothers and the Academy

Cambricon did not begin in a garage. It began in a state laboratory.

The founders are brothers. Chen Yunji, born 1983, and Chen Tianshi, born 1985, grew up in an intellectual family in Nanchang, Jiangxi, in a home whose library did more of their early education than school did. Chen Yunji skipped grades and entered the University of Science and Technology of China’s “genius youth class,” a program designed to accelerate the country’s brightest students, at fourteen. His younger brother followed him into the same program at sixteen. Both earned computer science doctorates by the age of twenty-four.

They joined the Chinese Academy of Sciences Institute of Computing Technology, where Chen Yunji specialized in semiconductor architecture and Chen Tianshi in artificial intelligence. Around 2010 they began working on a question that seemed quixotic at the time, when Nvidia was still mostly a graphics-card company: could you design a chip specifically for deep learning, rather than adapting general-purpose hardware to the task? The dominant assumption then was that AI would run on GPUs, chips originally built for rendering graphics and repurposed for the parallel math that neural networks happen to need. The brothers bet on a different premise, that a processor designed from the ground up for neural networks, a domain-specific architecture, could be smaller, cheaper, and more power-efficient than a repurposed GPU. Their work produced the DianNao series of neural-network accelerator architectures, an influential academic line, and in 2014 a co-authored paper won the top award at ASPLOS, a leading computer-architecture conference. The recognition mattered: it established the brothers as serious architects of dedicated AI hardware years before the industry agreed such hardware was necessary.

Heading a team of twenty in a thirty-square-meter lab, the brothers built a prototype deep-learning processor in 2015. They named the project Cambricon, after the Cambrian explosion, the geological moment 540 million years ago when life on Earth diversified suddenly and dramatically. The English name fuses “Cambrian” with “silicon.” The brothers were betting their chips would do for artificial intelligence what the Cambrian did for biology.

In March 2016 the Cambricon project spun out of the Academy as a company, with Chen Tianshi as chairman and CEO and Chen Yunji as chief scientist. The spin-out was not a simple startup. It was a joint effort with the Institute of Computing Technology’s own technology-transfer platform, seeded by roughly 10 million yuan of CAS money. This is the whole-of-nation model in miniature: the state acts as incubator, provides the founding intellectual property, and shepherds a strategic asset from the lab into the market. Chen Yunji returned to academia shortly after founding. Chen Tianshi stayed to run the company. His stated philosophy has never been about brand. “People don’t need to know our name,” he has said, “as long as we can support downstream applications.” What he cares about, in his own framing, is mastering the AI chip instruction set as China’s path out of dependence on Western semiconductors. He treats the instruction set not as a corporate moat but as a national imperative.

The Huawei Years and the Near-Death

For its first few years, Cambricon’s entire story was one relationship.

In September 2017, Huawei launched the Kirin 970, which it billed as the world’s first smartphone chip with a dedicated neural processing unit for on-device AI. Inside that silicon, providing the computational horsepower for the NPU, was Cambricon’s 1A processor IP. For a young company spun out of an academy, this was total validation: its technology was designed into a flagship product from a top-tier global smartphone maker and scaled to millions of devices. The Kirin 980 followed. In 2017 and 2018, IP licensing to Huawei accounted for the overwhelming majority of Cambricon’s revenue, by some accounts as much as 98 percent.

Then, in 2019, the relationship ended. Huawei unveiled its own Da Vinci architecture, which would power all of its future AI chips through the HiSilicon subsidiary, and designed Cambricon out of the supply chain. The revenue stream that had been nearly the entire company vanished. By one accounting, licensing revenue collapsed from 117 million yuan to somewhere between 16 and 18 million. The company that had been Huawei’s celebrated partner was, within a single year, facing an existential question.

Chen Tianshi’s response was the pivot that defines the company. Rather than remaining a lightweight IP licensor, Cambricon would become a full-stack chip company with a “Cloud-Edge-End” product portfolio, designing and selling complete accelerators rather than licensing designs to others. This was an enormous, capital-hungry undertaking for a company that had just lost most of its revenue, and it did not pay off quickly. Cambricon went public on Shanghai’s STAR Market in July 2020, raising about 369 million dollars as China’s self-styled “first AI chip stock,” but the losses continued. Five consecutive years of them from the IPO through 2024, accumulating to roughly 3.8 billion yuan. In December 2022 the US added Cambricon to its Entity List, cutting the company’s access to advanced foreign technology and suppliers. In 2023, Cambricon laid off half the staff of its autonomous-driving chip unit. Early investors including Alibaba and SDIC Venture Capital sold their stakes. The share price fell to half its IPO level. The company that would become China’s king of stocks spent the years just before its coronation being described, by its own domestic critics, as the firm best at telling a good story and burning cash, and worst at making money.

What Cambricon Actually Sells

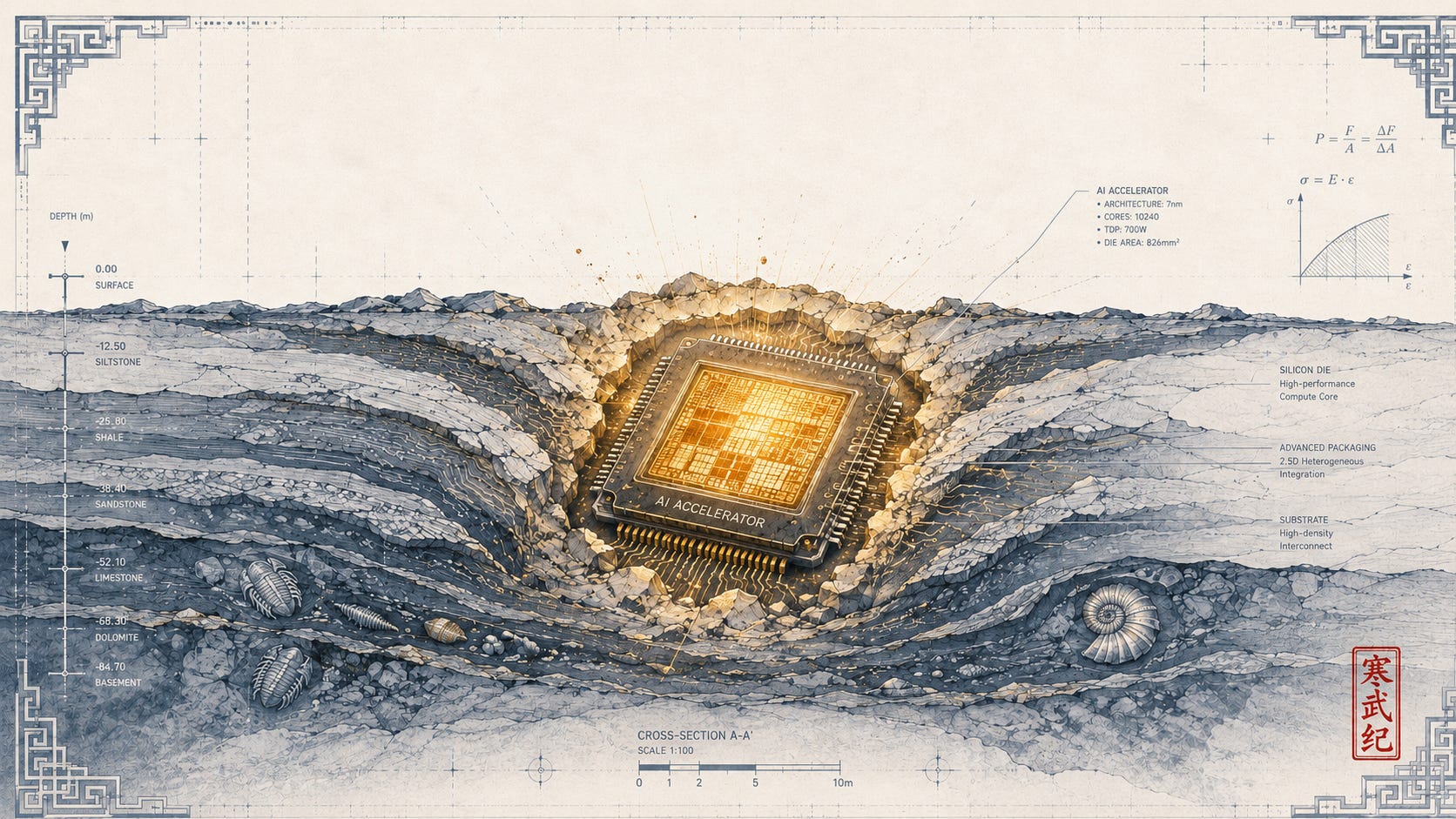

The product that changed everything is the Siyuan 590.

Cambricon designs the Siyuan (思元) line of Machine Learning Unit accelerators. The 590 is its current flagship, and its appeal has almost nothing to do with cutting-edge performance. It carries 80GB of high-bandwidth memory, which is enough to run large language models. It is built for inference, the stage where a trained model generates predictions, rather than for training, the far more compute-intensive stage where models are built in the first place. It works best in mid-size clusters of one to three thousand cards, enough to support real commercial deployments without requiring a supercomputer. It is manufactured at SMIC’s N+2 process, a 7-nanometer-class node built entirely on older DUV lithography rather than the EUV machines that China cannot import.

On raw specifications, the 590 lags Nvidia’s A100, a chip Nvidia introduced in 2020. Independent assessments put Cambricon’s chips roughly four to five years behind Nvidia’s leading parts on performance. Analysts estimate the 590 reaches something like 80 percent of the A100’s performance in certain scenarios, at a lower price than Nvidia’s China-specific H20. But the number that matters is not the performance ratio. It is that the 590 is a chip a Chinese cloud operator can actually purchase and install, in volume, today.

The next-generation Siyuan 690 is still in testing, with large-scale production potentially slipping to the second half of 2026. Because the underlying manufacturing node has not changed, the expected performance gains come from adopting more advanced memory and integrating more compute units rather than from a process leap. This is the central constraint of the whole enterprise: Cambricon is pursuing architectural efficiency because the manufacturing path to raw performance is blocked. It cannot out-spec Nvidia. It can only make chips that are good enough for the workloads that matter most, at a price and availability that Nvidia, locked out of the market, cannot match.

There is a second half to the product that matters as much as the silicon. When Cambricon pivoted from IP licensing to full-stack chips after the Huawei break, it also had to build the software layer that lets developers actually use its hardware. That layer is Neuware, Cambricon’s development stack, the equivalent in its own ecosystem of what CUDA is to Nvidia. Software is where Nvidia’s real moat lives: a generation of AI engineers learned to build on CUDA, and that accumulated tooling and habit is harder to replace than any single chip. Cambricon’s Neuware is far younger and far less mature, and the gap in software depth is as real as the gap in raw compute. But it exists, it works, and for a Chinese developer who cannot use CUDA-locked Nvidia hardware anyway, a less polished domestic stack that runs on available silicon is a trade worth making. The chip and the software together are what Cambricon sells, and both are best understood the same way: not as the best option, but as a working option in a market where the best option is off the table.

The Sanction Economy Made the Market

Cambricon’s turnaround was not primarily an engineering achievement. It was a geopolitical one.

Starting in October 2022, successive waves of US export controls cut China off from Nvidia’s most capable AI hardware. The first round restricted the A100 and H100. Nvidia responded by designing the H800 and later the H20, deliberately throttled parts meant to stay within the rules, and successive tightenings caught those too, along with the L40S and other data-center chips. By 2025 the pattern was clear: whatever Nvidia built for the Chinese market, the controls would eventually reach it. The most capable AI hardware on Earth became something the world’s second-largest AI market could not reliably buy. Huawei, the strongest domestic alternative, faced its own supply constraints.

The vacuum created a rare opening, and Cambricon’s years of stockpiled, unsold inventory suddenly inverted in meaning. What had looked like dead weight on the balance sheet became bargaining power. With Nvidia GPUs out of reach, Cambricon’s ready-to-ship stock became a lifeline for Chinese AI developers, some of whom were reportedly willing to pay a 30 percent premium for immediate delivery. In a post-sanction chip economy, inventory was leverage. A chip you could take delivery of this quarter was worth more than a better chip you could not take delivery of at all.

The financial reversal, when it came, was violent. First-half 2025 revenue of 2.88 billion yuan represented year-on-year growth that the company reported at over 4,300 percent. The cloud product line, the Siyuan accelerators, drove almost all of it. Cambricon closed 2025 with roughly 6.5 billion yuan in revenue, up from 1.2 billion the year before, and its first-ever annual profit, about 2.1 billion yuan against a net loss in 2024. The momentum carried into 2026: first-quarter revenue of 2.88 billion yuan, matching the entire first half of the prior year in a single quarter, with net profit of about 1.01 billion yuan. Gross margins held above 54 percent. Beijing reinforced the tailwind, launching new waves of AI infrastructure spending and building intelligent-computing centers across provinces, and in late 2025 adding Cambricon, alongside Huawei, to a government-approved AI hardware procurement list. That list matters more than it sounds: it channels public-sector and state-influenced demand toward two domestic names, and Cambricon is the only pure-play chip designer on it.

The logic underneath the numbers is the thesis of the entire company. In a normal market, the best chip wins. In a sanctioned market, the best available chip wins. Cambricon did not close the performance gap with Nvidia. The gap stopped mattering, because the better product was not on the shelf. Good enough, in stock, and domestic beat best in class and unavailable. This is not a temporary distortion that will correct when the technology catches up. As long as the sanctions hold, availability is itself a form of performance, and Cambricon’s entire commercial existence rests on that substitution.

The ByteDance Problem

The single largest risk in Cambricon’s business is hidden inside its single greatest strength.

The revenue that transformed the company is extraordinarily concentrated. In the first half of 2025, the top five customers accounted for 94 percent of revenue, and the single largest customer contributed roughly 80 percent. Chinese media have identified that dominant buyer as ByteDance, the parent of TikTok. Caixin reported that ByteDance pre-ordered approximately 200,000 of Cambricon’s Siyuan 590 chips. Bloomberg’s sources describe ByteDance as accounting for more than half of all Cambricon orders, with Alibaba expected to grow into a significant buyer as it scales its own domestic AI clusters.

This is the paradox of a proxy stock. The same hyperscaler demand that produced the 4,300 percent revenue surge also means that a single procurement decision by a single company can swing Cambricon’s year. If ByteDance’s domestic-chip buildout slows, or if it shifts orders toward Huawei, or if it secures Nvidia hardware through some future loosening of controls, the concentration that drove the ascent becomes the mechanism of a fall. Cambricon’s own risk disclosures acknowledge high customer concentration as a material risk. The market that prices Cambricon as a bet on China’s entire AI compute buildout is, at the level of actual orders, often pricing a bet on a handful of ByteDance purchasing decisions.

The concentration is not a sign of weak demand. It is a sign of how the demand is shaped. China’s AI compute buildout is being driven by a small number of enormous spenders, the domestic hyperscalers, each committing tens of billions of yuan to data-center capacity. When one of them decides to route a meaningful share of its domestic-chip budget to Cambricon, the effect on a company of Cambricon’s size is enormous. The same structure that makes a single large order transformational makes the loss of that order existential. Cambricon’s revenue is not diversified across a broad market of buyers the way Nvidia’s is. It is a function of what a few Chinese giants decide to do with the portion of their capex that cannot go to Nvidia. That portion is large and growing, which is the bull case. It is also concentrated and discretionary, which is the risk.

The Manufacturing Ceiling

Cambricon designs chips. It does not make them. And the making is where the ceiling is.

Like Nvidia, Cambricon is fabless: it relies on a foundry to manufacture its silicon. Its foundry is SMIC, and SMIC’s most advanced usable process for these chips is N+2, a 7-nanometer-class node built on DUV lithography. This works, but at a cost. Bloomberg has reported yield rates of roughly 20 percent for Cambricon’s largest dies, meaning that four out of every five chips coming off the wafer fail to meet the targeted criteria. For comparison, mature leading-edge processes elsewhere run yields far higher. Cambricon is trying to scale volume on a node that is both older and materially less forgiving than what its foreign competitors use.

The reported ambition is to ship roughly 500,000 AI accelerators in 2026, including as many as 300,000 of the flagship Siyuan 590 and 690, more than tripling the prior year’s estimated output of around 116,000 units. Whether that is achievable depends less on demand, which is abundant, than on manufacturing. Two constraints bind.

The first is foundry capacity. Cambricon competes for SMIC’s limited advanced-node output against Huawei, whose Ascend accelerators also depend on SMIC, and Huawei is itself planning to roughly double its chip output. There is only so much leading-edge wafer capacity in China, and the country’s two most important AI chip programs are drawing from the same well. SMIC cannot import EUV lithography machines, which means its 7-nanometer-class output is produced through multi-patterning on DUV tools, a slower and lower-yielding process that constrains how many wafers it can push through. Every wafer Huawei takes is a wafer Cambricon does not get, and in that contest Huawei is the larger, more strategically central customer. The capacity Cambricon needs to hit 500,000 units is capacity it does not control and must compete for against a rival with more leverage.

The second constraint is memory. AI accelerators need large pools of high-bandwidth memory to keep their compute units fed, and HBM is dominated by South Korean suppliers, principally SK Hynix and Samsung. China has invested heavily but has not yet produced a competitive domestic alternative at the required specification. Even Huawei’s Ascend chips have relied on HBM stacks from the Korean suppliers. This means a Chinese cloud operator can secure Cambricon chips and still face delays if it cannot pair them with matching memory, and it means Cambricon’s roadmap is hostage to a component it cannot make and cannot fully source domestically. The company must lock in memory procurement early, and any tightening of the global HBM supply, which is already strained by hyperscale demand worldwide, lands directly on its ability to ship.

The manufacturing ceiling is the part of the Cambricon story that the stock price is least equipped to see. Demand can be modeled. Government support can be assumed. But a 20 percent yield on a contested node, paired with an imported-memory bottleneck, sets a hard limit on how many chips actually reach customers, regardless of how many the market wants. A company can have every order it could wish for and still be capped by how many good dies come off the wafer and how much memory it can attach to them.

Cambricon and Huawei in the Stack

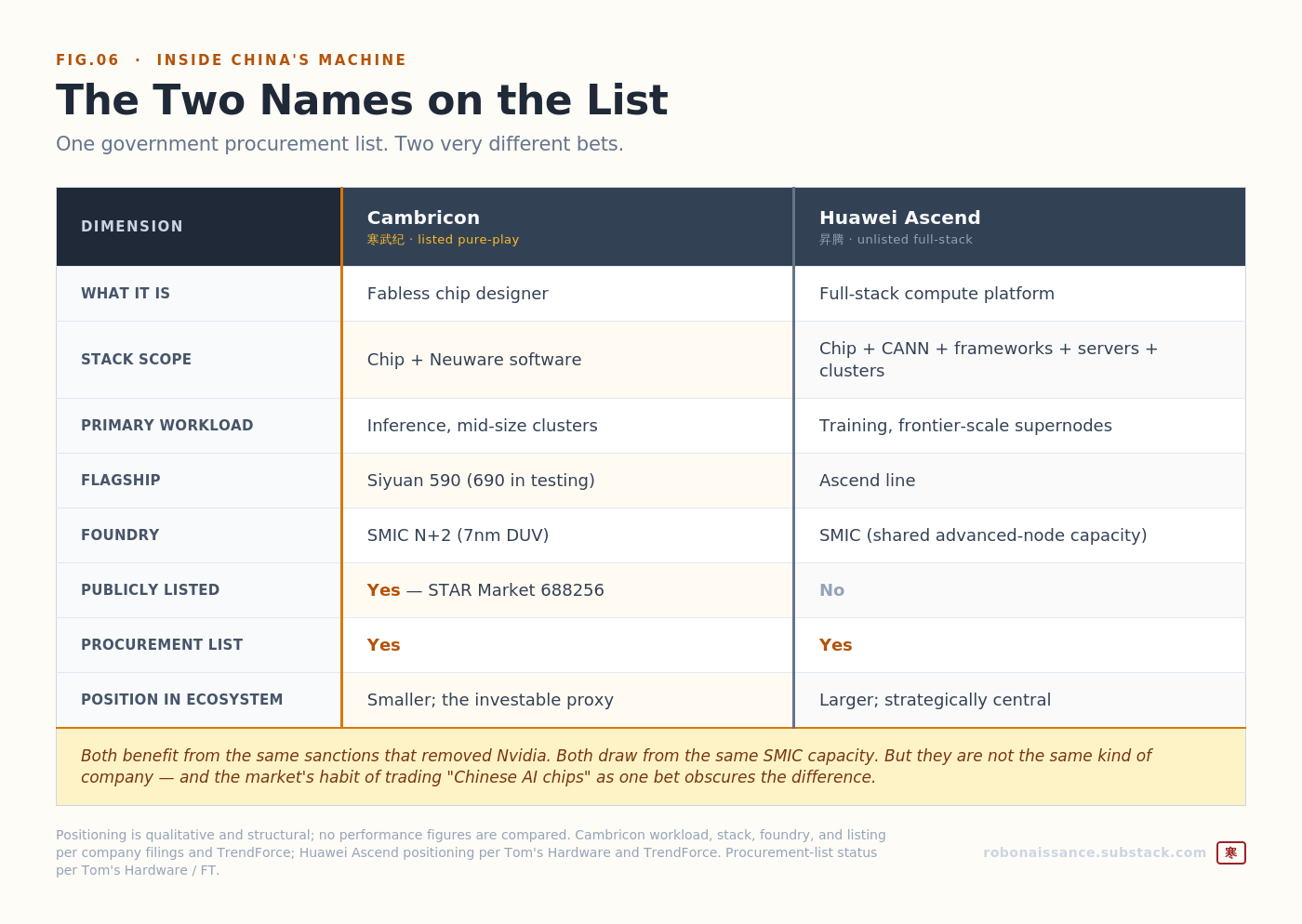

To understand Cambricon’s real position, you have to place it next to Huawei, because the two occupy quite different roles in China’s AI chip ecosystem.

Huawei’s Ascend is a full-stack platform. It spans the accelerator silicon, the CANN software layer that competes with Nvidia’s CUDA, the frameworks above it, and the servers and cluster systems that package thousands of chips into training-grade supernodes. Huawei is building the entire vertical, from the chip to the data center, and aiming it squarely at the most demanding workload: training frontier models. Its Ascend line is the backbone of many in-country training clusters.

Cambricon is narrower and, in a sense, more classical. It is a fabless chip designer with a software stack, Neuware, that provides the developer interface to its hardware, but it does not build servers or clusters or aspire to own the full training stack. Its sweet spot is inference in mid-size deployments. In the language of the ecosystem, Huawei is the full-stack training ambition and Cambricon is the good-enough inference play. Both sit on the government procurement list. Both benefit from the same sanctions that removed Nvidia. But they are not the same kind of company, and the market’s habit of treating “Chinese AI chips” as a single trade obscures the difference.

This division also frames Cambricon’s dependency. It competes with Huawei for SMIC’s wafers while being far smaller and less strategically central to the state than Huawei is. In a genuine capacity crunch, it is not obvious that Cambricon wins the allocation fight. Its position rests on being the listed, investable, pure-play name in a category where the strongest player, Huawei, is unlisted and pursuing a much larger and more integrated ambition.

The inference-versus-training split is the cleanest way to see where each company fits. Training a frontier model requires enormous clusters of the most capable chips, tightly interconnected, running for weeks; this is the hardest problem and the one Huawei’s full-stack Ascend systems are built to attack. Inference, running a trained model to serve users, is less demanding per chip and far more widely distributed across the economy, and it is where the actual volume of AI compute will ultimately sit as models get deployed. Cambricon has chosen the larger, less glamorous half of that market. The DeepSeek moment sharpened the point: when DeepSeek trained its latest model on Nvidia hardware but ran inference on domestic chips, it illustrated exactly the division of labor that favors a company like Cambricon. Training may still reach for the frontier. Inference can increasingly run on good-enough domestic silicon, and that is the half of the workload Cambricon is positioned to capture.

Capability Versus Capture

Strip away the stock-price drama and Cambricon’s story reduces to a single distinction: the difference between capability and capture.

Capability is whether you can build a chip good enough to matter. Cambricon has cleared that bar. The Siyuan 590 is not a frontier part, but it runs real inference workloads for real hyperscalers at real scale, and in a market where the frontier alternative is banned, good enough is a genuine capability. The DeepSeek moment reinforced this: when a leading Chinese model optimizes for domestic silicon, the whole ecosystem’s center of gravity shifts toward chips like Cambricon’s.

Capture is whether you can convert that capability into durable, defensible share of a market whose size justifies your valuation. Here the picture is far less settled. Cambricon’s capture depends on three things it does not fully control. It depends on the sanctions persisting, because a return of Nvidia to the Chinese market on favorable terms would reopen the performance gap that sanctions currently paper over. It depends on winning enough of SMIC’s contested capacity against a larger, more strategically favored Huawei. And it depends on a customer base concentrated enough that a single hyperscaler’s change of plan could reset the entire revenue line.

The market that made Cambricon China’s most valuable stock in 2025 was pricing capture as though it were already achieved. What Cambricon has actually proven is capability. The distance between the two is the distance between a chip that works and a business that compounds, and it is a distance the manufacturing ceiling, the customer concentration, and the geopolitics have not yet let the company close. Cambricon is the clearest window China has into what its domestic AI chip ecosystem can now do. It is also the clearest window into what that ecosystem still cannot do. Both things are true, and the stock price only reflects one of them.

Inside China’s Machine. China’s AI and robotics ecosystem, from the inside.

Sources

Founding and history: Wikipedia (”Cambricon Technologies”); PandaYoo (”The Cambrian Explosion: How Cambricon Became China’s Billion-Dollar AI Chip Powerhouse”); VnExpress (”From youth geniuses to tech founders”); South China Morning Post (”Cambricon: how 2 ‘genius brothers’ created China’s potential rival to Nvidia,” August 2025); Chinadaily (2018). Founding date (March 15, 2016), CAS Institute of Computing Technology spin-out, DianNao architecture lineage, 10 million yuan CAS seed, and ASPLOS 2014 award are confirmed across multiple sources.

Huawei licensing and near-death: PandaYoo; michaelbommarito.com wiki; Wikipedia. Kirin 970/980 IP licensing (2017-2018), the ~98% revenue concentration, the 2019 Da Vinci transition ending the relationship, and the revenue collapse are reported across multiple sources; the specific 117M → 16-18M yuan figures are per michaelbommarito citing EqualOcean.

Products and manufacturing: TrendForce (”Cambricon Remains China’s Top AI Chip Startup,” December 2025); Tom’s Hardware (”Cambricon targets 500,000 AI chips in 2026”); TechRadar; techbuzzchina (”Cambricon: China’s Nvidia—or Nvidia Without the Profits?”). Siyuan 590 specifications (80GB HBM, inference focus, 1,000-3,000 card clusters), SMIC N+2 (7nm) DUV manufacturing, and the Siyuan 690 timeline are per TrendForce and Tom’s Hardware. The 20% yield figure is per Bloomberg via Tom’s Hardware and TechRadar. The 500,000-unit 2026 target (including 300,000 Siyuan 590/690) is per Bloomberg via multiple outlets.

Financials: Bloomberg (”China AI Chip Market Lifts Cambricon to First-Ever Annual Profit,” March 12, 2026, citing the company’s own statement); EqualOcean (”Cambricon Reports H1 2025 Revenue of CNY 2.881 Billion”); hellochinatech (”Cambricon at 348 Times Earnings,” April 2026); BigGo Finance; Investing.com; Futubull; Tom’s Hardware. Full-year 2025 revenue (6.5B yuan, up from 1.2B in 2024) and first-ever annual net profit (2.1B yuan, versus a 452M-yuan loss in 2024) are per Bloomberg citing Cambricon’s statement. H1 2025 revenue (2.881B yuan, +4,347.82%) and net profit (~1.04B yuan) are confirmed across EqualOcean, Futubull, and SCMP. Q1 2026 figures (2.88B revenue, ~1.01B net profit, +185%) are per hellochinatech, BigGo, and Tom’s Hardware. Gross margin above 54% is per Investing.com (TTM 54.99%) and hellochinatech. Five consecutive years of net loss from the 2020 IPO through 2024 (~3.8B yuan cumulative) is per BigGo citing financial filings.

Customer concentration: BigGo Finance (top five customers 94% of H1 2025 revenue, largest ~80%); TradingView/Invezz citing Bloomberg (ByteDance largest customer, >50% of orders); Caixin via BigGo (ByteDance ~200,000 Siyuan 590 pre-order). These are reported figures attributed to Bloomberg and Caixin sourcing, not company disclosures of specific customer names.

Ecosystem and procurement: TrendForce; Tom’s Hardware (”Huawei could seize China’s AI chip crown in 2026”); Financial Times via TrendForce (government procurement list adding Huawei and Cambricon). Huawei Ascend full-stack positioning and the SMIC capacity competition are per Tom’s Hardware and TrendForce.

Classification: Founding history, Huawei licensing relationship, Entity List addition (December 2022), IPO (July 2020), and financial results are Confirmed from multiple sources and public filings. Customer identities (ByteDance, Alibaba) are Reported per Bloomberg and Caixin sourcing and attributed accordingly; Cambricon does not publicly disclose customer names. Manufacturing yield (20%) and 2026 shipment targets (500,000 units) are Reported per Bloomberg sourcing. Performance comparisons to Nvidia (80% of A100 “in certain scenarios,” 4-5 years behind) are analyst estimates and are hedged accordingly. Siyuan 690 mass-production timing (H2 2026) is Reported and subject to manufacturing risk.