The Deployment Gap

$5 billion invested. 13,000 humanoid robots shipped. Fewer than 200 outside China are doing productive work. A company-by-company scorecard.

The Robot Renaissance isn’t measured in press releases. It’s measured in deployment hours. This week, we count them.

In a warehouse outside Atlanta, Georgia, a robot named Digit picks up a plastic tote, pivots, and places it on a conveyor belt.

It has done this more than 100,000 times.

The warehouse belongs to GXO Logistics, the world’s largest pure-play contract logistics provider. The robot belongs to Agility Robotics. Since June 2024, Digit has been working ten-hour shifts at GXO’s Flowery Branch facility, moving totes from autonomous mobile robots to pack-out conveyors for the apparel brand SPANX. It is not a demo. It is not a pilot. It is work, billed monthly under the industry’s first Robots-as-a-Service contract for a humanoid.

That warehouse in Flowery Branch might be the single most important building in the humanoid robot industry. Not because of what happens inside it, but because of what it reveals about everything happening outside it.

Here is the gap: the humanoid robot sector has attracted more than $5 billion in venture and private funding since 2020, according to PitchBook and Crunchbase data. Figure AI alone raised $1.9 billion and commands a $39 billion valuation. Tesla plans to spend $20 billion in capital expenditure in 2026, much of it directed at Optimus production lines. China poured $7 billion into 610 embodied-intelligence deals in the first nine months of 2025, a 250% increase over the prior year, according to IT Juzi, a Chinese venture capital database. Morgan Stanley projects a $5 trillion market by 2050.

And the total number of humanoid robots doing genuinely productive work for paying customers on factory floors and in warehouses? Generously counted, perhaps 1,200. Strip out the research labs and entertainment stages, and the number drops further. In an industry valued in the hundreds of billions, the productive fleet would still fit inside a single warehouse.

This is not a criticism. It is a diagnosis. The entire Western humanoid robot industry, representing tens of billions in invested capital, has roughly 100 units at the productive level for paying external customers. The industry’s most important metric is not who raised the most money or shipped the most units. It is who converted deployment into productive hours, for customers who pay by the month and will cancel the moment the robot stops earning its fee.

The Deployment Hierarchy

Before the scorecard, a framework. The industry uses “shipped,” “deployed,” and “operational” as though they are synonyms. They are not. Understanding the difference is essential to reading every number that follows.

This scorecard covers bipedal humanoid robots and, where data sources include them, wheeled humanoid-form platforms. The category boundary is not stable: see “What the Numbers Tell Us” below for why a single definitional choice can shift global market share by ten percentage points.

Shipped means a unit left the factory and reached a destination. It says nothing about what happens next. A robot shipped to a university research lab, a robot shipped to a trade show floor, and a robot shipped to a logistics customer are all “shipped.” Unitree’s 4,200 units and AgiBot’s 5,168 units are shipment figures. They measure manufacturing output and sales, not productive work.

Deployed means a unit is operating in a real environment, performing tasks. But deployed for whom, doing what? Tesla has placed Optimus units on its own factory floors, though the company has not disclosed how many. When asked directly on the Q4 2025 earnings call, CEO Elon Musk did not provide a number and acknowledged that the robots are not yet doing “useful work.” They are collecting data. That is valuable R&D. It is not commercial deployment.

Productive means a unit is completing tasks that a paying customer values enough to keep paying for. Agility’s Digit at GXO is productive: it moves totes under a monthly Robots-as-a-Service contract. If it stops delivering value, the contract ends. UBTECH’s Walker S2 units at BYD and Foxconn are productive: they perform repetitive tasks on automotive production lines under commercial agreements.

A fourth level exists but no company has reached it. Profitable means the unit generates more revenue than its total cost of operation, including manufacturing, maintenance, integration, and support. No humanoid robot deployment is provably profitable yet.

Every number in this scorecard is tagged to its level in this hierarchy. The industry’s marketing conflates these levels. This analysis does not.

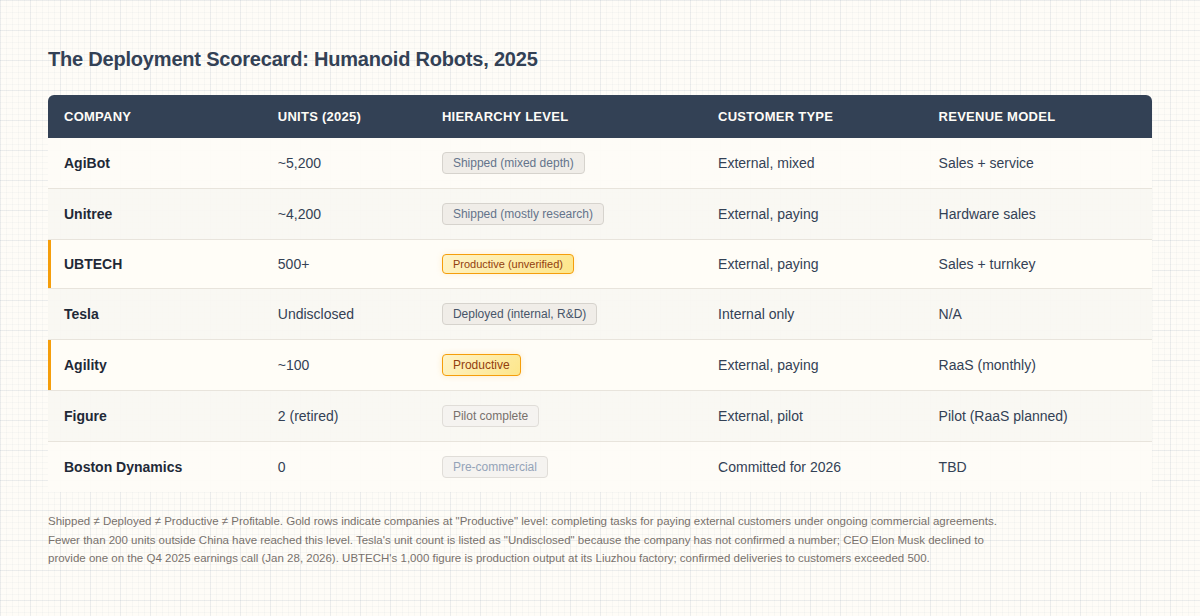

Here is the scorecard summary:

The rest of this article explains how each company earned its place in this table.

The Scorecard

Agility Robotics: The Quiet Leader

Deployment Status: Commercial (Productive)

Agility Robotics occupies an unusual position. It is neither the most funded nor the most famous humanoid robot company. It is simply the one with the most verifiable productive deployment.

The numbers: approximately 100 Digit units sold as of 2025. The GXO partnership, signed in June 2024 after a successful pilot in late 2023, represents the industry’s first formal multi-year commercial agreement for a humanoid robot. The first Digit units went to work in Georgia on June 5, 2024. By October 2025, they had celebrated their one-year anniversary on the job. By November, they had passed the 100,000-tote milestone.

What Digit actually does is deliberately mundane. It picks totes off autonomous mobile robots and places them on conveyors. It stacks containers at different floor locations. It handles payloads up to 35 pounds. The tasks are repetitive, physically exhausting for human workers, and essential to the fulfillment pipeline. They are exactly the kind of work that makes a business case for automation.

Beyond GXO, Agility’s customer list includes the Schaeffler Group, which made a minority investment and committed to deploying Digit across its global plant network. Amazon has been testing Digit for tote handling and item consolidation. Mercado Libre has signed on as a commercial customer. The training approach blends teleoperated demonstrations, reinforcement learning, and simulation, then validates the results through thousands of real-world cycles under variable lighting, placement configurations, and warehouse traffic.

The key insight is in Agility’s business model. The Robots-as-a-Service structure means GXO does not buy robots outright. It pays monthly. That means Agility must deliver sustained, measurable value or the contract evaporates. There is no place to hide behind a one-time purchase.

Scorecard: Real revenue. Real customers. Real deployment hours. The benchmark against which every other company should be measured.

Figure AI: Lessons from the Line

Deployment Status: Pilot Complete (Shipped, no longer Deployed)

Figure AI’s story is a study in contrasts. On one hand: a $39 billion valuation, $1.9 billion in total funding, partnerships with BMW and investors including NVIDIA, Microsoft, OpenAI, and Jeff Bezos. On the other hand: two robots, one factory, one task.

The data from BMW’s Spartanburg plant is the most detailed performance disclosure any humanoid company has published. Two Figure 02 robots worked for 11 months on the body shop floor, running 10-hour shifts Monday through Friday. Their job: picking sheet-metal parts from racks and placing them on welding fixtures, after which traditional six-axis industrial robots welded the parts and fed them into the main line. The cycle time requirement was 84 seconds total, with 37 seconds allocated for the loading phase.

Over that period, the two robots contributed to the production of more than 30,000 BMW X3 vehicles. They moved over 90,000 components and covered approximately 1.2 million steps across 1,250 operating hours. The robots recorded what Figure described as “minimal hardware failures,” with one notable exception: the forearm subsystem was the top failure point, a problem driven by tight packaging, dexterity requirements, three degrees of freedom, and thermal constraints.

That last detail matters. Figure published its failure data. The forearm finding is exactly the kind of hard-won knowledge that only comes from sustained real-world operation: the component that looks fine in simulation, works in the lab, and then breaks on the factory floor because thermal conditions in an active body shop are nothing like a climate-controlled R&D facility. That learning was folded directly into the Figure 03 redesign.

Following the BMW deployment, Figure retired the entire Figure 02 fleet. Figure 03 is the next chapter, with the BotQ manufacturing facility designed for an initial capacity of up to 12,000 units annually and home robotics testing underway. But as of February 2026, Figure 03 has no announced commercial deployment.

Scorecard: Genuine pilot with published performance data. But two robots at one site for 11 months is a proof of concept, not a commercial operation. The valuation-to-deployment ratio is the most extreme in the industry: $39 billion divided by 1,250 operating hours.

Tesla Optimus: The Data Collection Machine

Deployment Status: Deployed Internally (Not Productive, Not Commercial)

Tesla’s Optimus program is simultaneously the most ambitious and the most difficult to evaluate. The ambition: 50,000 units by end of 2026, a dedicated factory at Giga Texas capable of producing 10 million units annually by 2027, a target price of $20,000 to $30,000.

The reality, stated by Elon Musk himself on Tesla’s Q4 2025 earnings call in January 2026: the robots are “not in usage in our factories in a material way.” They exist primarily so the robot can learn.

Let that sink in. Tesla’s own CEO acknowledged, under earnings call scrutiny, that Optimus units on Tesla’s factory floors are primarily training platforms, not productive workers. When asked directly how many units were deployed and performing production tasks, Musk did not provide a number. He said the program is “still very much at the early stages” and “still in the R&D phase.” Previous predictions of 1,000-plus units doing “useful things” by end of 2025, made on the Q4 2024 earnings call, went unmet. The robots are sorting battery cells, handling parts, and navigating factory environments to generate training data. This is valuable work in the R&D sense. It is not productive deployment by the hierarchy defined above.

In January 2026, Tesla commenced Gen 3 production at its Fremont factory, converting Model S and Model X production lines to Optimus manufacturing. The Gen 3 hands represent a significant hardware upgrade: 22 degrees of freedom with 50 actuators, 25 per forearm and hand, up from 11 degrees of freedom in Gen 2. The design uses a tendon-driven system that relocates actuators from the hand into the forearm, a meaningful engineering advance.

But there are no external customers. No purchase option exists. No pre-order system is available. The consumer sale target has been pushed to end of 2027. The production timeline has shifted multiple times. And the gap between Tesla’s stated production targets and its demonstrated capability remains enormous: building 50,000 humanoid robots in a year would represent a 100x increase over the industry’s total cumulative output.

Tesla’s competitive advantage is data. Millions of vehicles collecting real-world driving data gave Tesla an edge in autonomous vehicles. The same logic applies to Optimus: the more robots operating in Tesla’s own factories, the more training data they generate, the faster the AI improves. But data collection is a means, not an end. The question is when “learning” becomes “working.”

Scorecard: Impressive hardware progress. Internal deployment for data collection, though scale is undisclosed. Zero external customers, zero commercial revenue, and the CEO’s own admission that the robots are not yet doing useful work. Every production timeline Musk has stated for Optimus has slipped.

UBTECH: China’s Mass Production Play

Deployment Status: Commercial (Productive)

If you are looking for the company with the most humanoid robots deployed in actual factories doing actual work, it is not an American company. It is UBTECH, based in Shenzhen.

The numbers are striking. UBTECH began mass production of its Walker S2 at its Liuzhou factory in mid-2025. By December, 1,000 units had rolled off the production line. Actual deliveries to customers exceeded 500, meeting the company’s 2025 target. Orders for the Walker series exceeded 800 million yuan, approximately $112 million, since early 2025. Its production targets scale to 5,000 units annually by 2026 and 10,000 by 2027.

The customer list reads like a directory of Chinese manufacturing: BYD, Geely Auto, FAW-Volkswagen Qingdao, Audi FAW, Dongfeng Liuzhou Motor, BAIC New Energy, Foxconn, and SF Express. Walker S2 units are deployed on automotive production lines performing repetitive, mobility-heavy tasks. They are also deployed in logistics operations and data collection centers, including a 159-million-yuan contract in Zigong, worth approximately $22 million, and a record 250-million-yuan order signed in September 2025.

Some skepticism is warranted. When UBTECH released footage of hundreds of Walker S2 robots moving in synchronized formation inside a warehouse, Figure CEO Brett Adcock publicly questioned whether the footage was computer-generated. UBTECH denied this. More fundamentally, the Chinese humanoid robot market benefits from strong government support and subsidies that make direct cost comparisons with Western companies complicated. “Orders” are not the same as “sustained productive deployment,” and the Chinese market’s enthusiasm for humanoid robots may be running ahead of demonstrated ROI.

Still, the volume is real. More than 500 units delivered to industrial customers, from a production run of 1,000, is a milestone no other humanoid company has matched.

Scorecard: By far the largest deployed fleet among companies focused on industrial customers. Real customers in real factories. But questions remain about depth of deployment: how many hours per robot, what task complexity, what failure rates? And the role of government support in creating artificial demand deserves scrutiny.

AgiBot: The Shipment Champion and a Definitional Problem

Deployment Status: Commercial (Shipped, Mixed Deployment Depth)

According to Omdia’s General-Purpose Embodied Intelligent Robot 2026 report, the company that shipped the most humanoid robots in 2025 was not Tesla, not Unitree, and not UBTECH. It was AgiBot, a Shanghai-based startup founded in February 2023. In under three years from founding to global volume leader, AgiBot shipped 5,168 units and captured 39% of the global market.

That statistic deserves a closer look.

AgiBot’s portfolio spans three form factors: full-sized bipedal humanoids in the A-Series, compact half-sized humanoids in the X-Series, and wheeled mobile manipulators in the G-Series. When AgiBot announced its 5,000th unit off the production line in December, the company disclosed the breakdown: 1,742 A-Series bipedal units, 1,846 X-Series half-sized units, and 1,412 G-Series wheeled robots. As The Robot Report noted, roughly 3,588 of those are actually bipedal. The remaining 1,412 are dual-armed mobile manipulators on wheels. Whether a wheeled robot with two arms counts as a “humanoid” is not a trivial question when global market share rankings depend on the answer.

The deployment scenarios are broad: reception and hospitality, entertainment performances, industrial manufacturing, logistics sorting, security patrol, data collection, and research education. At its October 2025 launch event, AgiBot demonstrated the industrial-grade G2 performing seatbelt lock cylinder assembly alongside human workers, precision RAM insertion learned within an hour, and autonomous logistics sorting handling more than 95% of factory floor conditions. The G2 features automotive-grade components, submillimeter accuracy, and dual hot-swappable batteries for 24/7 operation.

This breadth is simultaneously AgiBot’s strength and its analytical challenge. A company deploying robots for hotel reception and factory assembly and security patrol and entertainment is covering enormous ground. But it raises the question of depth. Is AgiBot solving one industrial problem with relentless focus, or spreading across many use cases to maximize shipment volume before its planned Hong Kong listing, targeted for Q3 2026?

AgiBot won multiple Best of CES 2026 awards and entered the U.S. market in January. Bloomberg described it as “topping the list of humanoid producers.” But the company’s most important test lies ahead: converting breadth of deployment into depth of industrial value.

Scorecard: Global shipment leader by Omdia’s count. Remarkable speed from founding to scale. But the 5,168 figure includes wheeled robots that stretch the definition of “humanoid,” and the deployment mix skews toward service and demonstration roles rather than sustained industrial production. The definitional ambiguity in industry reporting is not AgiBot’s fault, but investors should understand what the numbers contain.

Unitree: The Research Platform Giant

Deployment Status: Commercial (Shipped, Mostly Research)

Unitree claims to have shipped over 5,500 humanoid robots in 2025. Omdia’s more conservative estimate puts the figure at approximately 4,200, ranking Unitree second globally behind AgiBot. Either way, Unitree has shipped more humanoid robots than every Western competitor combined. The Hangzhou-based company has been profitable every year since 2020, according to CEO Wang Xingxing, though audited financials have not yet been published ahead of the planned STAR Market listing. It is preparing for an IPO on Shanghai’s STAR board, targeting a valuation of up to 50 billion yuan.

The numbers are real. The question is what they mean in the deployment hierarchy.

The vast majority of Unitree’s shipments are G1 units, a compact humanoid standing 130 cm tall, priced from $16,000 to $73,900 depending on configuration. Its primary customers are universities and research labs: Stanford, MIT, UT Austin, Amazon’s robotics research division. These institutions buy G1 units the way biology departments buy microscopes. They are tools for research, not tools for production. The G1 is the platform on which graduate students train algorithms, test locomotion strategies, and publish papers. It is enormously valuable for the field. It is not doing useful work on a factory floor.

Unitree’s larger H1, at 180 cm and $90,000, has been trialed at Nio and Geely factories and showcased at every major robotics event from CES to NVIDIA’s GTC. The company has appeared at China’s Spring Festival Gala two years running. In January 2025, 16 H1 robots performed a creative dance called “YangBOT,” twirling handkerchiefs in northeastern Chinese-style floral jackets. In February 2026, the performance escalated dramatically: G1 and H2 robots executed kung fu sequences, parkour, aerial flips, and Drunken Fist routines alongside students from the Tagou Martial Arts School. Both performances were stunning technical demonstrations of coordinated locomotion. But a controlled stage performance and a factory shift are different tests. As Chinese technology analyst Patrick Zhang noted, “Robots may struggle in real-world environments, but on stage they hold all the advantages.”

Most recently, Unitree released footage of G1 robots assembling robot parts in Unitree’s own factory, powered by a new embodied AI model called UnifoLM-X1-0. This is a meaningful step: robots building robots creates a closed-loop data engine. But it is also a carefully controlled internal deployment, not third-party customer work.

CEO Wang Xingxing has proposed what he calls the “80/80” test: the moment a humanoid robot can complete 80% of tasks in 80% of unfamiliar environments. By that standard, Unitree is candid about where it stands. The company forecasts a breakthrough in capabilities by 2026, with mainstream commercial use three to five years away.

Scorecard: Second-highest unit volume globally, first among purely bipedal platforms. Profitable. Real products at real price points. But the bulk of shipments go to research and entertainment, not industrial production. Unitree is the world’s leading seller of humanoid research platforms. Whether it is the world’s leading deployer of humanoid workers is a different question.

Boston Dynamics Atlas: The Deliberate Latecomer

Deployment Status: Pre-Commercial (2026 Units Fully Committed)

Boston Dynamics is the company that made humanoid robots famous through a decade of viral YouTube videos featuring parkour, backflips, and box-stacking feats. It is also, as of February 2026, the company with zero commercial humanoid deployments.

That is about to change. At CES in January 2026, Boston Dynamics unveiled the production version of its all-electric Atlas. The company began manufacturing immediately at its Boston headquarters, and all 2026 units are fully committed: fleets will ship to Hyundai’s Robotics Metaplant Application Center and Google DeepMind in the coming months.

The approach is deliberately conservative. Boston Dynamics spent over a decade on Atlas R&D. It retired the iconic hydraulic Atlas in April 2024, replacing it with an electric platform redesigned for commercial viability. The production version features components designed for compatibility with automotive supply chains, backed by Hyundai Mobis actuators. The robot is priced at approximately $420,000, positioning it firmly at the premium end.

Hyundai, which holds an 80% controlling stake in Boston Dynamics, acquired from SoftBank for $880 million in 2021, is both the parent company and the first customer. Plans include a robotics factory capable of producing 30,000 Atlas units per year, with deployment at Hyundai’s new Georgia Metaplant targeted for 2028. Additional external customers are expected in early 2027.

Scorecard: No commercial deployment yet, but the most methodical commercialization approach in the industry. The Hyundai backing provides manufacturing scale, a guaranteed first customer, and the supply chain infrastructure that most startups lack. If execution matches the plan, Atlas could scale faster than anyone once it starts.

A Note on Customer Hedging

BMW’s trajectory illustrates how customers are navigating this market. After its Figure AI pilot ended with the Figure 02 retirement, BMW did not wait for Figure 03. Its Leipzig plant in Germany is now piloting AEON, a humanoid robot from Hexagon Robotics, marking the first humanoid deployment in European automotive production, with a full pilot phase beginning summer 2026. For customers, the switching costs between humanoid providers are still low. The robots are not yet differentiated enough to create lock-in. This is good news for the industry’s development, but a warning for any company that assumes a pilot converts automatically into a long-term contract.

What the Numbers Tell Us

According to Omdia, the global humanoid robot market shipped approximately 13,000 units in 2025, a year of explosive growth. The three Chinese leaders, AgiBot, Unitree, and UBTECH, account for roughly 80% of that total. But sort those units by their level in the deployment hierarchy, and the picture changes sharply. The entire Western humanoid robot industry, representing tens of billions in invested capital and hundreds of billions in projected market value, has approximately 100 units at the “productive” level for paying external customers.

Four patterns emerge from this data.

First, the deployment funnel is brutally narrow. There are approximately 50 companies building humanoid robots worldwide. Fewer than ten have any commercial deployment. Fewer than five have repeat customers doing productive industrial work. The industry talks in billions. It ships in dozens to factories.

Second, the tasks are profoundly simple. Digit moves totes. Figure 02 loaded sheet metal. Walker S2 performs repetitive mobility-heavy tasks on production lines. These are not the general-purpose, multi-skill, cognitive robots of investor presentations. They are pick-and-place machines in a human form factor. That is not a failure. It is a necessary starting point. But the gap between “move a tote” and “do anything a human can do” is measured in decades, not quarters.

Third, “units shipped” conflates fundamentally different markets. AgiBot deploys across hospitality and light industry. Unitree sells research platforms to universities. UBTECH sells industrial automation to auto manufacturers. Agility sells productive labor hours to logistics companies. Each is a valid business. But only the last two prove that humanoid robots can do industrial work that someone will pay for on an ongoing basis. Investors who treat all unit sales as equivalent will misread the market.

Fourth, “humanoid” itself is an unstable category. AgiBot’s global lead includes 1,412 wheeled mobile manipulators. They have two arms and a torso. They do not have legs. Omdia counts them. Other analysts might not. When a single definitional choice can swing global market share by ten percentage points, the industry needs clearer taxonomy before investors can make meaningful comparisons.

The Reliability Threshold

These four patterns share a common root cause. The gap between “shipped” and “productive” is not primarily a manufacturing problem or a sales problem. It is a reliability problem.

Rodney Brooks, the co-founder of iRobot and Rethink Robotics, has spent decades building robots that ship to real customers. His assessment of the humanoid robot industry is characteristically blunt: “I know how hard it is to deploy robots, and how hard it is to make something a customer is really going to pay for. It’s got to be very, very reliable. And it’s got to work with a bunch of nines: 99.999% of the time.”

That number, 99.999%, is the threshold. Run the math: a robot working 10-hour shifts encounters thousands of decision points per shift. At 99.9% reliability, it fails multiple times per day. At 99.99%, it fails a few times per week. At 99.999%, it fails once every few months. The difference between “impressive demo” and “useful worker” is three orders of magnitude in reliability.

Reliability is not a fixed property of a robot. It is a property of a robot in a specific environment. The same Digit that completes 10-hour shifts at GXO’s Flowery Branch facility would face a different reliability profile in a cold-storage warehouse, a pharmaceutical cleanroom, or an automotive body shop running at 40°C. Each new environment demands re-integration: new sensor calibrations, new path planning, new edge cases that only surface after hundreds of operating hours. This is why deployment does not scale like software. Doubling the number of robots is a manufacturing problem. Doubling the number of environments is an engineering problem, and a much harder one.

This is why Agility’s 100,000-tote milestone matters more than Tesla’s undisclosed fleet of Optimus units. Agility’s number measures successful task completions for a paying customer. Tesla’s number, whatever it is, measures units on the floor for data collection. One is a reliability metric. The other is a logistics metric. They are not the same.

And every hour a robot spends on a factory floor at the “productive” level generates data that no simulation can replicate: how lighting conditions affect grasp reliability at 3 AM, how a freshly waxed floor changes traction, how a forearm subsystem fails under sustained thermal stress. Figure published its forearm failure data. That knowledge, earned through 1,250 hours of real operation, is worth more than another round of simulation benchmarks. Agility’s 100,000-tote milestone represents not just proof of concept but a compound data advantage that accelerates with every shift. Deployment data is the new moat.

What This Means

The deployment gap is not a temporary condition. It is the natural state of an industry where the distance between “works in the lab” and “works on the floor” spans three orders of magnitude in reliability. But the gap also contains a signal: the companies and strategies that are closing it fastest tell us where the industry is actually heading, as opposed to where pitch decks say it is heading.

For engineers: One of the most undervalued career moves in humanoid robotics right now is reliability engineering at a company with actual deployments. The forearm failure, the thermal constraint, the waxed-floor edge case: these problems are only visible from the factory floor, and solving them is what separates robots that demo from robots that work.

For founders: The RaaS model is winning. Agility and Figure are both moving toward it. It aligns incentives correctly: the robot company only gets paid when the robot delivers value. It also creates recurring revenue and a data flywheel. If you are building a humanoid robot company and your business model requires customers to write a seven-figure check before deployment, you are making adoption harder than it needs to be.

For investors: Watch the deployment hours, not the funding rounds. Figure AI’s $39 billion valuation rests on 1,250 hours of commercial operation. AgiBot’s global shipment crown includes wheeled robots and hotel reception units alongside factory workers. UBTECH’s $112 million in orders comes with 500-plus units delivered from a production run of a thousand. The ratio of valuation to verified productive deployment hours is the single best measure of how much future is priced into a company’s present.

The pattern from past technology cycles is consistent. In the early days of the internet, the gap between market capitalization and revenue was astronomical. Most of that gap eventually closed, often painfully. The companies that survived were the ones that converted hype into recurring usage. Amazon did not win by having the highest valuation. It won by having the most customers buying the most products the most often. The humanoid robot industry will follow the same logic. The question is not who has the most capital, but who will be the first to make deployment hours compound.

The Warehouse Test

Come back to Flowery Branch, Georgia. The Digit robot picks up another tote. It does not know it is making history. It does not know that $5 billion in venture capital has been invested to create its industry. It does not know that Morgan Stanley projects a $5 trillion market for its successors by 2050.

It just picks up the tote, pivots, and places it on the conveyor.

That is the test. Not whether a robot can do a backflip. Not whether a press release promises 50,000 units next year. Not whether a valuation has enough zeros.

Can it pick up the tote again? And again? And again, for 10 hours, five days a week, for a customer who is paying by the month and will cancel the contract the moment the robot stops being worth the fee?

That is the only question that matters.

What an amazing research report. I wasn't aware of most of this. I still question the wisdom of deploying humanoid robots for most production environments. OTOH, I heard recently that Japan's interest in it is largely targeted to elder-care. To Westerners, this sounds preposterous and inhumane, but the Japanese have a somewhat different relationship with synthetic beings.

What a fascinating read! It’s a really smart breakdown of why it’s so hard to take humanoid robots from the lab into the real world.