Inside China’s Machine: Unitree

Filed for a $7 Billion IPO. The Price Destroyer. 5,500 Humanoids Shipped. Now Profitable. Waiting on a Brain.

On March 20, 2026, Unitree filed for an initial public offering on Shanghai’s STAR Market (科创板) seeking to raise 4.2 billion yuan ($610 million). Reuters and other market reports estimate a target valuation of 40 to 50 billion yuan (approximately $7 billion), though the prospectus itself does not disclose a valuation figure. The prospectus revealed numbers that no other humanoid robotics company has matched in public disclosure. 2025 revenue of 1.708 billion yuan, up 335 percent year-on-year. Net profit attributable to shareholders of 288 million yuan (up 204 percent), with adjusted net profit excluding non-recurring items of approximately 600 million yuan (up 674 percent). Humanoid shipments of 5,500 units in a single year, which Unitree reported as 32.4 percent of the global market. Omdia’s separate January 2026 report had placed AgiBot first with 5,168 units and Unitree second with 4,200; the prospectus’s higher figure likely reflects later Q4 deliveries, and Unitree and AgiBot are effectively tied at the top. The prospectus also shows the path to profitability was not linear: net losses of 22.1 million yuan in 2022 and 11.1 million yuan in 2023, followed by Unitree’s first scaled profit year in 2024 (94.5 million yuan), and 105.3 million yuan in the first nine months of 2025 before the surge to year-end. Early investors have publicly described Unitree as “profitable since 2020,” but the formal financial disclosures show the breakthrough was 2024, with humanoid revenue scaling above quadruped for the first time.

The founder, Wang Xingxing (王兴兴), is 36 years old, was born in Ningbo, and built his first quadruped robot as a master’s thesis at Shanghai University in 2013. He now controls 68.78 percent of the voting rights in what may become the first humanoid robotics company to trade on a major Chinese exchange. He has spent 2026 navigating the most intense year of his career: a Spring Festival Gala performance watched by hundreds of millions, an IPO acceptance under the STAR Market’s new preliminary review mechanism, an on-site regulatory inspection twelve days later, and a product line that now spans five humanoid models priced from $4,290 to $90,000 plus.

This is the story of how a 50-square-meter office in Hangzhou built one of the two highest-volume humanoid robot operations in the world by being ruthless about cost, how an academic supplier became a national symbol, and why the same business model that made Unitree profitable may also be the ceiling it cannot break through without building something it has not yet demonstrated: a capable embodied intelligence.

The Engineer Who Won Twice

Wang Xingxing’s biography reads like a prepared legend, and in Chinese tech media it has been retold often enough to acquire mythological texture. Born 1990 in rural Ningbo, Zhejiang. Undergraduate at Zhejiang Sci-Tech University (浙江理工大学), a regional school not in the top tier. Master’s at Shanghai University (上海大学), also not top tier. Built XDog, a quadruped robot, as his 2016 master’s thesis. The robot became a Bilibili sensation, attracted early investors and buyers, and gave Wang his way out of academia.

He took a job at DJI in 2016 after graduation, then resigned within months to start Unitree in a 50-square-meter office in Hangzhou’s Binjiang District (滨江区) on August 26, 2016. His co-founder and college classmate Chen Li (陈立) had been running international sales at Hikvision (海康威视), the Hangzhou-based surveillance giant that built one of China’s most successful overseas B2B operations before being added to the US Entity List. Chen brought the playbook. Unitree started shipping internationally in 2018. Between 2022 and 2024 overseas sales exceeded domestic revenue, with overseas falling to roughly 39 percent of revenue in the first nine months of 2025 per the prospectus.

Wang’s voting control (68.78 percent through direct, indirect, and special-voting-rights arrangements) keeps founder authority exceptionally high at IPO. The shareholder list is a small gallery of Chinese industrial and financial power: Meituan (9.6 percent), HongShan Capital/HongShan China (7.1 percent), Matrix Partners China (5.5 percent), plus investments direct or indirect from Tencent, Alibaba, Ant Group, Xiaomi, and ByteDance. Industrial backers include BYD and Geely. State-backed funds from Shanghai and Beijing also participated. Lei Jun’s Shunwei Capital has been in since early rounds and has publicly thanked Wang in person. The return on that Xiaomi-affiliated investment is now one of Lei Jun’s most celebrated bets.

Wang sat in the front row at President Xi Jinping’s high-profile business symposium in February 2025, alongside Jack Ma and other Chinese tech founders. Being in that row places a company in a specific political category. Unitree has since been positioned consistently by state media as a national champion of embodied intelligence (具身智能), the term China’s 15th Five-Year Plan identifies as a strategic industry alongside quantum computing, 6G, nuclear fusion, and brain-computer interfaces.

The Price Destroyer

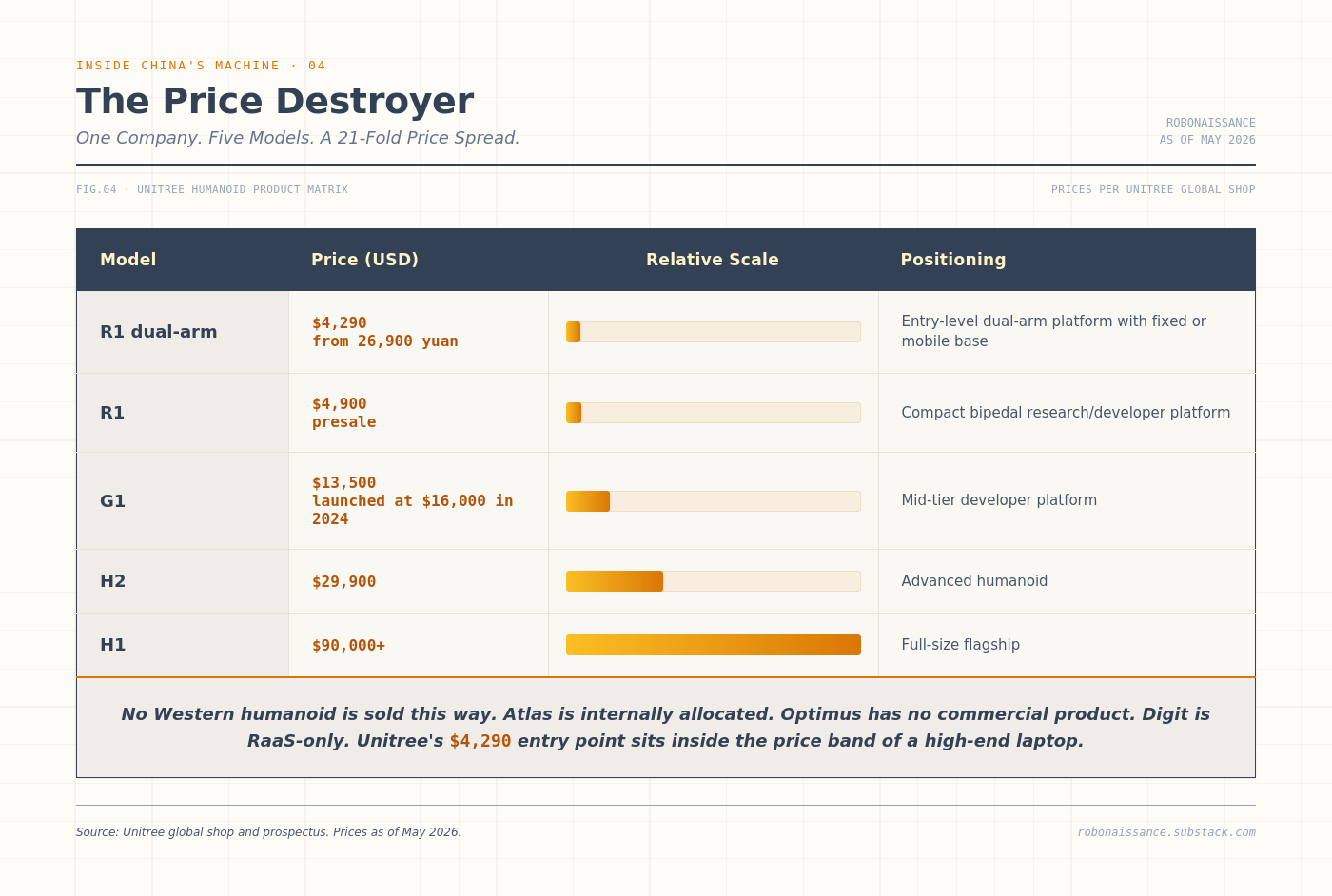

Unitree ships five humanoid robot models, alongside the quadruped lineup that built the company. Official and current prices from Unitree’s global shop:

On April 30, 2026, Unitree extended the R1 line downward with a dual-arm-only variant starting at 26,900 yuan, roughly $4,290. The new entry-level configuration abandons full bipedal architecture in favor of a fixed base or mobile chassis paired with one or two arms (5 or 7 degrees of freedom each, total 15 to 31 DoF), with optional Nvidia Jetson Orin compute. The same day, the company opened its first direct-sales retail store in Beijing’s Wangfujing commercial district. Both moves extend the price-destroyer thesis. The new R1 dual-arm puts a humanoid manipulation platform inside the price band of a high-end laptop, and Wangfujing positions Unitree to sell directly to walk-in retail customers, not just researchers and enterprises.

The pricing numbers tell the story of the business. The G1, launched at $16,000 in 2024, now sells for $13,500 after eighteen months of manufacturing learning. That is less than a premium mountain bike. A university robotics lab can put it on a purchase order; a PhD student can buy one with grant money. No Western humanoid is sold this way. Boston Dynamics’ production Atlas is not on the market: all 2026 units are committed to Hyundai’s factories and Google DeepMind’s research. Tesla’s Optimus has no commercial product. Agility Robotics’ Digit is deployed through Robots-as-a-Service contracts with monthly fees, aimed at logistics operators rather than individual buyers. Unitree is not competing on price against these companies. It is operating in a different product category entirely: a humanoid you can actually purchase, for research, development, or demonstration, without a procurement officer and a multi-year contract.

The pricing is not achieved through subsidy or loss-leader strategy. The 2024 breakthrough year showed how the model finally compounded: gross margin expanded from 44.2 to 56.4 percent even as revenue grew nearly two and a half times, with 2025 adjusted net profit then growing 674 percent year-over-year per the prospectus. The prospectus reveals how.

Vertical integration of hardware. Except for chips, almost all of Unitree’s robot hardware is designed and manufactured in-house, including motors and reducers (the gearboxes that translate motor rotation into joint movement). The GO-M8010-6 motor, a core component, retails at $369. A Boston Dynamics equivalent component is neither sold publicly nor priced comparably. Chen Li, in a 2024 TechNode interview, described in-house component design as “our most fundamental competitive advantage.” The prospectus confirms: vertical integration is the margin source.

Manufacturing discipline. Reduce the number of wires. Reduce chips. Reduce screws. Design for assembly. The Hangzhou operation applies standard Chinese consumer-electronics manufacturing discipline to humanoid robots, the same cost-engineering that made DJI dominant in drones. Wang’s short stint at DJI in 2016 before founding Unitree is underrated in most retellings: he absorbed DJI’s approach and transferred it to bipedal robotics.

Supply chain leverage. Zhejiang province is home to dozens of precision component manufacturers that supply the broader Chinese robotics industry. Unitree buys at scale from suppliers geographically adjacent to its own factory. Alibaba’s ecosystem and the broader Zhejiang industrial base provide the supporting infrastructure.

The result: Unitree has effectively created a product category that did not previously exist, a humanoid robot accessible to individual researchers, universities, and hobbyists, at a price point that fits inside a single research grant. In the quadruped market, where the category is mature and Western competitors do sell comparable products commercially, the price delta is stark: Boston Dynamics’ Spot quadruped sells for $74,500, while Unitree’s Go2 sells for under $2,000 at base configuration. This is a direct comparison between two products sold through the same channels to the same customers. The thirty-fold price delta has collapsed the quadruped research market into near-monopoly: Unitree holds 60+ percent global market share in quadrupeds per Omdia and other third-party research. Whether the same thing happens in humanoids depends on whether industrial deployment becomes a separable market from research and development, or whether Unitree’s category-defining affordability eventually extends into the factory floor where Atlas and Digit are trying to operate.

Who Actually Buys These Robots

The IPO prospectus breaks down Unitree’s customers with unusual clarity. The picture that emerges is narrower than the brand suggests.

Universities and research institutions remain the largest customer category. The prospectus documents 71 order records from universities, representing roughly half of Unitree’s business by transaction count. Chinese institutions include Sun Yat-sen University (中山大学), Southern University of Science and Technology (南方科技大学), and Shenzhen University (深圳大学). International institutions span European and North American research labs across robotics, reinforcement learning, and embodied AI. The China Select Committee’s May 2025 call to add Unitree to the US Entity List was motivated in part by concern that Unitree’s quadrupeds have become the default research platform in US academic robotics labs.

State-owned enterprises and government agencies became the fastest-growing customer category in 2025. Applications include power-grid inspection (where quadrupeds replace humans in hazardous electrical environments), subway tunnel inspection, gas pipeline monitoring, and “guided tour and performance” deployments in offline cultural and tourism venues. In mid-2025, Unitree and Zhipu Robotics jointly won a 124 million yuan China Mobile procurement contract for humanoid biped robot OEM services spanning 2025-2027. Unitree’s share was 46.05 million yuan for small-form humanoid robots, computing backpacks, and five-finger dexterous hands. The customer was a subsidiary of China Mobile; the application was enterprise reception and tour-guide duties in business halls.

Enterprise pilots are the smallest category by revenue but the one with the largest long-term strategic implication. Unitree humanoid industry-application revenue comes mainly from enterprise reception and tour-guide use (50-70 percent), intelligent manufacturing, and intelligent inspection. JD.com (京东) is Unitree’s largest individual corporate customer for quadrupeds. Actual factory floor deployment of humanoids remains limited. Tech Buzz China, in its April 2026 analysis of the prospectus, noted that “real factories require 95 to 99 percent uptime; current humanoids manage about 90 minutes” of continuous operation before battery swap or software intervention.

Consumer and entertainment buyers drove the fastest revenue growth in 2025. Consumer quadruped sales nearly quadrupled year-on-year in the first nine months of 2025. Entertainment events, marketing demos, and the Spring Festival Gala appearances have produced a secondary revenue stream through rental and performance contracts. This is the revenue the brand is built on, but it is not the revenue that will sustain the 2030 valuation implied by the current IPO target.

Three facts about the customer mix deserve emphasis. First, the top five customers represent only 10.6 percent of revenue per the prospectus, signaling unusually healthy diversification. Second, 115 winning bids across Chinese public procurement platforms through 2025 confirm the state-sector integration. Third, overseas sales were 39 percent of revenue in the first nine months of 2025, down from above 50 percent in earlier years. Unitree is not a domestic-only story even as US policy pressure intensifies.

The Technology Position

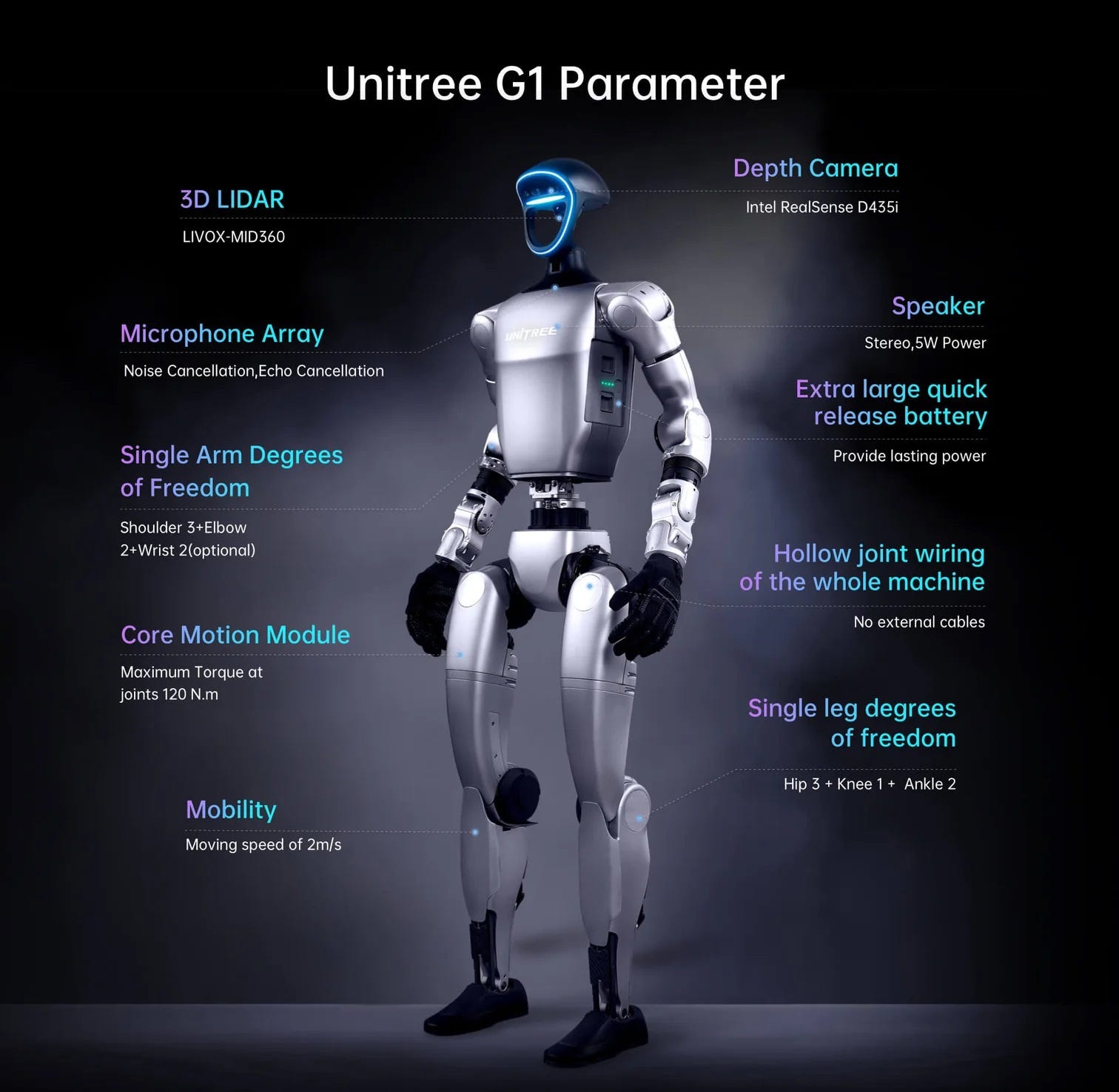

Unitree’s hardware is one of the two highest-volume humanoid platforms in the world by unit count. The intelligence that operates the hardware is not world-class.

This is the honest assessment the prospectus itself implicitly acknowledges. Of the 4.2 billion yuan the IPO is raising, nearly half (approximately 673 million yuan per year over three years) is earmarked for training AI models. Unitree’s existing R&D expenditure on “Multimodal Embodied AI Model” increased exponentially between 2024 and 2025 while other R&D areas grew at a steadier pace. The company’s own strategic plan, documented in the IPO prospectus and the 2025 “Statement to Investors” from Wang Xingxing, is to close the gap between world-class hardware and world-class embodied intelligence.

The current state of Unitree’s software capability:

Motion control and locomotion: world-class. The Drunken Fist routine, the mid-air backflips, the four-meters-per-second cluster coordination, and the autonomous fall-and-recovery are real demonstrations of world-class motion control through reinforcement learning applied to bipedal dynamics. Unitree’s robots are among the most physically capable humanoids shipping today.

Manipulation: competent but limited. The G1 supports force-controlled three-fingered hands with optional tactile feedback. The R1 and H2 offer upgraded dexterous manipulation. The demonstrations exist; the failure rate on unscripted manipulation tasks is not publicly disclosed.

Autonomous task completion: limited. The Spring Festival Gala performance was choreographed. Wang confirmed to 36Kr that the sequences were practiced. Many enterprise demonstrations involve teleoperation with a human operator directing the robot remotely. Autonomous workflow completion in novel environments, which is the capability that would unlock the factory-floor market Tesla and Figure are targeting, remains in development.

Embodied intelligence foundation model: emerging. Unitree’s UnifoLM (Unitree Unified Large Model) initiative, announced in 2025, is the company’s bet on building its own multimodal embodied AI system. The architecture and training details are not publicly disclosed. The IPO proceeds will fund the scaling of this work over 2026-2028. Whether UnifoLM can produce the kind of task generalization that competitors like Figure’s Helix and Google DeepMind’s RT-2 line are demonstrating is the open question.

The pattern matches a broader Chinese robotics industry thesis: world-class hardware, competitive software at the motion-control and perception layers, and a meaningful gap at the embodied intelligence layer where generalization across tasks and environments requires model capabilities that depend on foundation-model research traditionally stronger in US labs.

The 20,000-Unit Bet

Wang told 36Kr in February 2026 that Unitree plans to ship 10,000 to 20,000 humanoid robots in 2026, roughly four times 2025’s 5,500. Morgan Stanley has doubled its 2026 Chinese humanoid shipment forecast to 28,000 units.

The production capacity exists. Unitree’s manufacturing infrastructure claims a 75,000-unit annual capacity ceiling, though this is an aspirational peak rather than a realistic 2026 target. The question is demand.

Unitree’s prospectus is unusually specific about where demand comes from. University and research sales are saturating: there are only so many universities in the world, and Unitree’s quadrupeds and humanoids are already widely deployed across Chinese, US, and European research labs. State-owned enterprise tour-guide applications will continue to grow but have natural ceilings set by the number of business halls, science museums, and cultural sites in China. Entertainment revenue is episodic and does not support twelve thousand units a year.

The long-term prize, as Unitree and every serious humanoid company acknowledges, is industrial deployment where humanoids substitute for human labor at scale. Automotive assembly. Logistics. Warehouse picking. Assembly-line support. These applications require 95-99 percent uptime, sustained autonomous operation, and the kind of task generalization that embodied intelligence has not yet achieved. Tesla’s Optimus is competing for this market. Figure is competing for this market. Apptronik, 1X, AgiBot, and a dozen Chinese entrants are all competing for this market. None has demonstrated sustained commercial deployment at scale.

Unitree’s bet is that hardware leadership plus three years of concentrated AI model investment plus continued cost reduction produces a viable competitor for the industrial market by 2028. The risk is that hardware advantage matters less than embodied-intelligence capability once deployment reaches factory scale, and Unitree’s software work has to catch up faster than Tesla’s, Figure’s, and Google DeepMind’s work progresses.

The Risks

Five risks deserve acknowledgment.

The software gap. This is the most-discussed and the most important. Unitree’s hardware ships; its embodied intelligence is a work in progress. The IPO funding allocation shows the company is taking the problem seriously, but the outcome is not guaranteed. A company that spends 673 million yuan per year on AI model training over three years is still spending less than what Anthropic, OpenAI, or even MiniMax spends annually on foundation-model research. Hardware margin subsidizing software investment is a defensible strategy only if the software investment converges on useful generalization within the runway.

US regulatory pressure. The May 2025 China Select Committee request to designate Unitree as a Chinese military company and add it to the Entity List has not yet resulted in formal action, but the political pressure is real. Security researchers published findings in April 2025 alleging backdoors in Unitree products. Unitree denied intentional backdoors and patched the vulnerability. In September 2025, the same researchers published wormable vulnerabilities affecting the Go2, B2, G1, and H1 lines. If Entity List designation occurs, the 39 percent overseas revenue Unitree reported for the first nine months of 2025 is at immediate risk, and the US academic-robotics customer base that cannot easily substitute away from Unitree hardware becomes a political liability rather than a strategic moat.

Customer concentration in unsustainable segments. University sales saturate. Tour-guide deployments have ceilings. The IPO valuation implies industrial-scale deployment by the late 2020s. If that deployment does not materialize, Unitree is a mid-size industrial hardware supplier with a valuation appropriate to a much larger market opportunity.

IPO regulatory scrutiny. On April 1, 2026, the China Securities Association randomly selected Unitree for mandatory on-site IPO inspection, just twelve days after the Shanghai Stock Exchange accepted the company’s STAR Market application. The selection itself was statistically expected (CSAC samples 20 to 33 percent of recent applicants, and Unitree was one of two companies drawn from six Q1 2026 STAR Market applications), but on-site inspections in Chinese IPO history have produced material delays and occasional withdrawals when prospectus claims fail to verify. Independent analysts have already flagged four areas of likely scrutiny in the prospectus: customer concentration disclosure, the gap between humanoid revenue figures and demonstrated factory deployments, the use-of-proceeds plan, and specific revenue-recognition practices. A clean inspection outcome supports the implied 40 to 50 billion yuan valuation. A finding of material deficiencies would force re-rating not just of Unitree but of the broader humanoid IPO pipeline behind it.

Competitive intensification. AgiBot shipped 5,168 humanoid units in 2025 per Omdia and has built the fastest production ramp in Chinese humanoid history. UBTECH has China Mobile contracts and Dongfeng/NIO pilot programs. A dozen other Chinese humanoid companies announced IPO plans in 2025-2026. Western competitors including Tesla, Figure, Apptronik, Agility, and 1X are funded at scale. TrendForce projects Unitree and AgiBot together will hold roughly 80 percent of Chinese humanoid shipments in 2026, a duopoly structure that benefits Unitree at the top of the market but offers no protection against AgiBot specifically. Unitree’s price-destroyer strategy works against Western competitors but not against other Chinese competitors who can match the manufacturing cost structure.

The Implications

For the engineer: Unitree is the platform Chinese and international embodied-intelligence research runs on. Studying what the community builds on Unitree hardware is studying the actual experimental frontier of embodied AI. The company’s SDK and integration tooling are, by industry consensus, less polished than Boston Dynamics’ or ANYbotics’, but the hardware cost-performance ratio compensates. For any engineer working on bipedal locomotion, whole-body control, or manipulation learning, Unitree is the default hardware target.

For the founder: Unitree validates a specific thesis: in Chinese hardware manufacturing, vertical integration of motors, reducers, and key mechanical components produces structural cost advantages that Western competitors cannot easily replicate. If you are building anything where the bill of materials matters and where Chinese supply chain access is feasible, the Unitree approach (design in-house, manufacture in-house, ship at prices your competitors cannot match) is the template. If you are building at the embodied intelligence software layer, Unitree is either your partner or your competitor depending on how UnifoLM develops.

For the investor: Unitree’s IPO is the cleanest available exposure to Chinese humanoid robotics at scale, but with three qualifications. First, the technology bet is not yet proven: a hardware leader must converge on software capability. Second, US regulatory risk is real and growing. Third, the pricing implies industrial-scale deployment the industry has not yet demonstrated. The company is now profitable, which differentiates it from every other humanoid robotics company you could buy, but the scaled profit history is one year (2024) plus nine months. Profitability today comes from customer segments (universities, tour-guides, entertainment) that will not support the market capitalization implied by the current IPO target. The investment case requires believing UnifoLM will close the gap in time.

The Body Without the Brain

Unitree is one of the two highest-volume humanoid manufacturers in the world, alongside AgiBot. It is also a company whose business model depends on eventually becoming something different than what it is now. The quadruped business that built Unitree is a mature segment where the company has won. The humanoid business that drives the current valuation is a frontier segment where hardware has outpaced intelligence, and where Unitree’s next three years will determine whether the company graduates from hardware volume leader to viable industrial deployment platform, or settles into a profitable but bounded niche supplying the research and entertainment markets.

Wang Xingxing wrote in the IPO prospectus that 2026 marks Unitree’s tenth anniversary. The first ten years built the body. The next ten will determine whether the company can build the brain.

On February 16, 2026, approximately twenty-five Unitree robots performed a Drunken Fist kung fu routine on China’s Spring Festival Gala, the most-watched television broadcast in China. Chinese media reported the cluster as twenty-four G1s and one H2. The robots executed trampoline-assisted aerial flips reaching three meters, performed what Unitree described as the world’s first single-leg continuous flips and seven-and-a-half-rotation airflare spins, and repositioned at four meters per second in coordinated cluster formation. Unitree’s partnership deal with the Gala was reportedly valued at roughly 100 million yuan. Wang Xingxing told state media: “In the past one or two months, I’ve personally been under quite a lot of pressure. We had to deliver a performance that was significantly better than last year’s.” When the Gala director called him to ask whether a robot’s fall during rehearsal had been a malfunction, Wang told her it was part of the routine. Drunken Fist requires a state of precarious balance. A robot that falls and then stands back up looks more convincingly drunk than one that performs cleanly. The fall was scripted.

What viewers saw was a body with no mind: a carefully choreographed sequence executed by hardware doing exactly what it was told. The performance was impressive because the hardware is impressive. The performance was also the ceiling of what Unitree’s current software can reliably deliver without extensive rehearsal and scripted choreography. The company’s bet, its IPO, and its position in China’s embodied intelligence strategy all depend on closing the gap between what the hardware can do and what the intelligence can direct it to do.

The hardware is real. The intelligence isn’t. Not yet.

Inside China’s Machine. China’s AI and robotics ecosystem, from the inside.

Sources

IPO prospectus and financial data: South China Morning Post (”Inside Unitree’s landmark IPO: what to know about China’s humanoid giant,” March 2026), CNBC (”Unitree plans Shanghai IPO, testing interest in humanoid robots,” March 20, 2026), KraneShares (”A Complete Guide To Unitree Robotics’ 2026 IPO,” April 2026), 36Kr (”Half of the Investment Circle Owes Gratitude to Unitree,” March 2026), Caixin Global (”Unitree Robotics Files for $608 Million STAR Market IPO,” March 21, 2026). All financial figures (2025 revenue 1.708B yuan, 335% YoY growth, 600M yuan adjusted net profit, 674% adjusted net profit growth, 288M yuan headline net profit, 204% headline net profit growth, 32.4% global humanoid market share, 5,500 humanoid units 2025) are Confirmed from the Shanghai Stock Exchange prospectus. Historical financial trajectory (2022 net loss 22.1M yuan, 2023 net loss 11.1M yuan, 2024 net profit 94.5M yuan, 2025 9M net profit 105.3M yuan; gross margin trajectory 44.2% in 2023 to 56.4% in 2024 to 59.5% in 2025 9M) is from the prospectus financial summary on the Shanghai Stock Exchange filing portal. Early investor characterization of “profitable since 2020” comes from Zhao Nan via 36Kr (March 2025); this characterization conflicts with the formal prospectus disclosures for 2022-2023, and the prospectus is the primary source. The 40 to 50 billion yuan ($7B) IPO valuation target is per Reuters via CNBC.

IPO regulatory inspection: China Securities Association announcement (April 1, 2026), RobotToday analysis (”Unitree’s IPO Review: What It Means for China’s Humanoid Robot IPO Landscape,” April 2026).

April 30, 2026 R1 dual-arm launch and Wangfujing retail store: Humanoids Daily (”Unitree Expands R1 Lineup with Dual-Arm Modular Platform Starting at $4,290,” April 30, 2026), CNX Software (”$4,290+ Unitree R1-A5 and R1-A7 humanoid robots,” May 1, 2026), Interesting Engineering (”Unitree unveils $4,290 humanoid robot with upper-body-only design,” May 2026), 36Kr (”Unitree Unveils Upper-Body-Only Humanoid Robot,” May 2026), CnTechPost (April 30, 2026). The 26,900 yuan base price is consistent across all sources; the $4,290 USD conversion reflects the May 2026 official rate and is used by the majority of English-language coverage.

TrendForce duopoly projection: TrendForce 2026 humanoid robot industry report, summarized in Jiemian News and 36Kr (April 2026).

Shareholder structure and voting rights: SCMP IPO coverage, 36Kr. Wang Xingxing 23.82% direct + 10.94% indirect, 68.78% voting via special-voting-rights arrangement. Meituan 9.6%, HongShan 7.1%, Matrix Partners China 5.5%. Industrial and financial backers confirmed: Tencent, Alibaba, Ant Group, Xiaomi, ByteDance, BYD, Geely, Shunwei Capital, Shanghai and Beijing state-backed funds.

Founder biography: SCMP, Wikipedia, CnTechPost, 36Kr, ChinaTalk (”Unitree Goes Public” by Irene Zhang, April 2026). Wang born 1990 Ningbo, Zhejiang Sci-Tech University undergrad, Shanghai University master’s (2013 XDog thesis), brief DJI employment, Unitree founded Hangzhou Binjiang District August 26, 2016. Co-founder Chen Li (Hikvision international sales background) confirmed from TechNode interview.

Product pricing: Unitree official global shop (shop.unitree.com as of April 2026): R1 $4,900 presale, G1 $13,500, H2 $29,900, H1 $90,000+. G1 launched $16,000 in 2024 per The Robot Report. Go2 quadruped base configuration confirmed under $2,000.

Customer data: Prospectus (top 5 customers 10.6% of revenue, 71 university orders, 115 winning bids, 39% overseas in first nine months 2025). JD.com largest corporate customer per ChinaTalk. China Mobile 124M yuan contract (Unitree portion 46.05M yuan) per 36Kr. Overseas exceeded 50% in earlier years per Chen Li TechNode interview, with the prospectus showing the more recent decline to 39% in 9M 2025.

Spring Festival Gala technical claims: Wang interview with 36Kr and Cailian (February 2026), as reported by SCMP and CnTechPost. Three-meter-plus maximum backflip height, 4 m/s cluster speed, autonomous coordination via 3D LiDAR. Drunken Fist scripting confirmed by Wang directly. Performance autonomy claim (”fully autonomously”) from Unitree announcement.

Technology assessment: Tech Buzz China (”Unitree Can Build the Body, Can It Build the Mind?” April 2026) for honest technology reading (teleoperation prevalence, 90-minute battery runtime, 95-99% factory uptime requirement gap). UnifoLM described in Unitree official materials and ChinaTalk analysis. R&D expenditure on “Multimodal Embodied AI Model” growth trajectory per prospectus and ChinaTalk.

US regulatory pressure: Wikipedia, US House Select Committee on China public statements (May 2025), ABI Research and security research publications (April 2025, September 2025). Entity List request confirmed; formal designation not yet enacted as of April 2026.

Competitive context: Article 1 (China Humanoid Robotics Industry Landscape) and Article 2 (AgiBot) for AgiBot 5,168-unit comparison. Morgan Stanley 2026 Chinese humanoid shipment forecast (28,000 units) via eWeek. 2024 Unitree humanoid shipment figure (~1,400 units) via Kaiyuan Securities research report cited in 36Kr.

Classification summary: Financial data from prospectus is Confirmed. Technology assessments are Estimated from third-party analysis (Tech Buzz China, ChinaTalk, SemiAnalysis). 2026 shipment targets (10,000-20,000 units) are Projected per Wang’s public statements. 2030 market forecasts are Projected from Morgan Stanley research.

| A guest post by

|

| A guest post by

|