Inside China’s Machine: Zhipu

The World’s First Listed AI Lab. Up Twenty-Five-Fold at Its Peak. Its Best Model Is Free. It Loses Six Yuan for Every One It Earns. The Price Was Never About the Business.

On July 2, 2026, shares in the world’s first publicly traded AI lab fell almost 17 percent in a single session. Six days later, on the morning a lock-up expired and roughly 46 billion Hong Kong dollars of previously frozen stock became sellable, the same shares rose 13 percent. Within twenty-four hours of that, the company sold four billion dollars of new stock into the rally.

Zhipu AI, which trades in Hong Kong under the name Knowledge Atlas Technology, ranks by Bloomberg’s reckoning as the most volatile stock in Asia. The volatility is not a side effect. It is the mechanism.

The underlying business is stranger than the chart. In 2025 Zhipu booked 724 million yuan of revenue, about 105 million dollars. It lost 4.72 billion yuan, about 650 million. It spent 3.18 billion yuan on research and development, roughly 4.4 times its entire revenue for the year. Its flagship model, GLM-5.2, is published under an MIT licence, which means anyone can download the weights, run them on their own servers, fine-tune them, build a commercial product on top, and never send Zhipu a cent.

In late June the market decided this company was worth one trillion Hong Kong dollars, about 128 billion US dollars. More than Meituan, a company that delivers food to hundreds of millions of people and actually makes money doing it.

The easy reading is that the market has lost its mind. The more useful reading is that the market is pricing something real, and the something is not the income statement. It is pricing scarcity, sovereignty, and a float small enough to move with a shove. This is the story of all three, and of what happened when the world finally put a public price on a frontier AI lab and discovered that the price says almost nothing about the lab.

The Tsinghua Lineage

Zhipu did not begin as a startup. It began as a university research group, and the difference explains most of what the company became.

The Knowledge Engineering Group at Tsinghua University, known internationally as THUDM, had spent years working on knowledge graphs and language models before either was fashionable. In 2019 two of its professors, Tang Jie and Li Juanzi, spun the work out into a company. The architecture they carried with them was called GLM, the General Language Model, and it supplied both the company’s technical identity and its name.

The lineage did two things, and only one of them gets written about.

The first is technical. In March 2023, months before most Chinese AI companies had shipped anything a developer could touch, Zhipu released ChatGLM-6B, an open-weight chat model small enough to run inference on a single consumer graphics card. It became one of the most downloaded models of that year and the first widely usable Chinese instruction-tuned large language model. Hobbyists fine-tuned it on laptops. University labs built coursework around it. Enterprises pulled it apart to see how it worked. The habit of giving models away started at the very beginning, and it started for the least romantic of reasons: giving them away was how an academic spin-out got noticed.

The second thing the lineage bought was trust, and trust turned out to be the business. Zhipu became one of the “Six Little Tigers,” the cohort of Chinese large-model startups that emerged during the generative AI wave, and before listing it assembled an unusually broad investor register: Alibaba, Tencent, Ant Group, Meituan, Xiaomi, Hillhouse, Qiming Venture Partners, Chinese local-government funds, and Saudi Aramco’s Prosperity7 Ventures, roughly 1.5 billion dollars in all. A Tsinghua spin-out with state-linked capital on its cap table is a company a Chinese state-owned bank can buy from without anyone in the procurement chain having to justify the decision. That access is not a soft advantage. As the revenue breakdown will show, it is the entire commercial engine.

The third thing, and the one that explains the rest, is a habit of betting early on things that look foolish at the time.

In 2021, with GPT-3 fresh and the Chinese market unconvinced, Tang Jie put the question to an internal meeting: should Zhipu attempt a model with hundreds of billions of parameters? He understood what failure would mean for a company of that size. He decided to do it anyway. Per 36Kr’s account of the period, Zhipu rented a thousand Nvidia A100 cards from the Jinan Supercomputing Center and rebuilt the training operators from the bottom up, then ran the job for eight months. For scale, the Beijing Academy of Artificial Intelligence, one of Zhipu’s own incubators, had 480 A100s in total at the time. Zhipu rented more than twice the card count of the institution that helped birth it, and pointed all of it at a bet most of the field thought was premature.

The result was GLM-130B, and it landed roughly a year and a half before ChatGPT made the world care. Tang has a phrase for the pattern, which he traces back to an academic search engine he ran on a single desktop computer in 2006: essence, counter-intuition, focus. Think hard enough to justify the contrarian path, then hold it long enough for the path to arrive.

Fewer than nine hundred people work at Zhipu. Roughly three-quarters of them are researchers. The company is run by chief executive Zhang Peng, with Tang Jie as its defining scientific figure and Liu Debing as chairman. For a company the market briefly valued above Meituan, it is a very small building full of academics.

What Zhipu Actually Sells

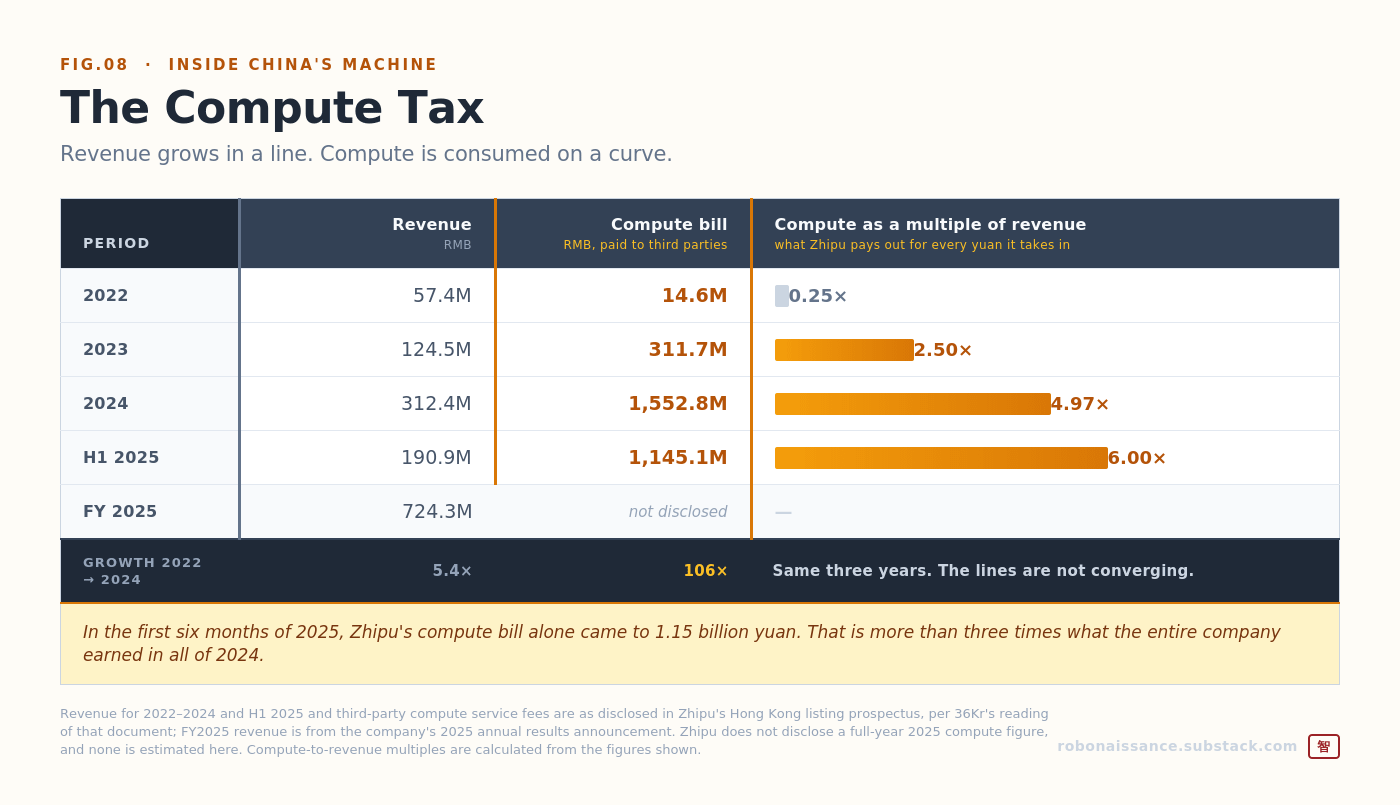

In 2025, 534 million of Zhipu’s 724 million yuan in revenue, 73.7 percent of the total, came from on-premises deployment.

That single number reorganises the company.

On-premises deployment means Zhipu’s engineers go to the customer’s building. They install the GLM model suite inside the customer’s own servers and internal network so that no data ever leaves the premises. They fine-tune the model on the customer’s data. They integrate it with the customer’s existing systems. They stay until it works. Then they do the whole thing again at the next customer.

The customers are Chinese state-owned enterprises, banks, and government bodies: institutions that cannot put sensitive data on someone else’s cloud and will not buy a foreign model at any price. For them a Tsinghua-descended, state-invested, domestically hosted model is not one option among several. It is the option. This is what the Tsinghua lineage bought, converted into invoices.

The remaining 190 million yuan, 26.3 percent, came from the cloud business: the API, the developer platform, the part that behaves like software. That segment is growing quickly. Its share of revenue rose from 15.5 percent in 2024. Its gross margin climbed from 3.3 percent to 18.9 percent as inference optimisation and scale drove the marginal cost of serving a token down.

But the shape of the company is set by the 73.7 percent, and that shape has a problem. Overall gross margin fell from 56.3 percent in 2024 to 41.0 percent in 2025. The on-premises segment’s own margin fell from 66.0 percent to 48.8 percent. Margins compress in that business as it grows, because growing it means hiring more engineers to sit in more buildings. There is no version of on-premises deployment in which the tenth customer is cheaper to serve than the first. Human effort does not have a cost curve. It has a headcount.

The growth is not in doubt. Zhipu’s revenue ran 57.4 million yuan in 2022, 124.5 million in 2023, 312.4 million in 2024, and 724 million in 2025. That is a company roughly doubling every year, and it makes Zhipu the largest independent large-model developer in China by revenue. The trajectory is exactly what a believer would want to see.

Underneath it sits the bill that decides everything. Zhipu’s payments to third parties for compute were 14.6 million yuan in 2022. They were 311.7 million in 2023. They were 1.55 billion in 2024. In the first half of 2025 alone, per figures drawn from the company’s prospectus, they were 1.15 billion.

Set the two series side by side over the same window. Between 2022 and 2024, Zhipu’s revenue grew about fivefold. Over those identical three years, its compute bill grew more than a hundredfold. And in the first six months of 2025, compute alone cost more than the company earned in all of 2024.

The lines are not converging.

Traditional software is written once and copied for nothing, which is why software companies are the most profitable enterprises ever constructed. A large model breaks that. It is written once and then paid for again every single time somebody uses it. Revenue grows in a line. Compute is consumed on a curve, and the curve steepens as context windows lengthen and reasoning chains run longer. For every yuan Zhipu earned in 2025, it handed considerably more than a yuan to chipmakers and cloud providers.

On 31 March 2026, Zhang Peng took all of this to the market in Zhipu’s first earnings call as a public company. He reported the 724 million yuan of revenue. He reported the 4.72 billion yuan loss. He told analysts the company was pivoting from on-premises deployment toward the cloud, that recurring platform revenue had grown sixtyfold, and that Zhipu had raised API prices 83 percent and still could not meet demand. He said Zhipu would continue down the path of being China’s Anthropic.

The next trading day the stock closed up almost 32 percent, at 915 Hong Kong dollars, pushing the company’s market value above 400 billion.

A company had just disclosed that it lost six yuan for every yuan it earned, and the market added a hundred billion Hong Kong dollars to its value. Whatever was being priced in that room, it was not the income statement.

The Open-Weight Paradox

Zhipu’s best model is free.

GLM-5.2, released in mid-June 2026 with support for context windows up to a million tokens, is published under an MIT licence. Download the weights. Run them on hardware you own. Modify them. Build a product. Sell it. Send Zhipu nothing, ever. This is not a hobbled community edition kept at arm’s length from the real thing. It is the flagship, the same model the company benchmarks against the American frontier.

The obvious question is how any of this is supposed to produce a business.

The answer is that openness is a distribution strategy Zhipu can afford precisely because its revenue does not come from selling access to the model. It comes from selling deployment, integration, and service. The open weights are the marketing. The on-premises contract is the product. Giving away the model does not cannibalise the revenue, because the customers paying the revenue were never going to rent a model over an API in the first place. They were going to pay someone to come to their building and install one.

What the giveaway buys is reach. By the company’s count, more than four million registered corporate and developer users across 218 countries and regions, and integration with nine of China’s top ten internet firms. It buys the developer habit, which is the raw material that eventually becomes API revenue. And it buys a specific kind of credential: a model whose weights the entire world has inspected is a model a bank’s risk committee can approve without taking anyone’s word for anything.

The evidence that the strategy is working is not the download count, which is easy to inflate and impossible to bank. It is the price. Through a period when Chinese rivals were slashing API prices to buy share, Zhipu raised its API pricing by 83 percent, and demand kept outrunning supply. Annualised recurring revenue on the open platform reached 1.7 billion yuan, roughly 240 million dollars, a sixtyfold increase year on year, according to figures Zhang Peng gave on the company’s first earnings call as a public company.

A company that can raise prices during a price war has something the price war cannot reach.

What changed the demand curve was agents. The GLM-5 series is tuned for long-horizon software engineering, models that keep working across hundreds of iterations rather than answering one question and stopping, and Zhipu sells a coding plan that plugs into the tools developers already use. When a coding agent runs autonomously for an hour, it does not consume one query’s worth of tokens. It consumes thousands. Zhipu’s chairman, Liu Debing, has argued that the resulting volume and price growth is durable rather than a spike, because it is driven by models getting more capable and users asking them to do more.

That is the bull case in one sentence: an agent is a token furnace, and Zhipu sells tokens.

The Float Machine

None of that explains a stock that went from 116.20 Hong Kong dollars in January to an intraday high of 2,980 on 22 June, a twenty-five-fold move in under six months. For that you need the plumbing.

When Zhipu listed on 8 January 2026 at 116.20 Hong Kong dollars a share, it sold about 43 million shares including the over-allotment, roughly 9.65 percent of its share capital. Of that, eleven cornerstone investors took about 2.98 billion Hong Kong dollars, close to 70 percent of the shares on offer. Cornerstone investors are the large institutions a Hong Kong issuer lines up before an offering: they commit to buy a substantial block, they get a guaranteed allocation, and in exchange they agree not to sell for six months. Retail investors oversubscribed what remained by more than a thousand times.

Do the subtraction. The shares actually available to trade on day one came to roughly 17.35 million. Under four percent of the company.

A stock with a four percent float does not have a price the way a normal stock has a price. It has a clearing level between a very small number of willing sellers and whatever demand turns up, and through the first half of 2026 the demand that turned up was every investor on earth who wanted exposure to Chinese frontier AI and had, until January, no listed pure-play way to get it. Not DeepSeek, which is private. Not Moonshot, which is private. Not Huawei, which is unlisted and does not sell models anyway. There was Zhipu, and there was MiniMax, which listed a day later, and that was the entire menu.

UBS said it without decoration: the valuations reflected a scarcity premium and a limited number of tradable shares. Bloomberg later observed that Zhipu’s shares rank as the most volatile in Asia, in large part because so few of them float.

The machine ran for six months. Then July arrived and ran it in public.

On 2 July, with the cornerstone lock-up approaching, the stock fell almost 17 percent in a session on nothing but the anticipation of supply. It closed at 1,754 Hong Kong dollars and its market value dropped below 800 billion. The trade was so crowded and the float so thin that the mere prospect of 25.68 million shares becoming sellable, 5.8 percent of the company, took roughly a sixth of the value off in a day.

Then the lock-up expired on 7 July, and the cornerstone investors did not sell. Nearly seventy percent of them had committed to hold. On 8 July the stock rose 13.35 percent and added more than 100 billion Hong Kong dollars of market value in a single session, because the absence of selling was read as a vote of confidence.

Within twenty-four hours, Zhipu sold stock into that rally. It placed about 19.8 million new shares at 1,588 Hong Kong dollars each, raising roughly 31.4 billion Hong Kong dollars, a little over four billion US dollars, in one of the largest equity placements Hong Kong has seen this year and more than six times the size of Zhipu’s own IPO. CICC ran the book. The shares were priced at a discount of about 13 percent to the previous close, which is what it took to get institutions to buy at that level.

After the lock-up release, and after the placement, only around 13.5 percent of Zhipu’s issued stock is freely tradable.

The company did not fix the float. It monetised it.

The control experiment ran the next day. MiniMax, the other Chinese model developer to list in Hong Kong in January, hit its own lock-up expiry on 9 July. Its founders had extended their lock-ups. Strategic shareholders had pledged not to sell. It fell more than 20 percent intraday anyway.

The difference was not the plumbing, which was much the same. The difference was that MiniMax had tried to raise the price of its M3 model, been refused by the market, and cut it back. Zhipu had raised prices 83 percent and been paid. A thin float amplifies whatever conviction exists. It does not manufacture it. When the conviction is there, the float turns a good quarter into a twenty-five-fold move. When it is not, the same thin float turns an unlock into a rout.

Trained Without Nvidia

The claim that matters most to anyone tracking China’s AI stack is one Zhipu makes without much fanfare.

GLM-5, the open-weight flagship released in February 2026, was reportedly trained and served on Chinese accelerators rather than Nvidia hardware: Huawei’s Ascend, along with silicon from Cambricon, Moore Threads, and Kunlunxin. On the earnings call, Zhang Peng said Zhipu had been accelerating its use of domestic chips since February to meet a sharp rise in compute demand. The research budget includes co-design work for domestic chip adaptation. The company built its own asynchronous reinforcement learning framework, Slime, in part to make a training pipeline run on the hardware it was actually allowed to buy.

Zhipu did not choose this path so much as have it chosen for it. In January 2025 the US Commerce Department added Beijing Zhipu Huazhang Technology and its subsidiaries to the Entity List, citing concerns that the company was helping advance China’s military modernisation through AI. Zhipu disputes the rationale and says it does not depend on American large-model technology. Whatever one makes of the designation, its practical effect was to restrict access to US technology and turn domestic silicon from a preference into a requirement.

What came out the other side closes a loop that runs through this whole series. A frontier-class open-weight model, competitive on international coding benchmarks, trained on Chinese chips.

Cambricon needed a customer whose inference workloads were large enough to make a domestic accelerator business real. Zhipu needed silicon it was permitted to buy. The chip needed the model. The model needed the chip. Both needed the export controls that created the closed market in which each was the other’s best available option. The stack fork is no longer a forecast. It is a shipped artifact with a benchmark score.

The Sovereignty Trade

In mid-June 2026, Anthropic suspended access to its newest models, Fable and Mythos, in order to comply with US Department of Commerce export controls. Access was restored on 1 July.

Into that window, Zhipu shipped GLM-5.2. In an internal memo reviewed by Bloomberg, Tang Jie set out the argument. Zhipu was choosing a different path, he wrote, reaching higher with one hand to push the limits of intelligence while using the other to lay a road, making frontier capability as open and as widely available as it could be made. Real security, he argued, comes from broad participation and oversight rather than from barriers. The company put the same point more sharply on social media: frontier intelligence should not belong only to a few, nor be subject to withdrawal by a handful of rules at any moment.

The framing was not quite accurate. The models were suspended to comply with a regulatory order, not withdrawn on a corporate whim, and they were back inside three weeks.

The inaccuracy did not matter commercially, and understanding why is the point. A buyer choosing what to build a business on does not price the reason a model might become unavailable. The buyer prices the possibility. Zhipu never argued that American models were worse. GLM-5.2 landed second on the Code Arena front-end leaderboard, behind Anthropic’s Claude Fable 5, and Zhipu did not pretend otherwise.

But look at what that leaderboard said during those three weeks. The best coding model in the world was one nobody outside the United States could use. The second best was one anybody could download for free and run on their own hardware forever. Zhipu did not need to win the benchmark. It only needed the benchmark to be read one row down.

This is the Cambricon logic, moved one layer up the stack.

Cambricon’s chips are not the best chips. They are the chips a Chinese buyer can actually take delivery of, and in a sanctioned market availability functions as a form of performance. Zhipu’s models are not the best models. They are models a buyer can download, audit, host, and keep, and in a market where the frontier can be switched off by a foreign regulator, permanence functions as a form of performance.

Good enough and available beats best and unavailable, in silicon. A model you can keep beats a better model you can lose, in weights. The same trade, made twice, at two different heights of the same stack.

Anthropic or Palantir

Which leaves the valuation, and the valuation reduces to a classification question.

The market is pricing Zhipu the way it prices a frontier platform: a paradigm-setting company with an ecosystem premium and operating leverage that will eventually detonate, where today’s losses are the entry fee for owning tomorrow’s standard. That is the case for a trillion-dollar market capitalisation, and it is the case Zhang Peng makes when he says Zhipu will continue along the path of being China’s Anthropic.

Zhipu’s income statement describes a different company. Nearly three-quarters of revenue comes from project-based delivery to enterprise and state customers, with engineers on site, bespoke fine-tuning, and margins that thin as the work scales. Chinese analysts have made the comparison bluntly: the valuation says Anthropic, the business model says Palantir. Deep client engagement, qualification barriers, and delivery teams, rather than platform economics.

Both descriptions are partly true, and the distance between them is where all the risk lives.

The resolution, if it comes, is visible in the mix. The platform business is the 26.3 percent, and it is the part that is compounding: cloud revenue share rising, cloud gross margin up from 3.3 to 18.9 percent, platform recurring revenue up sixtyfold, prices rising into a price war. The services business is the 73.7 percent, and it is the part that pays the bills today while capping what the company can ever be. Zhang Peng has said the company is shifting from on-premises deployment toward cloud, which is the correct direction and also an admission of what the current mix means.

A trillion-dollar valuation is a bet that the 26.3 percent becomes the company and the 73.7 percent becomes a legacy line item. That transition is possible. It is not yet visible in a single full year of audited results.

The multiples measure that distance. At a trillion Hong Kong dollars, Zhipu traded above a thousand times trailing revenue, with some estimates putting it near 1,280 times. For a rough sense of scale, OpenAI’s reported valuation of around 730 billion dollars against roughly 13 billion dollars of revenue works out near 56 times. Even on JPMorgan’s aggressive forecast of 4.6 billion yuan of Zhipu revenue in 2026, a rise of more than 500 percent, the forward multiple still runs above 200 times. JPMorgan expects profitability in 2028. Soochow Securities models a slower ramp to a smaller number.

The competition is not standing still while Zhipu grows into the price. DeepSeek is reported to have closed more than seven billion dollars in fresh funding. Moonshot is raising ahead of its own listing. MiniMax, which listed in Hong Kong a day after Zhipu, cut the price of its M3 model by half and then watched roughly half its market value disappear. In a market where model capability converges and price becomes the battlefield, pricing power is the only thing separating a platform from a commodity, and pricing power is precisely what Zhipu has so far managed to hold.

It is also going back for more capital. On 1 June the company announced plans for an A-share listing on Shanghai’s STAR Market targeting roughly 15 billion yuan, about 2.2 billion dollars. The application cleared the acceptance stage on 17 June. If it completes, Zhipu becomes the first Hong Kong-listed AI company to run a full dual listing into the mainland, in front of domestic investors who watched Nvidia’s run from the outside and would like a local champion of their own.

The Compute Tax

This series has now met three versions of the same problem.

Cambricon proved capability and has not yet proved capture: a good-enough chip running at real scale, priced by the market as though the share were already won. X Square Robot has capture and has not yet proved capability: four internet giants and a 2.8 billion dollar valuation attached to a model that clears its own benchmark on four tasks out of seventeen.

Zhipu is the third variant, and the most instructive, because it has both.

The capability is real. GLM-5.2 sits second on a serious international coding leaderboard, behind one American model and ahead of everything else that is open. The weights are public, the benchmarks are independent, and the model was trained on Chinese chips. The capture is real too. Nine of China’s ten largest internet companies have integrated its models. Four million developers are registered. Recurring platform revenue grew sixtyfold in a year. It raised prices 83 percent in the middle of a price war and demand went up.

And it still loses roughly six yuan for every yuan it earns.

What Zhipu lacks is neither capability nor capture. It is unit economics. Software’s great trick was always that you write it once and the ten-millionth copy costs nothing to make. Large models break the trick. Every copy costs. Every query costs. Every additional customer arrives with a compute bill stapled to them, and the bill grows with the context window, the reasoning length, and the agentic loop that the entire industry is racing to make longer. Zhipu spent 4.4 times its revenue on research last year not out of recklessness but because that is the current price of standing at the frontier.

On 11 July 2026, three days after the lock-up expired and the company sold four billion dollars of stock, Tang Jie sent his staff a letter titled “The Great Wave Has Arrived.” In it he announced a two-year plan and a decision: Zhipu will not pursue short-term monetisation of AI applications. It will spend the next two years on long-horizon task execution, autonomous agent systems, models that generate their own training data and improve themselves, and safety governance built into the foundation. He described the Hong Kong listing not as an arrival but as a reset, and summarised the choice in a line. Others rang the bell. We returned to zero.

Read that against the compute tax. Zhipu is not failing to fix its unit economics. It is declining to. The founder looked at a company losing six yuan for every one it earns, with four billion fresh dollars in the bank and a market capitalisation the size of a national champion, and told his staff that the correct thing to optimise for is not the margin.

He has done this before. In 2021 he bet the company on hundred-billion-parameter models when the field thought it was premature, and GLM-130B arrived eighteen months ahead of ChatGPT. In early 2025 he decided the chat paradigm was exhausted and turned the company toward coding and agents, and that bet produced GLM-5.2 and everything that followed. Twice the counter-intuitive path paid. He is now betting a third time, and the market has priced the bet as though it has already won.

The world finally has a public price for a frontier AI lab. That price was set by a four percent float colliding with unlimited demand, and what it says is: scarcity, sovereignty, and the option value of being China’s default. What it does not say is that the business works. What the founder has now said, in writing, is that he does not intend to make the business work yet.

Zhipu has proved that a company can build a frontier model on sanctioned silicon, give the weights away for free, and still get the world to pay it. It has not proved that a company can do all of that and make money, and for the next two years it will not be trying to.

Nobody has done this before. Zhipu is simply the first one that has to do it with a ticker, a filing calendar, and a quarterly obligation to show its work.

Inside China’s Machine. China’s AI and robotics ecosystem, from the inside.

Sources

Company, founding, and leadership: AI Wiki (”Zhipu AI”, “Z.ai”); Quartz; South China Morning Post; Rockrose. Founding (2019, spun out of Tsinghua University’s Knowledge Engineering Group / THUDM by professors Tang Jie and Li Juanzi), the GLM architecture lineage, ChatGLM-6B (14 March 2023), the July 2025 rebrand to Z.ai, CEO Zhang Peng, chairman Liu Debing, and the “Six Little Tigers” cohort framing are reported across these sources. Headcount (fewer than nine hundred, roughly three-quarters in research) is per KuCoin and 36Kr, drawn from company disclosures; treat as approximate.

Tang Jie, the GLM-130B decision, and the coding bet: 36Kr; BigGo Finance; geopolitechs; recodechinaai. The 2021 decision to commit to a hundred-billion-parameter model, the rental of roughly a thousand Nvidia A100 cards from the Jinan Supercomputing Center, the rebuilding of training operators, the eight-month training run, and the comparison to the Beijing Academy of Artificial Intelligence’s 480 A100 cards are per 36Kr’s account and are attributed as such in the text; they rest on a single Chinese-language reconstruction of the period and are not company disclosures. GLM-130B’s arrival roughly eighteen months before ChatGPT, the “essence, counter-intuition, focus” formulation, and the 2006 single-desktop academic search system are per Tang Jie’s own July 2026 internal letter as reported by 36Kr, BigGo, and geopolitechs. The early-2025 decision to reallocate toward coding and reasoning following DeepSeek R1 is per Tang Jie’s public remarks and the same letter.

The 11 July 2026 internal letter: Bloomberg (which reports having reviewed the memo directly); Business Standard summarising Bloomberg; 36Kr (exclusive); BigGo Finance; geopolitechs. The letter, titled “The Great Wave Has Arrived,” the two-year “Touch High” plan, the decision to forgo short-term monetisation of AI applications, the four priority areas (long-horizon task execution, autonomous agent systems, AI self-evolution, safety governance), and the “others rang the bell, we returned to zero” formulation are reported across these sources. Tang Jie’s argument that security comes from broad participation and oversight rather than barriers, and his framing of reaching higher with one hand while laying an open road with the other, are per Bloomberg’s account of the memo. Quotations are rendered as reported speech because the letter was written in Chinese and reaches English through translation.

First earnings call as a public company (31 March 2026) and market reaction: South China Morning Post; Yicai Global; CNBC; BigGo Finance. Zhang Peng’s statements on the call (the pivot from on-premises deployment toward cloud, MaaS annualised recurring revenue of RMB 1.7 billion representing sixtyfold growth, API pricing up 83 percent with demand still outrunning supply, the “China’s Anthropic” path) are per these outlets’ accounts of the call. The market reaction (shares closing up about 32 percent at HK$915 on 1 April, lifting market capitalisation above HK$400 billion) is per Yicai Global and BigGo Finance.

IPO and share structure: IPOX; AI Wiki; KuCoin; The Standard; Bloomberg. Listing on 8 January 2026 on HKEX under ticker 2513 (legal entity Knowledge Atlas Technology Joint Stock Company Limited), IPO price of HK$116.20, roughly HK$4.35 billion raised, and an implied valuation near US$6.5 billion are consistent across these sources. The share structure (about 43.03 million shares including over-allotment, roughly 9.65 percent of capital; eleven cornerstone investors subscribing about HK$2.984 billion, close to 70 percent of the offering; approximately 17.35 million shares in free float at listing, under 4 percent of total) is per KuCoin citing the offering documents and Dongwu Securities. Pre-IPO funding of roughly US$1.5 billion and the investor list (Alibaba, Tencent, Ant Group, Meituan, Xiaomi, Hillhouse, Qiming, local-government funds, Prosperity7 Ventures) is per Bloomberg via The AI Rankings.

2025 annual results (reported 31 March 2026): Company announcement via Momenta Media; South China Morning Post; Caixin Global; Yicai Global; CNBC; BigGo Finance; Futu (Soochow Securities commentary). Revenue of RMB 724.3 million (+131.9%), gross profit of RMB 297 million (+68.7%), gross margin of 41.0% (down from 56.3%), IFRS net loss of RMB 4.72 billion (+59.5%), non-IFRS adjusted net loss of RMB 3.18 billion (+29.1%), and R&D expense of RMB 3.18 billion (+44.9%, roughly 4.4x revenue) are confirmed across the company’s results announcement and multiple outlets. The two loss figures are not in conflict: they are IFRS and non-IFRS presentations of the same year. Revenue mix (on-premises deployment RMB 534 million / 73.7%; cloud MaaS and API RMB 190 million / 26.3%), segment gross margins (on-premises 66.0% to 48.8%; cloud 3.3% to 18.9%), MaaS annualised recurring revenue of RMB 1.7 billion (sixtyfold growth), API pricing up 83%, four million registered users across 218 countries, and integration with nine of China’s top ten internet firms are per the results announcement, the earnings call remarks of CEO Zhang Peng, and BigGo’s breakdown. Third-party compute service fees (RMB 14.6 million in 2022, RMB 311.7 million in 2023, RMB 1.5528 billion in 2024, RMB 1.1451 billion in H1 2025) are per 36Kr citing the prospectus.

Share price, lock-up, and placement: Caixin Global; South China Morning Post; BigGo Finance; The Standard; Bloomberg; Cryptobriefing. The 22 June intraday peak (HK$2,980, close HK$2,410, market capitalisation around HK$1 trillion / US$128 billion), the 2 July decline of almost 17% to a close of HK$1,754, the cornerstone lock-up expiry (25.68 million shares, 5.8% of equity, worth roughly HK$46 billion) around 7 July, the 8 July rise of 13.35% adding over HK$100 billion of market value, and the subsequent placement (approximately 19.8 million shares priced at HK$1,588, raising roughly HK$31.4 billion / about US$4.01 billion, roughly 4.2% dilution, CICC as sole overall coordinator, priced at a discount of about 13% to the HK$1,825 prior close) are reported across these outlets. The post-placement free float of around 13.5% and the characterisation of Zhipu as the most volatile stock in Asia are per Bloomberg (10 July 2026). The UBS observation on scarcity premium and limited tradable shares is per Caixin Global. All share prices and market capitalisations in this article are point-in-time and dated where cited; the stock is exceptionally volatile and any figure quoted here may have moved substantially by the time of reading. Multiples of the IPO price are calculated against the HK$116.20 offer price.

Models and benchmarks: AI Wiki; The AI Rankings; BigGo Finance; Asia Tech Review. GLM-4.7 (22 December 2025; 73.8% on SWE-bench Verified, 84.9% on LiveCodeBench), GLM-5 (February 2026), GLM-5.1 (April 2026), and GLM-5.2 (mid-June 2026; context up to one million tokens; MIT licence) are per company releases carried by these outlets. Sources differ on the exact GLM-5.2 release date within mid-June, so no single day is asserted here. GLM-5.2’s second-place ranking on the Code Arena front-end leaderboard, behind Anthropic’s Claude Fable 5, is per Code Arena results reported by Asia Tech Review and Startup Fortune. Zhipu’s own headline benchmark claims are vendor-reported and are treated separately from independent leaderboard results.

Domestic silicon: Reuters via AOL, as summarised by The AI Rankings; CNBC (earnings call). The report that GLM-5 was trained and served on Chinese accelerators (Huawei Ascend, Cambricon, Moore Threads, Kunlunxin) rather than Nvidia hardware is attributed to Reuters reporting and is presented here as reported rather than as company disclosure. Zhang Peng’s statement that the company is accelerating domestic chip use is per CNBC’s account of the earnings call. The Slime asynchronous reinforcement learning framework and “co-design for domestic chip adaptation” R&D allocation are per Soochow Securities’ annual-report commentary via Futu.

Entity List: SCMP via The AI Rankings. The January 2025 addition of Beijing Zhipu Huazhang Technology and subsidiaries to the US Entity List, the cited rationale regarding military modernisation, and Zhipu’s dispute of that rationale are reported per these sources.

Anthropic model suspension: Anthropic suspended access to its Fable and Mythos models on 12 June 2026 to comply with US Department of Commerce export controls, and restored access on 1 July 2026 after those controls were lifted (Anthropic statement: https://www.anthropic.com/news/fable-mythos-access). Zhipu’s public response, framing frontier intelligence as something that should not be subject to withdrawal, is per Zhipu’s social media as reported by Asia Tech Review. This article states the regulatory cause of the suspension because the distinction between a compliance-driven suspension and a discretionary withdrawal is material to the argument, and Zhipu’s framing elided it.

Valuation, forecasts, and competitors: Caixin Global; South China Morning Post; Startup Fortune; BigGo Finance; KuCoin; Asia Tech Review. The price-to-sales multiples (above 1,000x trailing revenue at the peak, with some estimates near 1,280x; forward multiple above 200x on JPMorgan’s 2026 forecast) are analyst and press estimates and vary with the share price; they are presented as indicative rather than precise. JPMorgan’s revenue forecasts (RMB 4.6 billion in 2026, RMB 11.4 billion in 2027, RMB 30.9 billion in 2028, with profitability expected in 2028) are per Caixin Global and SCMP. Soochow Securities’ lower forecasts are per Futu. The OpenAI comparison (roughly US$730 billion valuation against roughly US$13 billion of revenue, per Financial Times reporting) is used only as a rough scale reference. DeepSeek’s reported funding of more than US$7 billion, Moonshot’s raise ahead of listing, and MiniMax’s price cut and share decline are per Asia Tech Review, Caixin Global, and BigGo Finance. The Anthropic-versus-Palantir classification framing is an analyst comparison reported by BigGo Finance citing Chinese market commentary, not a claim originating with this publication.

STAR Market listing: Startup Fortune citing Caixin Global. The 1 June announcement of an A-share listing plan targeting roughly RMB 15 billion (about US$2.2 billion), the 2 to 8 percent post-issuance share capital range, Guotai Haitong Securities as tutoring institution, and clearance of the acceptance stage on 17 June are per these sources.

Classification: Financial results, share structure, IPO terms, lock-up mechanics, and the July placement are Confirmed from company disclosures and multiple outlets reporting them. Share prices and market capitalisations are point-in-time and are dated wherever cited. Domestic-chip training, competitor funding rounds, and analyst forecasts are Reported and attributed accordingly. Valuation multiples are estimates that move with the share price. Zhipu’s own benchmark claims are vendor-reported; only independent leaderboard placements are cited as results here.