Inside China’s Machine: The Platform War

Four Tech Giants. Four Strategies: Super-App, Token Hub, Full Stack, Distribution Flood. No Clear Winner. One Map.

The enterprise software stack in the United States is being reorganized around AI agents. Salesforce sells Agentforce. Microsoft embeds Copilot into every surface of its productivity suite. Google positions Gemini as an agentic layer across Workspace and Cloud. The competitive question is which enterprise vendor owns the layer where AI actually performs tasks.

In China, the same competition is happening with different participants, different distribution, and different stakes. The four companies competing are not enterprise vendors. They are Tencent, Alibaba, Baidu, and ByteDance. Their agent platforms reach consumers through WeChat, Alipay, Ernie Bot, and Doubao. Their enterprise offerings run on their own cloud infrastructure. Their models are owned, not licensed. Every one of them launched a new agent product or a new agent-capable model between January and April 2026, and all four are building agents into consumer super-apps that reach hundreds of millions of daily users. There is no comparable four-company race in any other market.

This article maps the four platforms. Who owns the agent layer in China, what they are betting on, and where each is strong and weak.

No Clear Winner

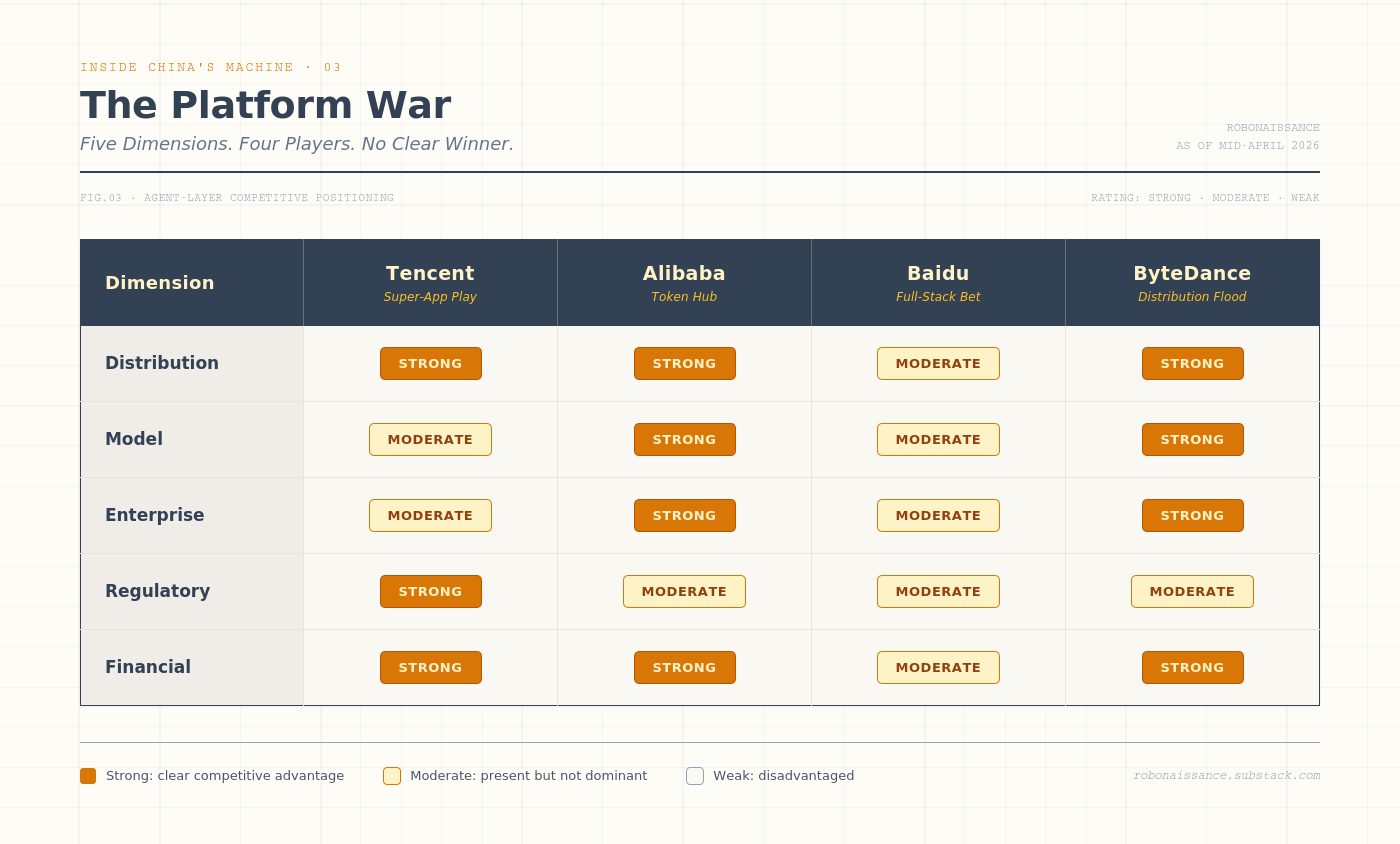

Four dimensions determine which platform wins the agent layer: Distribution (how many users the agent reaches), Model (how capable the underlying AI is), Enterprise (how serious the commercial offering is), and Regulatory (how well the platform navigates China’s security and data governance environment). A fifth dimension, Financial Commitment, captures how much each company is investing in 2026.

Rating scale: strong, moderate, weak. This is a judgment based on reported data as of mid-April 2026. Numbers referenced below are documented in Sources.

No single company leads across all five. The pattern is instructive.

Tencent: The Super-App Play

Tencent’s bet is that AI agents become features of existing super-apps rather than standalone products. The distribution infrastructure is already built. WeChat has roughly 1.4 billion monthly active users and generates over $16 billion in annual app revenue through payments, mini-programs, e-commerce, content, and advertising. The thesis: attach an agent layer to the existing habit, and the agent inherits the scale without needing to acquire users.

The OpenClaw integration made the thesis concrete. On March 22, 2026, Tencent launched ClawBot, a WeChat plugin that appears as a contact within the messaging interface. Users send instructions the same way they message friends. In early April, Tencent Cloud launched ClawPro in public beta, an enterprise AI agent management platform that lets businesses deploy OpenClaw-based agents in ten minutes, with template selection, model switching, token-consumption tracking, and security compliance. During internal beta, ClawPro was adopted by more than 200 organizations across finance, government, and manufacturing.

As of April 2026, Tencent has launched more than ten agent products, including QClaw, WorkBuddy, ClawBot, ClawPro, CodeBuddy, the ADP agent development platform, the SkillHub skill community, and security tools branded as “Lobster Butler” (龙虾管家). Personal desktop tools, enterprise platforms, developer infrastructure, and consumer integrations, all within a single month.

Distribution: Strong. WeChat’s 1.4 billion MAU is the single most valuable distribution asset in Chinese consumer AI. No other platform comes close to its daily habit formation.

Model: Moderate. Tencent’s Hunyuan foundation model (406 billion parameters) lags the capability frontier in public benchmarks. Chief AI Scientist Yao Shunyu, a former OpenAI researcher, joined in December 2025 to close the gap. Hunyuan 3.0 is scheduled for April 2026. The Tencent consumer assistant Yuanbao grew twentyfold in daily active users between February and March 2025, largely because Tencent integrated DeepSeek models to compensate for Hunyuan’s weakness.

Enterprise: Moderate. ClawPro launched in public beta April 3 with 200+ organizations. The product is new. The enterprise cloud business is smaller than Alibaba’s. Tencent holds a smaller share of China’s AI cloud market than Alibaba’s 35.8 percent, although exact rankings shift with reporting source.

Regulatory: Strong. Tencent’s long operational experience with WeChat has built one of the most sophisticated compliance apparatuses in Chinese consumer tech. The “Lobster Butler” branding for security tooling is a tell: Tencent is deliberately positioning its OpenClaw integration as the most governance-ready option as Chinese regulators tighten agent rules.

Financial: Strong. Tencent spent 18 billion yuan on AI products in 2025 and announced plans to at least double that in 2026 (roughly $5 billion). President Martin Lau confirmed on the March earnings call that capital expenditure will rise, with compute earmarked for both internal training and external leasing through Tencent Cloud.

The risk. AI agents could displace super-app behavior. If users start conducting tasks through agents rather than through WeChat mini-programs, Tencent’s distribution advantage becomes a liability rather than a moat. The bet depends on agents remaining features of WeChat rather than replacing it.

Alibaba: The Token Hub

Alibaba’s bet is that tokens, the basic unit of AI processing, are the business. The company reorganized its entire AI operation in March 2026 into the Alibaba Token Hub (ATH), consolidating five previously separate AI units (Tongyi Laboratory, Qwen, Wukong enterprise AI, Alibaba Cloud AI infrastructure, and a research arm) under CEO Eddie Wu’s direct oversight. Wu’s framing in his announcement letter: “ATH is built around a single organising mission: create tokens, deliver tokens and apply tokens.”

The structural logic is coherent. China now processes 140 trillion tokens per day, up from approximately 100 billion at the start of 2024, according to China’s National Data Administration. NDA administrator Liu Liehong used the term 词元 (cí yuán) as the official Chinese translation for “token” at the China Development Forum in March 2026. The character 元 in 词元 means “element” or “base unit” in the NLP sense, but its homograph with 元 (the yuan, China’s currency) has led SCMP and Fortune to frame the choice as invoking token-as-currency. Liu himself called tokens “the settlement unit linking technological supply with commercial demand.” If tokens are the unit of AI economic activity, the company that creates, delivers, and applies the most tokens captures the most value.

Alibaba has three things competitors lack. First, Qwen. Qwen3 is consistently ranked among the world’s top open-source large language models (the AI systems that power modern chatbots and agents) and reaches 300 million monthly active users across Alibaba’s consumer ecosystem (Taobao, Tmall, Alipay, Amap, Fliggy). Second, the Taobao/Tmall/Alipay distribution: a week of 2026 Chinese New Year promotion delivered 140 million first-time AI shopping experiences. Third, the cloud business: Alibaba Cloud holds roughly 35.8 percent of China’s AI cloud market, the largest share among Chinese providers.

The Wukong enterprise platform, launched March 2026, is the commercial vehicle. Wukong coordinates multiple agents handling complex business tasks (document editing, meeting transcription, workflow automation) within a single interface. The architecture is similar to what Tencent’s ClawPro offers, but with Alibaba’s cloud scale and enterprise customer base underneath.

Distribution: Strong. Qwen’s 300M MAU is behind Doubao’s 159M only by aggregation methodology. Counting unique users across Alibaba’s consumer ecosystem, the total reach is higher. Alipay’s 120 million AI-agent transactions in a single week in February 2026 is the clearest data point: Chinese consumers are already making autonomous purchases at scale, and Alipay is the rails.

Model: Strong. Qwen has consistently ranked among the top Chinese open-source models. Alibaba also benefits from its own in-house chip work: in April 2026, the company unveiled a new data center running entirely on its proprietary Zhenwu chips, reducing dependence on foreign compute.

Enterprise: Strong. Alibaba Cloud’s 35.8 percent AI cloud market share, Wukong’s multi-agent enterprise platform, and deep integration with DingTalk (Alibaba’s workplace communication app, comparable to Slack) make Alibaba the most enterprise-ready of the four.

Regulatory: Moderate. Alibaba has faced ongoing regulatory scrutiny since 2021, including the Ant Group restructuring and ongoing anti-monopoly enforcement. The 2024 relationship with regulators has improved, but Alibaba carries more regulatory risk than Tencent. Deployment of agents at consumer scale through Alipay requires navigating both financial services regulation and AI-specific rules.

Financial: Strong. Alibaba’s 2025 AI R&D spend reached 67 billion yuan (roughly $9.4 billion), the largest among Chinese tech companies. The Alibaba Token Hub restructuring consolidates budget and strategic authority. Capital commitment is clear and growing.

The risk. The Token Hub strategy depends on tokens remaining the primary unit of AI economic activity. If agent deployment shifts toward fixed-price subscriptions or outcome-based billing, the token-centric framing becomes less useful. Alibaba also faces the challenge of integrating five previously separate units under a new structure: organizational coherence is never a given.

Baidu: The Full-Stack Bet

Baidu’s bet is vertical integration. The company owns a foundation model (ERNIE 5.0, multimodal, 2.4 trillion parameters), its own AI chips (Kunlunxin M100 launching early 2026, M300 in 2027), its own cloud platform (Qianfan), its own consumer interface (Ernie Bot, branded domestically as Wenxiaoyan), and its own agent development platform (AgentBuilder). It also owns the largest autonomous driving business in China: Apollo Go has completed 17 million rides, runs 250,000 weekly rides fully driverless, and operates in 22 cities.

The thesis: in a compute-constrained environment, the platform that owns chips, models, cloud, and applications end-to-end captures the most margin. Baidu is replicating Google’s vertical integration strategy at smaller scale.

ERNIE 5.0, unveiled at Baidu World 2025 in November, is natively multimodal (text, images, audio, video trained jointly from scratch). Baidu’s own benchmarks claim ERNIE 5.0 is competitive with Gemini, GPT-5, and DeepSeek across language, audio, and visual tasks, though independent benchmarks show mixed results. The ERNIE agent products (GenFlow for general-purpose, Famou for self-evolving agents, Oreate for AI workspace) cover personal, enterprise, and developer tiers.

Baidu was also the most visible promoter of consumer OpenClaw adoption. Installation events at its Beijing headquarters drew hundreds of attendees, and its OpenClaw-based agent suite spans desktop software, cloud services, mobile tools, and smart home devices. The full-stack approach: every layer of the agent stack is a Baidu product.

Distribution: Moderate. Ernie Bot reached 200+ million users by April 2024 and continues to grow, but the distribution is weaker than Tencent’s or Alibaba’s. Baidu Search remains China’s largest search engine, which provides one distribution channel. Apollo Go provides another, but neither has the 1.4 billion user scale of WeChat or the 300 million-plus of Qwen and Taobao.

Model: Moderate. ERNIE 5.0 ranks competitively in Chinese benchmarks (ranked No. 1 in China and No. 8 globally on LMArena’s text benchmark, a community-run leaderboard where users compare model outputs head-to-head, as of January 2026) but lags Qwen3 and Doubao-Seed-2.0 in some comparisons. Chinese AI coverage consistently places ERNIE behind Qwen in open-source impact.

Enterprise: Moderate. Qianfan cloud is the smallest of the three major Chinese clouds (Alibaba, Tencent, Baidu by market share). AgentBuilder has strong developer adoption (50,000+ developers, 30,000+ agents by mid-2024) but commercial scale is limited compared to Alibaba Cloud’s enterprise customer base.

Regulatory: Moderate. Baidu’s position is neither advantaged nor disadvantaged. The autonomous driving business operates under specific regulatory frameworks that provide some advantages in city-government relationships. Ernie Bot was among the first Chinese chatbots to receive regulatory approval in 2023, which suggests established compliance processes.

Financial: Moderate. Baidu’s AI-powered business reached 43 percent of core revenue in Q4 2025, up from 26 percent a year earlier. Total AI spend is smaller than Alibaba’s or Tencent’s in absolute terms. The Kunlunxin chip investment is significant but concentrated: Baidu is spending on chip development while peers spend on cloud buildout.

The risk. Full-stack vertical integration requires sustained excellence at every layer. If ERNIE falls behind Qwen and Doubao in capability, if Kunlunxin chips underperform NVIDIA alternatives, if Apollo Go fails to reach profitability, Baidu’s strategy fragments. The full stack is a strength when it works and a weakness when one layer slips.

ByteDance: The Distribution Flood

ByteDance’s bet is quantitative scale. Doubao is China’s largest AI application by monthly active users (159 million). Daily token usage surged to 16.4 trillion as of mid-2025, a 137-fold increase since Doubao’s May 2024 debut. Volcano Engine, ByteDance’s enterprise cloud arm, commanded 46.4 percent of China’s public cloud large model service market as of mid-2025, according to IDC, more than Baidu AI Cloud and Alibaba Cloud combined in that specific segment. This metric measures model API consumption, a narrower slice than the broader AI cloud market where Alibaba leads.

The strategy: make tokens radically cheap, integrate AI into every ByteDance product surface (Douyin, Jimeng, Lark, TikTok internationally), and let volume compensate for margin. Doubao enterprise tokens launched in 2024 at 99.3 percent below the industry average. Volcano Engine’s 2024 revenue was over 12 billion yuan, targeting 25 billion yuan in 2025. The 2030 target: 100 billion yuan.

The agent strategy has three layers. First, Doubao itself serves as both consumer AI app and API-accessible model. Second, Coze (扣子) is ByteDance’s agent development platform, allowing developers to build applications that integrate with Doubao, Lark, and third-party tools. Coze Studio and Coze Loop were open-sourced in 2025, gaining over 10,000 GitHub stars in three days. Third, Coze Space is an agentic collaboration platform with general-purpose agents (which ByteDance internally describes as “inexperienced interns”) and Expert Agents for specialized domains like user research and financial analysis.

ArkClaw, released by Volcano Engine during the OpenClaw boom, is a browser-native OpenClaw variant that eliminates the need for local installation. The design choice is characteristic: ByteDance optimizes for the broadest possible user access rather than for depth of integration.

Distribution: Strong. Doubao’s 159M MAU, Douyin’s 700M+ daily active users in China, and TikTok’s global reach add up to the largest addressable user base among the four. ByteDance’s autonomous commerce capability (Doubao can open JD.com, Taobao, Pinduoduo, and Douyin Mall simultaneously, compare prices, and complete a purchase in under 30 seconds) operates at a speed and cross-platform scale that Western consumer agents have not yet demonstrated.

Model: Strong. Doubao-Seed-2.0 is positioned against GPT-5.2 and Gemini 3 Pro. ByteDance’s internal benchmarks show Doubao leading Chinese peers in instruction following and tool invocation (the capabilities that matter most for agents). Token pricing is the most aggressive in the industry.

Enterprise: Strong. Volcano Engine’s 46.4 percent market share in public cloud large language model services is the dominant Chinese position. Enterprise integration with Lark (domestically branded Feishu, ByteDance’s workplace productivity suite) provides a software entry point that Tencent and Alibaba struggle to match. 2024 revenue of 12+ billion yuan on track to more than double in 2025.

Regulatory: Moderate. ByteDance has faced sustained regulatory pressure from both the Chinese government (on Douyin content moderation) and the US government (on TikTok’s ownership structure). The dual-regulator exposure creates ongoing distraction and potential forced restructuring. The February 2026 suspension of ByteDance’s Seedance 2.0 feature that turns facial photos into personal voices, over concerns about misuse, illustrates the responsiveness to regulatory signals.

Financial: Strong. ByteDance’s revenue has been growing fastest among the four. Volcano Engine’s trajectory from 12 billion yuan (2024) to 100 billion yuan target (2030) represents roughly an eightfold capital commitment. ByteDance is privately held and does not disclose consolidated AI spend, but inferred capital commitment exceeds Baidu and is comparable to Tencent.

The risk. ByteDance’s agent platform is distribution-led rather than ecosystem-led. If consumer AI agent adoption plateaus (as the OpenClaw aftermath suggests it might), ByteDance’s 159M MAU advantage shrinks. The enterprise strategy through Volcano Engine requires sustained technical credibility that competes with Alibaba Cloud’s longer track record. And the US TikTok situation remains an ambient risk to global strategy.

Model Suppliers: The Second Tier

The Big Four own platforms. A second tier of Chinese AI labs supplies models that run on those platforms, or competes directly for enterprise deployment. These companies are not playing the platform game, but they shape the platform war by providing the frontier model capabilities that platforms either absorb or license.

Zhipu AI (智谱): Tsinghua-originated, roughly $2 billion valuation as of 2025, preparing an IPO. GLM-5 Turbo launched February 12, 2026, built specifically for OpenClaw integration. Stock surged 25+ percent on the announcement; market cap crossed HK$100 billion. Strong Chinese government and academic relationships. Competes for enterprise deployments against Alibaba’s Qwen.

MiniMax: Founder Yan Junjie. M2.5 coding model launched February 2026, positioned as production-grade tool rather than chatbot. Stock rose 20+ percent on announcement; market cap crossed HK$100 billion. Operates Talkie (international companion chatbot, ~$70M revenue in 2024). Strategic pivot: from foundation model training to application-layer products, reducing cost and accelerating time-to-market.

Moonshot AI: Kimi chatbot, 13+ million users. $3.3 billion valuation. Kimi K2.5 launched January 2026 with video generation and agentic capabilities. Backed by Alibaba and Tencent (Moonshot is the canonical example of platform companies investing in model suppliers rather than competing directly). Focus on long-context processing, positioned as complementary to platform offerings.

DeepSeek: The one non-platform Chinese AI company to have moved global markets. Provides open-source models that Chinese platforms (especially Tencent, which integrated DeepSeek into Yuanbao) use to supplement their own foundation models. Commercial structure less transparent than peers. Relationship to the platform war: infrastructure provider rather than competitor.

01.AI: Kai-Fu Lee’s venture. Less public presence in the agent race, but foundation model work continues.

The second-tier pattern is consistent. These companies either supply models to the Big Four (Moonshot, DeepSeek) or compete for adjacent segments (Zhipu’s enterprise, MiniMax’s coding) rather than trying to become platforms themselves. Becoming a platform in China requires distribution infrastructure that takes decades to build. The model suppliers are smart not to try.

What This Pattern Reveals

The Chinese agent platform war differs from the US agent war in three structural ways.

First, consumer-first rather than enterprise-first. US agents deploy through enterprise software (Salesforce Agentforce, Microsoft Copilot) and reach consumers through employer mandates. Chinese agents deploy through consumer super-apps (WeChat, Alipay, Douyin) and reach enterprises through the same platforms extended into business surfaces. The direction of travel is reversed. The implication: Chinese agent capabilities get tested against consumer behavior before being hardened for enterprise, while US capabilities get tested against enterprise requirements before being adapted for consumer.

Second, open-source at the foundation. Every major Chinese platform has adopted OpenClaw, open-sourced its own agent development tools (Coze Studio, Coze Loop), and committed to open-weights models (Qwen, ERNIE). The competitive moat is not the framework. It is the distribution, the enterprise tooling, and the integration into local workflows. US agent platforms compete at both layers: proprietary frameworks plus proprietary distribution.

Third, state-adjacent development. Chinese central government restrictions on OpenClaw use in state-owned enterprises and banks, Ministry of State Security security manuals, 15th Five-Year Plan targets of 10 trillion yuan in AI industry size by 2030, local government subsidies in Shenzhen and Wuxi, the National Data Administration’s designation of 词元 as the official term for token: all of this shapes how Chinese platforms build agent products. US platforms operate under regulatory pressure (California AI laws, EU AI Act) but not within an industrial policy framework. The Chinese platforms that navigate regulatory environment best (currently Tencent, with its security-first positioning) capture advantages that are not technical.

Three implications for readers of this series.

For the engineer: The platform choice for agent deployment in China is primarily a distribution decision, not a model decision. All four platforms offer comparable agent capability on paper. The differentiator is how many users your agent reaches, what data it can access, and what ecosystem it integrates into. Build on WeChat for consumer reach, on Alibaba Cloud for enterprise scale, on Volcano Engine for token economics, or on Baidu for integrated compute. The model underneath is largely interchangeable.

For the founder: The defensible positions are narrow. Building a better agent framework will not matter: the Big Four have absorbed OpenClaw and will absorb whatever comes next. Building a better consumer-facing agent will not matter: the Big Four have distribution advantages that no startup can overcome at scale. The opportunities are in vertical applications (specific industry workflows where platform companies under-invest), in model specialization (following Moonshot and Zhipu into long-context, coding, or domain-specific models), or in international markets where Chinese platforms face regulatory barriers.

For the investor: The Big Four’s market capitalization already prices in significant agent-related upside. The interesting opportunities are in the second tier. Zhipu and MiniMax crossing HK$100 billion on agent-model announcements is a preview: model suppliers that can demonstrate enterprise traction will outperform platform companies whose agent economics are diluted by free consumer offerings. Alibaba’s 35.8 percent AI cloud market share is a structural advantage that should compound. Tencent’s double-down on AI spend (36 billion yuan planned for 2026) is a commitment worth tracking against delivery.

The Platform Layer Is the Prize

In the 2010s, the dominant platform layer was cloud infrastructure. AWS, Azure, and Google Cloud split the American market. Alibaba Cloud, Tencent Cloud, and Baidu Cloud split the Chinese market. The dominant cloud provider captured the economics of every application built on top.

The late 2020s will likely be defined by a similar platform war, but at the agent layer rather than the cloud layer. The agent layer sits above the cloud: agents orchestrate tool calls, manage context, and deliver outcomes that enterprise and consumer applications consume. The company that owns the agent layer owns the economic returns from every application that runs agents.

In China, the agent layer is being claimed by four companies with different strategies, different strengths, and different exposure to regulatory risk. None of them has yet locked in dominance. As of mid-April 2026, Alibaba and ByteDance lead on technical and financial commitment, Tencent leads on distribution and regulatory positioning, and Baidu competes on full-stack vertical integration from a weaker distribution base.

The race will resolve over the next eighteen to thirty-six months. By then, the platform war will have produced a clear hierarchy, and the economics of Chinese AI will be reshaped accordingly.

Inside China’s Machine. China’s AI and robotics ecosystem, from the inside.

Sources

Platform company strategies and product launches: Reuters, CNBC, Bloomberg, South China Morning Post, The Next Web, Fortune, KrASIA, TMTPOST, BigGo Finance, IndexBox. Tencent ClawPro launch (April 3, 2026) via Tencent Cloud official announcement and SCMP. WeChat ClawBot (March 22, 2026) via Reuters and PYMNTS. Alibaba Token Hub restructuring via Fortune (April 2026). ByteDance Coze and Doubao details via TechNode, KrASIA, TMTPOST. Baidu ERNIE 5.0 and full-stack strategy via Baidu World 2025 keynote, InfoWorld, eWeek.

User metrics: Double V Consulting (Doubao 159M MAU, Qwen 300M MAU). Fortune (140 trillion tokens/day in China, up from 100B at start 2024). Chinese New Year AI shopping data (Alipay 120M transactions in a week of February 2026) from Double V.

Market share data: 2025 IDC data on public cloud LLM market (Volcano Engine 46.4% as of mid-2025). Alibaba 35.8% AI cloud share via The Next Web ClawPro coverage (April 2026) citing industry data. Note: market share rankings shift with methodology and segment definition. Alibaba, Tencent, and Baidu are the three largest Chinese cloud providers by different measures.

Financial commitments: Tencent 18 billion yuan AI spend 2025, planned to double in 2026, via Martin Lau statements and Tencent earnings. Alibaba 67 billion yuan R&D spend 2025 via Second Talent industry reporting. Volcano Engine revenue 12+ billion yuan (2024) and 25 billion yuan (2025 target) via TMTPOST. Baidu AI-powered business 43% of core revenue (Q4 2025) via Baidu earnings.

Model capability benchmarks: LMArena rankings for ERNIE 5.0 (No. 1 in China, No. 8 global on text benchmark, as of January 2026) via ERNIE Blog. Doubao-Seed-2.0 positioning against GPT-5.2 and Gemini 3 Pro via TechNode (February 2026). Zhipu GLM-5 and MiniMax M2.5 announcements (February 12, 2026) via BigGo Finance.

Model supplier data: Moonshot AI valuation ($3.3B) and Kimi user base via Second Talent. Zhipu AI ($2B+) and MiniMax stock surges via BigGo Finance. DeepSeek context via Fortune and CNBC.

Government and regulatory context: 词元 (cí yuán) term designation from National Data Administration administrator Liu Liehong’s speech at China Development Forum 2026 (March 23-24, 2026) via SCMP, Fortune, PANews, China Daily. 15th Five-Year Plan AI industry target of 10 trillion yuan by 2030 via Vision Times. MIIT security guidelines and MSS “Lobster Safety Farming Manual” (March 2026) via multiple Chinese state media sources.

Classification of data points: User counts and token volumes are Confirmed (company disclosure or state regulator data). Market share percentages are Estimated (third-party research, methodology varies). Financial commitments are Projected (announced plans rather than reported results). 2030 targets (ByteDance 100B yuan, China AI industry 10T yuan) are Projected.