Inside China’s Machine: X Square Robot

Founded in Late 2023. No Mass-Production Yet. Backed by All Four of China’s Internet Giants. Valued at $2.8 Billion. A Bet on the Brain, Not the Body.

On June 29, 2026, a company that had existed for two and a half years and had not yet mass-produced a single robot announced that it was worth 2.8 billion dollars.

X Square Robot, a Shenzhen embodied-AI startup, said it had closed four consecutive financing rounds ending in a Series C, lifting its valuation past 20 billion yuan. What made the milestone unusual was not the number. Chinese robotics valuations had been climbing all year. It was the backer list. According to the company, X Square had become the only embodied-AI firm in China to secure lead-round investment, at different stages, from all four of the country’s internet giants: Meituan, Alibaba, ByteDance, and Xiaomi. The four companies do not agree on much. They compete across food delivery, cloud, short video, and consumer hardware. They had all decided to back the same robot company.

The robots themselves are still prototypes. The flagship, a wheeled humanoid called Quanta X2, exists in limited numbers and has not shipped at scale. The company’s revenue is negligible against its valuation. By the ordinary logic of a manufacturing business, none of this adds up.

It adds up differently once you see the money moving around it. In the first half of 2026 alone, China’s embodied-intelligence and robotics sector recorded 288 financing events and disclosed more than 46 billion yuan in funding, already exceeding the total for all of the prior year. Capital was concentrating at the top, and X Square sat at that top alongside a handful of rivals, several of them also valued near or above 2.8 billion dollars. The frenzy was real and it was specific: investors were not spreading bets evenly across the field, they were piling into a small number of companies they believed could own the future.

But X Square is not a manufacturing business, and the four giants were not pricing robots. They were pricing a bet on the hardest and least proven layer of the entire embodied-AI stack: the brain. This is the story of that bet, why it found X Square specifically, and what it reveals about where China’s robotics money is actually going. The short version: the body is nearly solved, and China is now paying its highest prices for the part that isn’t.

The Independent Variable

The company’s name is a statement of intent. In mathematics, the independent variable is the one you change to drive an outcome, the input that everything else responds to. The Chinese name, 自变量, carries that meaning and adds another: 自 means self, or autonomous. X Square wants to be the variable that changes the world, and it wants the change to be self-generated rather than borrowed. For a company that spent its first year unable to raise money, the name was more aspiration than description.

Its founder is not a typical robotics entrepreneur. Wang Qian earned his bachelor’s and master’s degrees at Tsinghua University, then a doctorate at the University of Southern California, where he worked on robot learning and human-robot interaction. Along the way he did something that, in hindsight, reads as remarkable: he was among the earliest researchers to bring the attention mechanism into neural networks, publishing at the same conference as Google’s early attention work in 2014, three years before the Transformer architecture would reorganize the entire field of AI. He was present at the conceptual origin of the technology that now underpins every large model.

And then he left. Wang moved into quantitative finance, founding a quant fund in the United States that by his own account did well. It should have been a satisfying outcome, the kind of career pivot that ends with a comfortable answer to the question of what to do with a doctorate. Instead he described lying awake at night with a single recurring thought: he should have stayed in robotics. The field he had left at its conceptual beginning had, in his absence, started to become the thing he had glimpsed early. In late 2023 he acted on the insomnia, walked away from the fund, and returned to the field, founding X Square in Shenzhen. His co-founder, Wang Hao, holds a doctorate in computational physics from Peking University and had led the development of one of China’s first ten-billion-parameter large models. The pairing is deliberate: a robot-learning researcher who understood the physical world and a large-model builder who understood scale. Their bet was that the future of robotics would look less like mechanical engineering and more like a foundation model, that the discipline was about to shift from building bodies to training brains.

When X Square launched, that bet was contrarian and, worse, unfundable. The embodied-intelligence landscape in China was already crowded. Galbot and AgiBot had both launched the same year with larger teams and more initial capital, and both had built their early identity around visible, demonstrable machines. X Square operated with almost no public profile, no flashy humanoid to show, and a thesis, that the invisible model mattered more than the visible robot, that was hard to sell to investors who wanted to see something move. It struggled to close early rounds. “The biggest difficulty was that nobody trusted us,” Wang has recalled. Two and a half years later, four of China’s most powerful technology companies would compete to fund it. The thing that made X Square unfundable in 2023, its insistence on building the brain before the body, is precisely the thing that made it the most sought-after embodied-AI investment in China by 2026.

The Brain, Not the Body

To understand what changed, you have to understand what X Square refused to build.

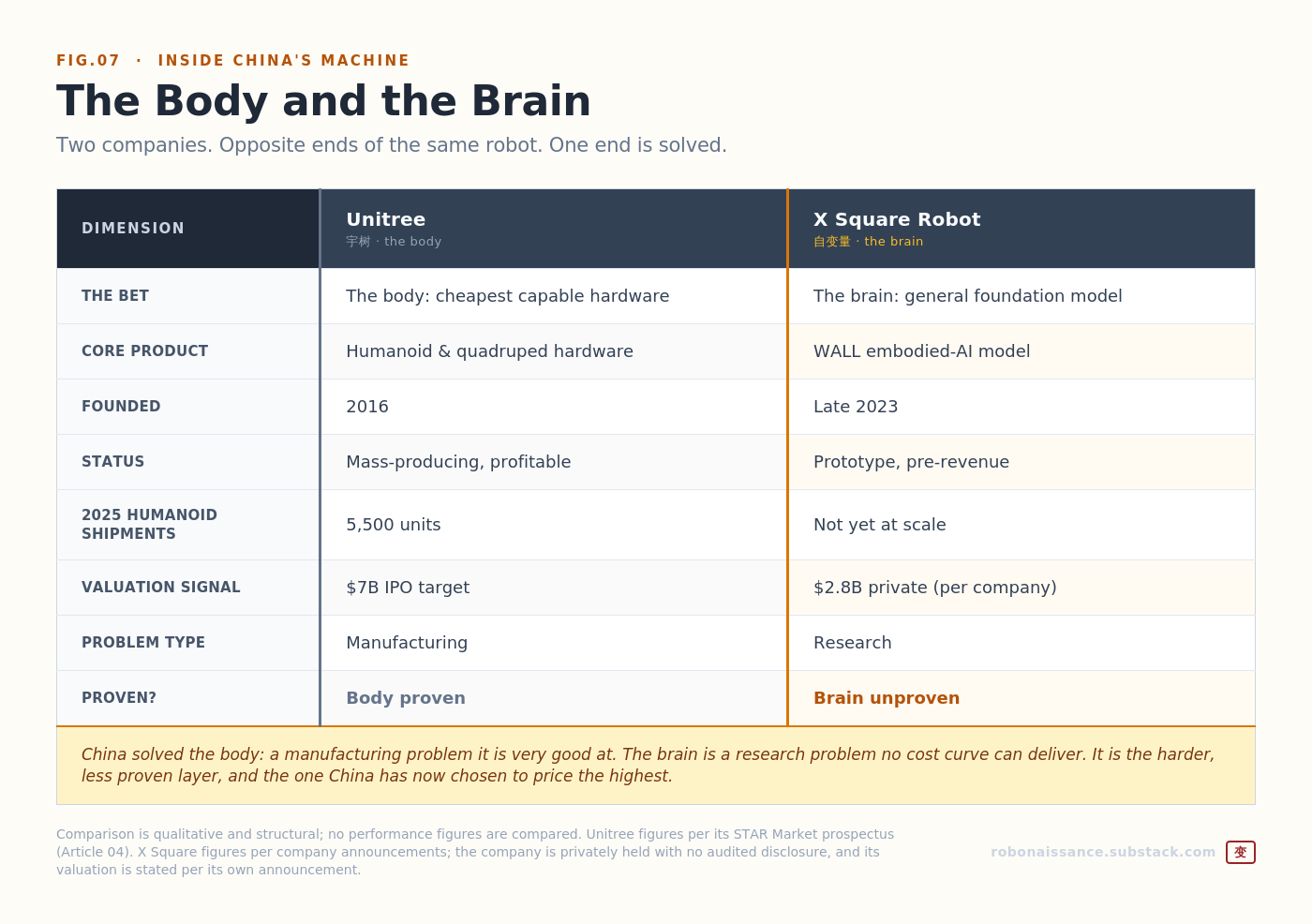

Most of the attention in humanoid robotics has gone to the body: the actuators, the joints, the bipedal locomotion, the choreographed demonstrations. Companies like Unitree turned the body into a real business, shipping thousands of capable machines at prices that collapsed the market. When twenty-five Unitree humanoids performed a kung fu routine on China’s Spring Festival Gala, hundreds of millions of people saw what a Chinese-built body could do. But a capable body is not an intelligent one. That Gala performance took months of rehearsal and pre-programmed choreography; even the stumbles were scripted. A robot that can backflip on command is still following a script. The moment the environment changes, the object shifts, the lighting differs, the scripted machine fails.

Wang’s framing for this is blunt. Traditional industrial robots, he argues, are precise, fast, and useless outside the exact conditions they were programmed for. He has described them as precise waste: machines that execute a pre-programmed instruction thousands of times with perfect repeatability and have no ability to observe the world, reason about it, and adapt. Change one variable and they break. The problem was never the body. The body works. The problem is that the body has no brain capable of handling the open, unstructured, endlessly variable real world.

X Square’s answer is what the industry calls an embodied intelligence foundation model, and specifically a Vision-Language-Action model, or VLA: a single system that takes in sensory input, video, language, tactile signals, and outputs physical action. The goal is a robot brain that parallels what large language models did for text, a model general enough that it does not need to be reprogrammed for every new task. Where Unitree bet that whoever built the cheapest capable body would win, X Square bet that the body is nearly solved and the real prize is the brain. It chose the harder half of the problem, and it chose to build it from scratch, in-house, from the first day. The two companies are not really competitors. They are betting on opposite ends of the same robot, and the market has now decided that the end X Square chose, the harder and less visible end, is worth more.

What WALL Actually Is

The brain has a name: WALL. It has arrived in three stages, and the progression tells you how the company thinks.

WALL-A came first, the company’s initial foundation model, built to integrate the Vision-Language-Action approach with what are called World Models, systems that learn to predict how the physical world will respond to an action. The combination matters. A pure VLA model maps perception to action: it sees, and it moves. Adding a World Model lets the system predict the consequence of an action before taking it, and use causal inference to understand feedback, which the company says sharply improves a robot’s ability to generalize to tasks it was never explicitly trained on. In practical terms, a robot with a World Model can reason about what will happen if it grasps an object a certain way, rather than only reacting after the grasp succeeds or fails. In September 2025 X Square released WALL-OSS, an open-source version of the model family, published on GitHub and Hugging Face. Open-sourcing a foundation model is a familiar competitive move: it seeds an ecosystem, invites outside developers to build on your architecture, and positions your model as a potential standard before anyone has agreed on one, the same logic that let earlier software platforms establish dominance by giving the core away.

In April 2026 came WALL-B, and with it the architectural claim that defines the company’s technical identity. WALL-B is built on what X Square calls a World Unified Model architecture. Where a modular system stitches together separate networks, one for vision, one for language, one for action, and passes information between them, WALL-B trains perception, language, action, and physical prediction inside a single unified network. The pitch is that unification produces stronger multimodal understanding and spatial reasoning than a pipeline of bolted-together parts, because the model learns the relationships between seeing, understanding, and acting rather than having them hard-wired at the seams. A modular system knows only what its designers told it to pass between modules; a unified system can, in principle, discover connections its designers never anticipated. Alongside it the company released WALL-OSS-0.5 and a world-modeling component called WALL-WM, which introduces event-level prediction by aligning language, vision, and action data around specific moments rather than treating them as separate streams.

Whether the unified architecture is decisively better than the modular approach is not yet settled. It is a research bet, not a proven result, and serious labs disagree about which path scales. Modular systems are easier to debug and improve piece by piece; unified systems are harder to train but may capture the world more coherently. But X Square’s bet is coherent, made by people who understand the tradeoff, and it is the thing the company is actually selling to investors: not a robot, but a thesis about how robot brains should be built.

The Benchmark Problem

Here is the number that keeps the story honest.

WALL-OSS-0.5, the model X Square released alongside WALL-B, achieved more than 80 percent autonomous task completion on four out of seventeen real-robot tasks, without post-training. That figure comes from the company itself, and read carefully, it is a study in what embodied AI can and cannot yet do. On four tasks, the model performs well straight out of the box, which is a real achievement for a general model with no task-specific tuning. On the other thirteen, it does not clear that bar. Four out of seventeen is not general intelligence. It is early, honest, promising, and nowhere near the reliability a commercial deployment demands.

This is the gap between the valuation and the capability. The body layer of the stack can be measured in units shipped and prices charged; Unitree moved thousands of robots and turned a profit. The brain layer is measured in success rates on manipulation benchmarks, and the leading Chinese brain, by its own reported numbers, clears a high bar on well under half of a seventeen-task suite. The reason this matters is not that four-of-seventeen is bad. For a two-and-a-half-year-old company, it is impressive. It matters because the market is pricing X Square as though the brain is close to solved, and the brain’s own benchmarks say it is not.

There is also a structural caution here. These numbers are self-reported. There is no audited filing, no independent third-party verification of the kind a public company’s financials would carry. A company reporting its own benchmark chooses which tasks to run, which to report, and how to define success, and every one of those choices can flatter the result. This is not an accusation against X Square specifically; it is the default condition of a privately held company announcing its own capabilities to justify its own valuation. The broader embodied-AI field has begun building shared evaluation platforms, including a real-robot benchmark called RoboChallenge that X Square itself helped organize, precisely because self-reported capability claims are hard to compare across companies and easy to frame favorably. The existence of that effort is a tacit admission by the whole industry that the current numbers cannot be taken at face value. When reading any embodied-AI company’s performance figures, including these, the right posture is interest tempered by the knowledge that the company chose which tasks to report and had every incentive to choose well.

None of this means X Square is overstating its progress. Four-of-seventeen without task-specific tuning is, if anything, an honest number, the kind a company inflating its story would have quietly rounded up or reframed. The distinction is narrower and more important: the capability is real, early, and unfinished, and the valuation assumes it will become real, mature, and finished. The distance between those two states is measured in research breakthroughs that have not happened yet, and research breakthroughs do not arrive on a fundraising schedule.

The Data Flywheel

If the model is the product, data is the moat, and X Square talks about data more than almost anything else.

The company organizes itself around three pillars: models, data pipelines, and hardware, and it insists the three form a loop rather than a line. To feed the model, X Square built its own data-capture tools, teleoperation rigs, exoskeletons, and a system it borrows from academic work called a Universal Manipulation Interface, all designed to record how humans actually perform physical tasks. It then runs what it calls a model-driven data pipeline, using the foundation model itself to decide what data is worth collecting and to generate more of it at scale. The model improves the data collection; the better data improves the model. Wang calls this a flywheel, and his framing of the competition is explicit: the next phase of embodied intelligence, he argues, is a battle of foundation models built on data closed-loops and their capacity to keep evolving.

The hardware exists to serve this loop. X Square has released wheeled robots, the Quanta X1, the X1 Pro, and the more humanoid Quanta X2, and it develops core components in-house, including robotic arms, joint modules, and controllers. But the hardware is downstream of the model, not the point of it. The company made a deliberate choice to build on wheeled bases rather than chase bipedal locomotion, on the argument that legs are an expensive distraction from the real problem, which is manipulation and reasoning, not walking. In one demonstration the company likes to cite, a Quanta X1 completed an autonomous food delivery through an open outdoor environment, a setting with none of the controlled conditions a lab demo relies on. It handled strong winds, a deformed package, and objects it could only partly see, using the model’s causal inference to fill in what was hidden and self-correcting when it stalled, completing the delivery loop without human intervention. In another, facing a disordered pile of parcels, the robot used generalization to pick out irregular items it had not been trained on specifically.

Whether those demonstrations generalize beyond the demonstration is exactly the four-of-seventeen question. A single successful outdoor delivery is not a reliability statistic; it is an existence proof that the approach can work at all, which is different from proof that it works consistently. But the ambition is coherent: a robot that handles the unscripted world by understanding it, not by being told about it in advance. The wager is that this understanding, once the model is good enough, transfers across tasks the way a language model’s fluency transfers across topics. That transfer is the whole thesis, and it is the thing not yet demonstrated at the reliability a business would require.

Why Four Giants Bet

The most revealing fact about X Square is the identity of its backers, because it explains what they think they are buying.

Meituan, Alibaba, ByteDance, and Xiaomi are not natural allies. They are pouring money into X Square anyway, and the logic is not robot hardware, which any of them could commission. The logic is the operating system. If embodied AI develops the way personal computing and mobile did, the durable value will not sit in the machines but in the software layer that every machine runs on, the platform that becomes the default brain for a generation of robots. Betting on X Square is a bet on owning, or at least sitting close to, that layer. It is an option on the robot operating system, bought early, while the price of the option is still a startup valuation rather than a platform monopoly.

Each giant has its own reason to want the seat. Meituan runs the largest delivery logistics network in China, a natural deployment ground for autonomous physical labor, and has led rounds accordingly. Alibaba, through its cloud arm, has a strategic interest in the compute and model infrastructure embodied AI will consume, and co-led an early round through Alibaba Cloud. ByteDance is a foundation-model competitor in its own right with an appetite for the next platform. Xiaomi builds a consumer-hardware and IoT ecosystem into which a household robot would slot directly, and led the Series B. Four different strategic motives converging on one company, and converging specifically because X Square built the foundation model in-house from the beginning rather than licensing a brain or bolting one onto someone else’s hardware. In a field where most companies bet on the body, X Square was the cleanest available bet on the brain, and the giants paid for cleanliness.

The pattern rhymes with earlier platform transitions. In the PC era, the lasting fortune went not to the companies that made the boxes but to the one that made the operating system every box ran. In mobile, the same. The hardware became a commodity; the platform captured the value. If embodied AI follows that arc, the humanoid body will commoditize the way PCs and phones did, driven down a cost curve by manufacturers like Unitree, while the brain, the model that every robot licenses or runs, becomes the layer that compounds. The four giants are each hedging against the possibility that they wake up in a robot-filled world where someone else owns the operating system. Backing X Square is cheaper than that risk. It does not require any of them to believe X Square will certainly win, only that the layer is worth owning a piece of, and that X Square is the purest available claim on it.

The Valuation Gap

Wang Qian is unusually candid about the economics, including the parts that should give an investor pause.

He has argued publicly that China’s embodied-AI companies are valued roughly an order of magnitude below their overseas counterparts, and that the sector needs more capital, more willingness to inflate, to drive the innovation required. He has said he is in no hurry to commercialize, that he allocates about two-thirds of spending to improving the model’s raw capability rather than chasing near-term revenue, and that he expects the first scenarios with positive return on investment to appear around 2026. He has predicted early consumer products in three to four years at a price somewhere between ten and twenty thousand dollars. These are the statements of a founder building for a horizon well beyond the current product, and they are refreshingly free of the pretense that the robots are about to generate meaningful revenue.

They also describe the risk precisely. A 2.8-billion-dollar valuation on negligible revenue is not a claim about today. It is a claim about a future in which X Square’s brain becomes something close to the default operating system for physical AI, deployed across delivery, logistics, elder care, and eventually the home. The valuation prices that future as substantially likely. The four-of-seventeen benchmark, the prototype-stage hardware, and the founder’s own three-to-four-year horizon all say the future is real but far, and contingent on a research bet, the unified-model architecture, that has not yet been proven to win. The gap between what the model can do today and what the valuation assumes it will do is the entire investment. Everything rests on whether the brain, in the end, generalizes.

The Bet on the Brain

Earlier in this series, Cambricon offered a distinction worth borrowing: capability versus capture. Cambricon had proven capability, a good-enough chip that ran at scale, while the market priced a capture it had not yet secured. X Square inverts the pairing. Here the capture has arrived first: four giants, 2.8 billion dollars, the pole position in Chinese embodied AI. It is the capability that remains unproven, sitting at four reliable tasks out of seventeen.

That inversion is the whole point of where China’s robotics money now flows. The body has been substantially solved. Unitree and its peers ship capable machines by the thousand, at prices no Western maker can match, and turn a profit doing it. The body is a manufacturing problem, and China is very good at manufacturing problems. The brain is a different kind of problem. It cannot be driven down a cost curve or scaled through a factory. It has to be discovered, and no amount of capital guarantees the discovery arrives on schedule.

This is why the most expensive bet in Chinese embodied AI is not the company that makes the best robot. It is the company that might, someday, make the best robot brain. X Square is that bet in its purest form: a foundation-model thesis wrapped in prototype hardware, funded by four rivals who each concluded that the software layer is where the lasting value lives. They may be right. The brain is the correct thing to want. It is also the least proven layer of the entire stack, the one part that manufacturing prowess cannot deliver, and the one China has chosen to price the highest. The body is real. The brain is the wager. The next few years will show whether the independent variable actually changes the outcome.

Inside China’s Machine. China’s AI and robotics ecosystem, from the inside.

Sources

Company and founder: Pandaily (”X Square Robot’s Wang Qian: Robots will eventually reach Mars,” April 2026, exclusive interview); Baidu Baike (Wang Qian profile); Chinadaily (”X Square Robot expands development of general-purpose robots,” August 2025); aifun.cc company profile. Founding (December 2023, Shenzhen), Wang Qian’s background (Tsinghua bachelor’s/master’s, USC PhD in robot learning, early attention-mechanism researcher publishing concurrently with Google in 2014, quant-fund founder before returning to robotics), and co-founder Wang Hao (Peking University computational physics PhD, led one of China’s first ten-billion-parameter models) are reported across these sources. The “nobody trusted us” and “precise waste” characterizations are Wang Qian’s own words per Pandaily and Chinese-language interviews.

Funding: PRNewswire / Morningstar / Yahoo Finance / The Robot Report / Pandaily / finsmes (”X Square Robot Secures Four Consecutive Financing Rounds,” June 29, 2026). Series C valuation of over US$2.8 billion (RMB 20 billion), the four-consecutive-rounds structure, and the claim of being the only embodied-AI company in China with lead-round backing from all four internet giants (Meituan, Alibaba, ByteDance, Xiaomi) are per the company’s own announcement, carried by these outlets. IDG participated in Series C; HongShan and Xiaomi in prior rounds. Earlier rounds (Series A+ ~1 billion yuan / $140M co-led by Alibaba Cloud and CAS Investment, September 2025; Series A++ ~$140M January 2026; Series B ~$276M led by Xiaomi, April 2026) are per The Robot Report, Frontier Enterprise, and RoboticsTomorrow. Total funding across rounds is estimated at $500-700M per Cryptobriefing. Valuation is stated per company announcement; there is no audited financial disclosure.

Models and technology: The Robot Report (”X Square Robot debuts foundation model,” September 2025; “secures $140M,” January 2026); RoboticsTomorrow; Frontier Enterprise; citybiz; Pandaily. WALL-A (VLA integrated with World Models), WALL-OSS (open-sourced September 2025 on GitHub and Hugging Face), and WALL-B (April 2026, “World Unified Model” architecture training perception, language, action, and physical prediction in a single network) are per company announcements carried by these outlets. The WALL-OSS-0.5 benchmark result (over 80% autonomous completion on four of seventeen real-robot tasks without post-training) is a company-reported figure; there is no independent third-party verification. RoboChallenge, the shared real-robot benchmark X Square helped organize, is referenced per the RoboChallenge organizing committee and arXiv benchmark documentation.

Products: Robozaps and Humanoid.guide (Quanta X2 specifications: ~172cm, 95kg, 62 total DoF, 6-DoF omnidirectional chassis, dual 7-DoF arms, optional 20-DoF hands, LiDAR/IMU/ultrasonic sensing, WALL-A model); The Robot Report (Quanta X1 autonomous food-delivery demonstration). Product status is prototype per manufacturer listings.

Industry context: BigGo Finance and IT Juzi (China embodied-intelligence funding H1 2026: 288 financing events, over 46 billion yuan, exceeding the prior full year); SiliconANGLE and Bloomberg (AI² Robotics and X Square each surpassing ~$2.8B valuation, June 2026). The “hardware camp versus brain camp” framing of the sector is per BigGo’s industry analysis.

Classification: Founding facts, funding rounds, investor identities, and model release dates are reported across multiple sources and attributed to company announcements where they originate there. All valuation and benchmark figures are company-reported, as X Square is privately held with no audited disclosure, and are attributed accordingly. Wang Qian’s forward-looking statements (pricing, timeline, capital-allocation, valuation-gap views) are his own predictions and characterizations, attributed as such. The unified-model architecture’s superiority over modular VLA is a research claim, not a settled result, and is presented as a bet rather than a fact.

| A guest post by

|

| A guest post by

|